The Bank of Canada faces a dilemma as it extends its holding pattern

Bank of Canada June 2026

Andrew DiCapua

Share:

The Bank can’t have their cake and eat it too. It is understandable that the messaging is intended to avert panic, while keeping its options open, but that balancing act will get harder. Governing Council acknowledged that the economy is still expected to remain in excess supply heading into the second quarter, while also making clear that it is prepared to look through some of the near-term inflation pressure from higher energy prices. However, their commitment to raise interest rates consecutively to address potential inflation pressures doesn’t jive, all of which could occur during significant upcoming trade volatility.

The path forward is becoming less certain, and the Bank can only buy so much time for a clearer answer that may not come quickly. With significant headwinds still facing the Canadian economy, and signs that the consumer strength that has helped support growth is beginning to weaken, a lower policy rate should not be ruled out entirely.

Key Takeways

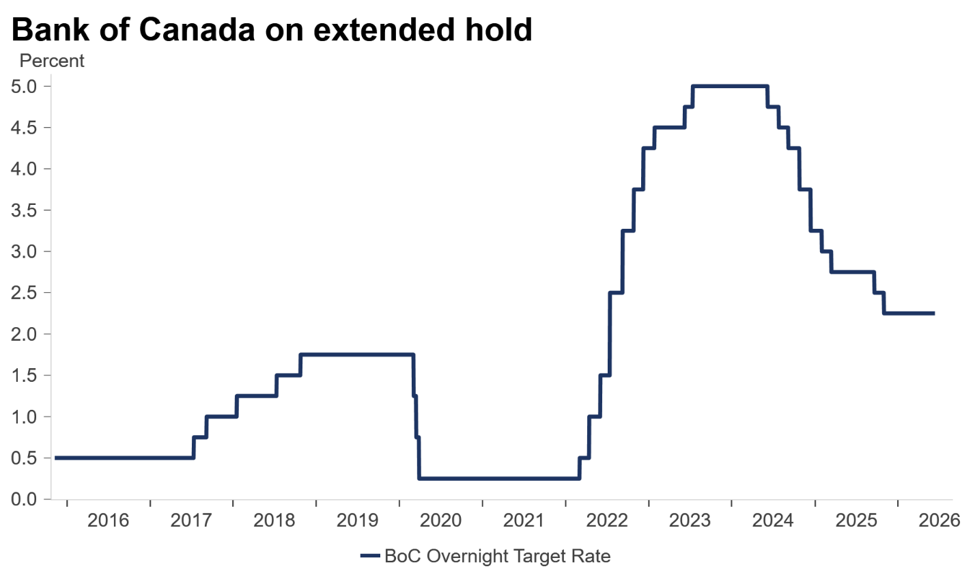

The Bank of Canada held its policy interest rate at 2.25% for the fifth consecutive meeting. As the war in the Middle East enters its fourth month, oil prices have remained elevated and inflation has risen. CPI inflation reached 2.8% in April, and the Bank expects inflation to hover close to 3% in the near term before easing gradually back toward target.

The decision comes after the Canadian economy contracted slightly in the first quarter. Real GDP edged down by 0.1%, weaker than the Bank expected in its April Monetary Policy Report. The details were mixed. Consumer spending continued to grow, rising 1.4%, but government spending unexpectedly declined. Housing activity fell, business investment remained weak, exports declined and imports rose strongly as businesses rebuilt inventories.

For now, the Bank is choosing patience. Governor Macklem said growth is expected to resume in the second quarter, supported by consumer spending and some stabilization in housing. However, even with a rebound, the economy is still expected to remain in excess supply. In a more normal cycle, weak growth, soft housing activity and excess supply would make the case for lower interest rates more straightforward. However, higher energy prices and trade uncertainty are complicating the picture.

The inflation details give the Bank some room to wait. The April increase was largely driven by energy prices and the impact of the elimination of the consumer carbon tax falling out. So far, there is limited evidence that higher energy prices are passing through broadly into other consumer prices. Core inflation measures improved in April, moving closer to 2%.

That said, the Bank is clearly worried about second-round effects. If higher energy prices influence transportation, food and input costs and broaden inflation, the statement indicated that “consecutive” rate hikes would be needed to address inflation. The longer oil prices stay elevated, the greater the risk that inflation expectations move higher.

With the confluence of supply shocks hitting the economy, inflation pressures can be absorbed by a weaker economy. There does not appear to be a strong growth engine in the economy. Consumer spending has helped hold growth up, but households are facing elevated costs reducing purchasing power. Business investment remains weak, exports are under pressure and trade uncertainty continues to weigh on confidence.

Implications

Although the Bank of Canada remains firmly on hold, further trade disruptions or weaker economic data would tilt the balance of risks toward rate cuts, while broader inflation pass-through from energy prices would tilt the balance toward hikes. The meeting was hawkish as Governor Macklem explicitly kept consecutive rate hikes on the table if energy prices become generalized and persistent inflation. As we move into the sixth Bank of Canada interest rate decision, the economy will remain in excess supply, holding the Bank to their position that they will look through temporary inflation. As such, we shouldn’t eliminate the possibility of a future cut in this environment.

Sources: Statistics Canada; Canadian Chamber of Commerce Business Data Lab

Other Blogs

Inflation cools ahead of the summer months

The Bank of Canada gains more confidence in growth prospects despite inflation risk

Canada’s labour market finally caught a bit of a break in June: Labour Force Survey May 2026

Record Exports Signal a Broader Trade Story: Merchandise Trade May 2026

Canada’s economy starts the second quarter with firmer footing

The Inflation Gap Widens as Price Pressures Spread Beyond Energy: May 2026 CPI

Consumers Keep Spending, but the Menu Is Narrowing

Canada’s Trade Story Finds New Supporting Cast: Merchandise Trade April 2026