Recession or Resilience? An unexpected first-quarter GDP contraction points to an uphill battle.

GDP Q1 2026

Andrew DiCapua

Share:

First-quarter growth was a disappointment. We’re certainly in a vulnerable position, with some of the key engines of growth beginning to sputter. Households were a strong source of growth, but some of that strength is water weight, which could evaporate quickly as we head into the second quarter as consumers draw down savings. Domestic demand, which had been an important source of resilience, weakened again. Business capital investment has now fallen for five consecutive quarters. There are some encouraging signs from industrial machinery and mineral exploration investment, and April shows some hope. This does not set the economy up for growth we had expected this year with the outlook to remain choppy. For the Bank of Canada, weak domestic conditions will be a clear concern and should eliminate the likelihood of rate hikes in the near term.

Key Takeaways

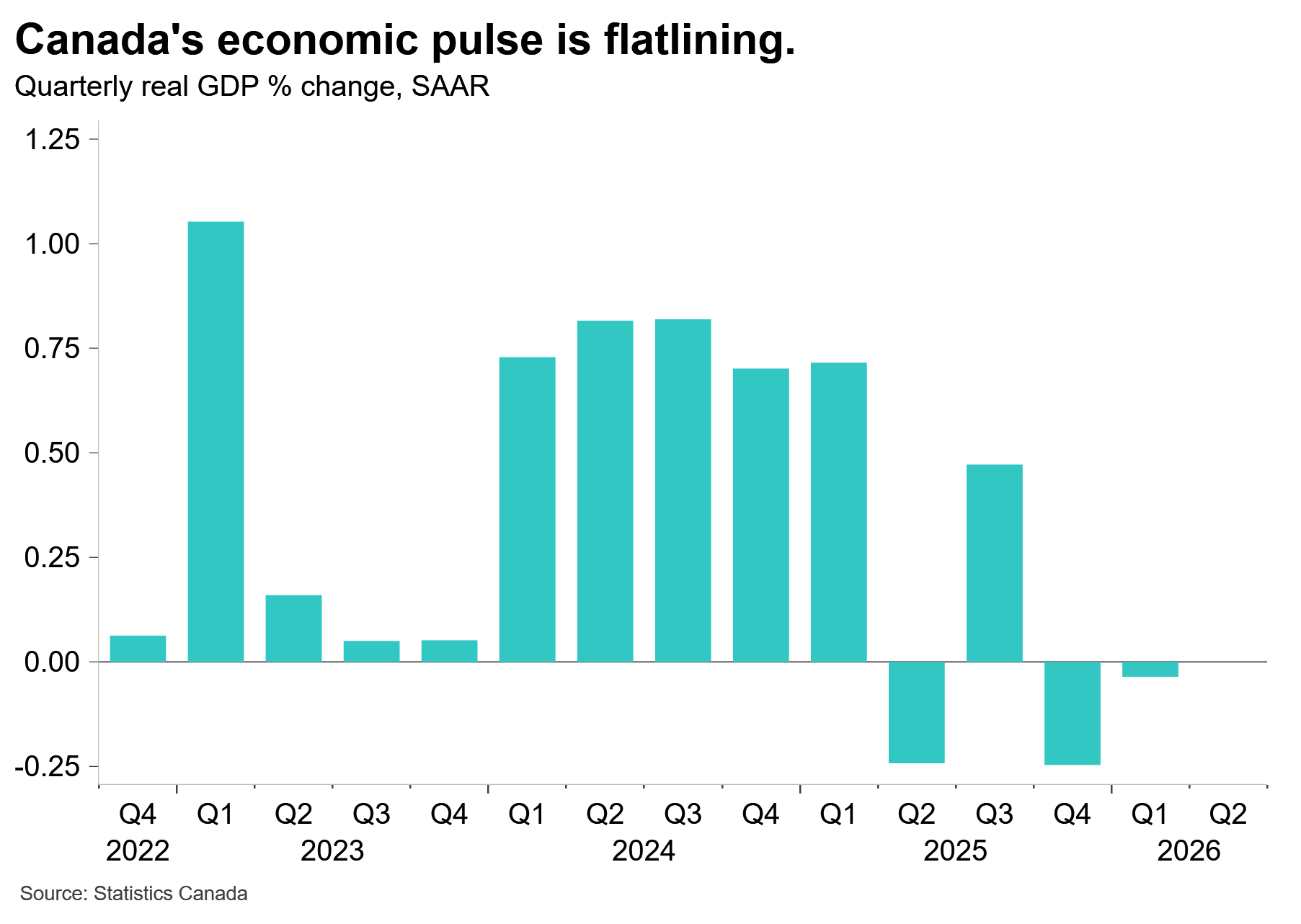

The Canadian economy unexpectedly dipped into a technical recession in the first quarter, declining 0.1% at an annualized pace. This was well below economist consensus estimates of 1.5% and BDLNow’s estimate of 0.9% q/q annualized. The resilience narrative has seemingly evaporated, with mixed signals from monthly GDP in the first two months of the year suggesting growth was still on pace.

