The Bank of Canada leaves rates unchanged, seeing as "appropriate" despite energy shock.

Bank of Canada April 2026

Andrew DiCapua

Share:

The Bank of Canada stepped away from standing ready to act and feels like they can now standby. Governing Council appears more confident that the Canadian economy is moving onto a firmer footing heading into the second quarter, following a disappointing start to the year. But a weaker loonie and renewed strength in commodity prices will make the Bank think twice before lowering interest rates.

The Bank has raised its inflation outlook, while its preferred measures of core inflation remain unchanged. Policymakers still see the oil shock as largely temporary rather than the start of a broader inflation problem. The overall message is that the Bank believes current policy remains appropriate. The economy is still too soft to justify a rate increase, but inflation and geopolitical uncertainty leave little room for a cut.

Expectations of a rate hike have now largely evaporated, which could add further pressure to an already weak Canadian dollar. While the economic outlook has improved, GDP growth is now expected to come in below 1% this year. That ongoing slack should help contain underlying price pressures, even as the war in the Middle East pushes headline inflation higher in the second quarter.

Overview

The Bank of Canada held its policy interest rate at 2.25%, as widely expected. Recent data have given Governing Council more confidence that the economy is recovering from a disappointing start to the year, but not enough confidence to change rates.

Economic activity was essentially flat in the first quarter, partly because of temporary declines in government spending, motor vehicle production and oil and gas investment. The Bank estimates that GDP growth rebounded to an annualized 2.5% in the second quarter. BDLNow is more optimistic, estimating growth of 4.6% based on data available as of July 13.

The decision was also less hawkish than previous communications. Language suggesting consecutive rate increases could be needed was removed, and market expectations for a near-term hike largely evaporated. Oil prices have fallen from their April peak, but remain volatile and sensitive to developments in the Middle East.

Growth outlook

The July Monetary Policy Report expects Canada’s economy to grow by just 0.7% in 2026, down from the 1.2% forecast in April. The downgrade reflects the weak start to the year rather than a deterioration in the forward outlook. Growth is projected to strengthen to 1.8% in both 2027 and 2028 as exports recover, investment improves and excess capacity is gradually absorbed.

Economic projections, July 2026

| Real GDP growth, % | 2026 | 2027 | 2028 |

| Canada | 0.7 (1.2) | 1.8 (1.6) | 1.8 (1.7) |

| United States | 2.4 (2.4) | 2.4 (2.3) | 2.4 (2.3) |

| China | 4.7 (4.7) | 4.2 (4.2) | 4.1 (4.2) |

| Global | 2.8 (3.0) | 3.2 (3.0) | 3.2 (3.2) |

Exports are expected to contribute more to growth as businesses adjust to the new trade environment and expand sales outside the United States. A weaker Canadian dollar should make Canadian products more competitive, while strong U.S. investment in artificial intelligence could lift demand for Canadian metals, electrical equipment and other inputs. However, the weaker loonie will also raise import prices and add modestly to inflation.

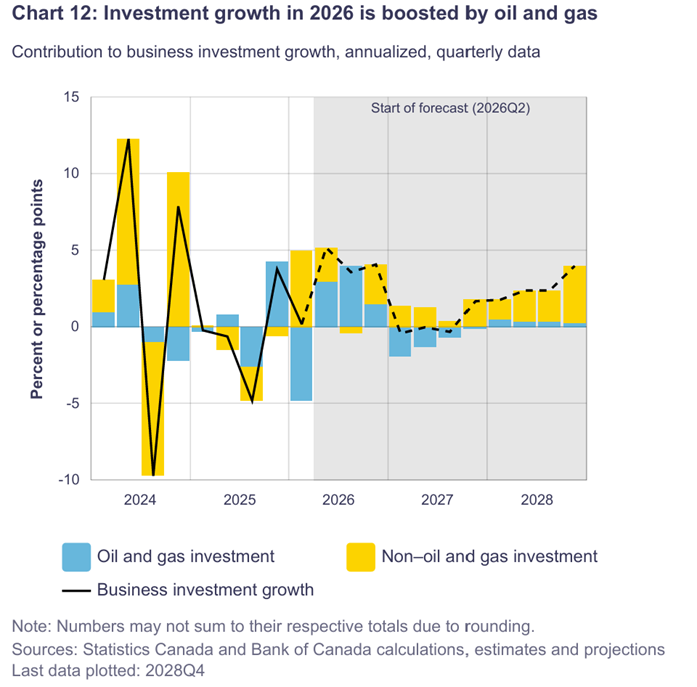

Business investment is expected to improve, initially led by the oil and gas sector. Infrastructure and major energy project announcements have also “contributed” to greater confidence in the outlook, although many remain in development and will take time to appear in the economic data.

