Canada’s economy starts the second quarter with firmer footing

GDP April 2026

Andrew DiCapua

Share:

This is not an economy in recession. April’s GDP rebound shows the economy is still chugging along, even if growth remains sluggish and not especially strong. Oil and gas provided the support, but the better signal is that the second quarter is off to a decent start, especially after the slight upward revision to previous GDP data. One encouraging sign is non-residential construction, which expanded for the tenth straight month. That points to some demand for business capital, although it is still too early to say whether this is showing up as sustained momentum in headline investment activity.

For the Bank of Canada, this rebound supports the view that risks are fairly balanced. Higher inflation driven by temporary oil price spikes is one thing, but there is not enough demand in the economy right now to suggest growth is about to reignite inflation.

Key Takeaways

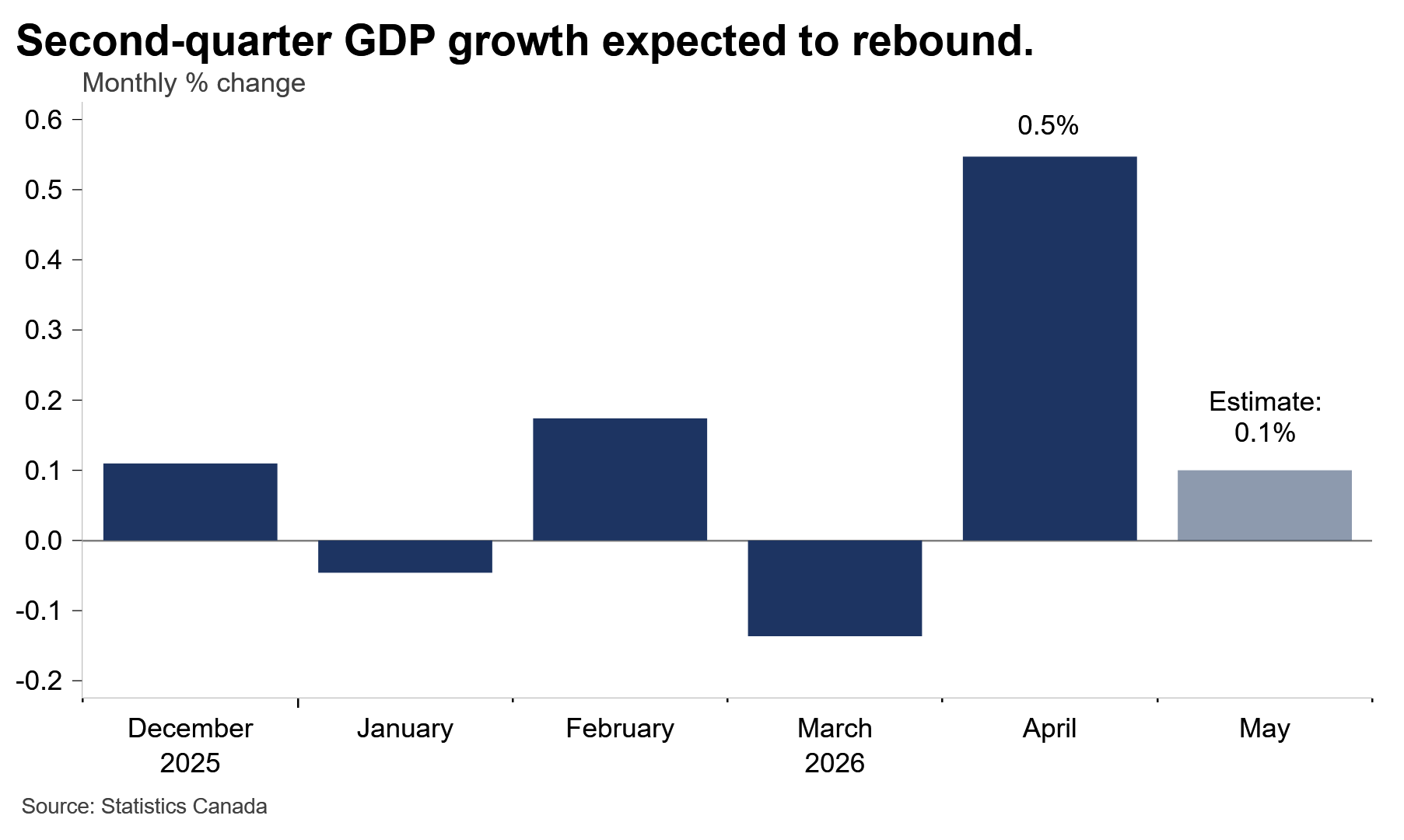

Canada’s economy got a much-needed boost in April. Real GDP expanded 0.5%, reversing the 0.1% decline in March, with mildly positive revisions to prior months. This does not erase the softness seen earlier in the year, but it does push back against the idea that Canada’s economy is sliding into recession. The better read is that the economy is still chugging along, with April showing broader momentum than we have seen in recent months.

Goods producing industries did most of the heavy lifting, expanding 1.3% in April. Mining, quarrying and oil and gas extraction was the overwhelming driver, rising nearly 3% as energy output rebounded and higher oil prices continued to support activity.

The encouraging part is that the rebound was not just an energy story. GDP rose in 14 of 20 sectors, with both goods and services expanding. Manufacturing contributed to the gain, supported by stronger production tied to energy products, motor vehicles and other manufactured goods. This is a welcome sign after a difficult start to the year for trade-exposed sectors, although it is still too early to call it a durable turnaround.

Construction also provided a positive signal, expanding for the first time in four months. Residential construction led to the expansion as more multi-unit buildings come online. Real estate also expanded as resale activity picks up. Non-residential construction continued to expand into its 10th month, which points to some underlying demand for business capital and commercial building activity. That said, we aren’t seeing consistent quarterly non-residential investment.

Public administration added to growth, while accommodation and food services also improved, suggesting some resilience in consumer facing services. Retail trade, however, was essentially flat in volume terms. This is expected to rebound in May, but it will be important to see how higher gasoline prices are distorting demand signals.

Implications

April puts the second quarter off to a much better start. Our tracking suggests second quarter GDP is currently on pace with a strong rebound of 2.3% annualized, which would mark a clear improvement from the slump at the start of the year. Early indicators for May also point to continued, though more modest, growth, with manufacturing and retail advance estimates quite positive.

For the Bank of Canada, this report supports the balanced risk assessment. The economy has regained some momentum, but not enough to suggest demand is running hot. Higher oil prices are expected to continue to impact headline inflation and boost Canada’s oil sector, but April’s data do not point to the kind of broad demand pressure that would reignite inflation. The economy remains in excess supply and is still far from overheating.

Charts

Other Blogs

The Inflation Gap Widens as Price Pressures Spread Beyond Energy: May 2026 CPI

Consumers Keep Spending, but the Menu Is Narrowing

The Bank of Canada faces a dilemma as it extends its holding pattern

Canada’s Trade Story Finds New Supporting Cast: Merchandise Trade April 2026

It is green across the board for May’s labour market: Labour Force Survey May 2026

Where Canada’s defence debate goes next

Recession or Resilience? An unexpected first-quarter GDP contraction points to an uphill battle.

Pivot or Peril: Are Canadian Cities Diversifying or Doubling Down on America?