Coming off a revised 1% annualized contraction in Q4 2025, we were hoping some domestic fundamentals would continue despite the headline decline. That wasn’t the case. First-quarter GDP was very weak, led by a significant increase in imports, partly offset by higher inventories and household demand.

Trade volatility returned, with imports up 12% annualized in the quarter, roughly half of which was tied to gold-related categories. Exports edged down 0.5% annualized, led by lower shipments of passenger cars and light trucks, which Statistics Canada noted have been impacted by U.S. tariffs. Higher crude oil and natural gas exports helped offset some of the weakness.

Households contributed about 0.2 percentage points to first-quarter GDP. Outside of inventories, this was the only component that supported activity. Household spending rose 1.5% annualized, led by financial services and food, but was tempered by fewer Canadians travelling abroad and lower purchases of new vehicles. Per capita spending remains healthy, though the household saving rate fell to 3.5%, its lowest level since the first quarter of 2024, suggesting consumers have less cushion if higher oil prices persist. Government spending dragged on growth, declining 2.4% annualized. This could reverse later in the year as measures announced in Budget 2025 begin implementation.

Business investment remains notoriously soft. Business capital investment fell 3% annualized in Q1, marking the fifth consecutive quarterly decline. Residential investment also fell 8%, following a 9% annualized decline in Q4, as resale housing activity remained weak. After a significant inventory drawdown last quarter, inventory investment built back up in the first quarter. Mineral exploration and software grew in the quarter and are up from last year, while industrial machinery investment rebounded in Q1 but remains significantly below last year’s level. Overall, the investment picture is choppy, though there should be more momentum in minerals and mining.

On a per capita basis, real GDP increased 0.2% as population declined for a second consecutive quarter while overall GDP was unchanged. We expect this to continue improving in 2026, reflecting more stabilization in living standards. However, stronger economic activity will be needed as population growth reverses its decline later in 2026.

March GDP added to the weak handoff from the quarter. Real GDP by industry edged down 0.1% in March, partially offsetting February’s 0.2% increase. Goods-producing industries contracted 0.8%, their fifth decline in six months, while services edged up only 0.1%. Mining, quarrying and oil and gas extraction, construction, and retail trade were key drags, while wholesale trade provided some offset.

Implications

Despite two consecutive quarters of decline meeting the technical definition of a recession, this isn’t a recession. That oversimplifies the challenges Canada faces, but there also isn’t the broad-based economic decline and elevated unemployment that would cause the C.D. Howe Institute to raise the recession flag. We’re walking on a treadmill at its lowest setting. We’re not burning much fat and we could trip, but we’re not likely to fall on our head.

Economic growth was well below the Bank of Canada’s April MPR estimate that GDP would grow 1.5% in the first quarter, which was also close to what monthly industry GDP had been tracking. Despite a declining population, consumption has held up, though the lower saving rate could signal that spending is being squeezed by higher oil prices and slower wage growth. StatCan’s April GDP flash points to a handoff of 0.4%, but the disconnect between monthly industry data and quarterly expenditure accounts leaves little room for optimism.

This report should wipe out any lingering concerns about near-term rate hikes. The Bank of Canada has been balancing a softer economy against inflation risks tied to higher energy prices, but today’s GDP numbers shift the focus back toward growth risks. This is not the kind of economic backdrop that supports tighter monetary policy.

Charts

Other Blogs

Canada’s labour market finally caught a bit of a break in June: Labour Force Survey May 2026

Record Exports Signal a Broader Trade Story: Merchandise Trade May 2026

Canada’s economy starts the second quarter with firmer footing

The Inflation Gap Widens as Price Pressures Spread Beyond Energy: May 2026 CPI

Consumers Keep Spending, but the Menu Is Narrowing

The Bank of Canada faces a dilemma as it extends its holding pattern

Canada’s Trade Story Finds New Supporting Cast: Merchandise Trade April 2026

It is green across the board for May’s labour market: Labour Force Survey May 2026