Global GDP is expected to be 2.8% this year, shifting growth into 2027. U.S. and China see similar growth trajectories to projections in April’s MPR.

Despite the second-quarter rebound, Canada’s economy remains in excess supply. The output gap is expected to close gradually through 2027 and 2028, leaving room for the economy to grow without immediately generating significant domestic inflation pressure.

Risks to inflation

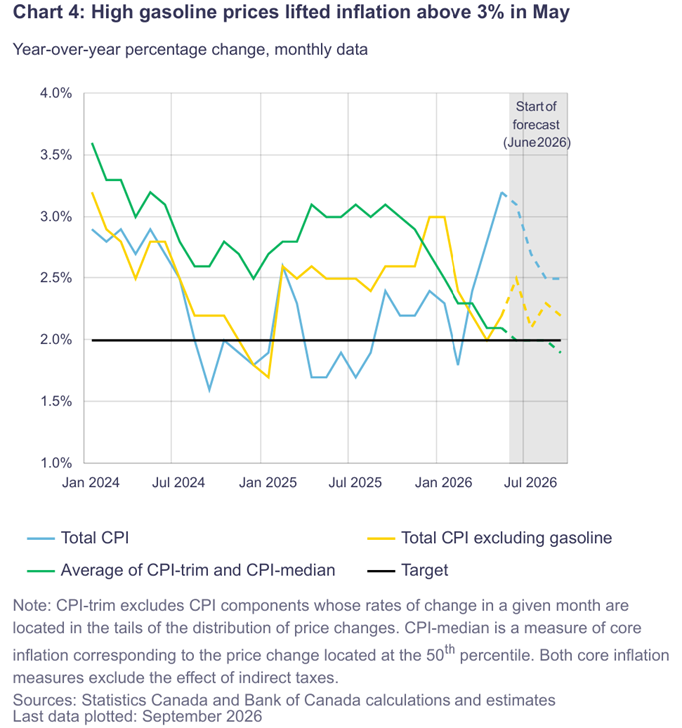

Headline inflation reached 3.2% in May, largely because of gasoline prices. The Bank expects inflation to ease from around 3% in the second quarter to roughly 2.5% during the second half of 2026, before returning to its 2% target in early 2027. Core inflation has moderated and is now close to 2%, suggesting the energy shock has not yet become a broader inflation problem.

The Bank can look through the direct effect of gasoline prices, but the indirect effects are harder to ignore. Higher transportation, fertilizer and other input costs are moving through supply chains. The Bank estimates these additional war-related costs could add about 0.4 percentage points to inflation at their peak in early 2027.

The risk is that businesses pass more of these costs on to customers than the Bank expects. A weaker dollar could amplify that pressure by raising import prices. For now, excess supply, softer services inflation and subdued labour-cost growth should help contain the pass-through.

Conclusion

Governing Council’s next decision is scheduled for September 2. Our base case is that rates will remain unchanged for the rest of 2026. The economy is improving, but remains too soft to justify a hike, while inflation and geopolitical uncertainty leave little room for a cut. The Bank is now less concerned about an immediate rate move and more focused on whether the recovery can build momentum without allowing energy-related price pressures to spread. For now, standing by remains the clearest path forward.

Other Blogs

Canada’s labour market finally caught a bit of a break in June: Labour Force Survey May 2026

Record Exports Signal a Broader Trade Story: Merchandise Trade May 2026

Canada’s economy starts the second quarter with firmer footing

The Inflation Gap Widens as Price Pressures Spread Beyond Energy: May 2026 CPI

Consumers Keep Spending, but the Menu Is Narrowing

The Bank of Canada faces a dilemma as it extends its holding pattern

Canada’s Trade Story Finds New Supporting Cast: Merchandise Trade April 2026

It is green across the board for May’s labour market: Labour Force Survey May 2026