Narrow Strait, Wide Impact:

How a Global Shock Reaches Canada

Jasleen Trehan

Share:

With the conflict in the Middle East entering its 12th week, the Strait of Hormuz — a 30-nautical-mile-wide chokepoint carrying one-fifth of global oil — has become the fault line of a global supply shock.

What started as a bottleneck led to rerouting and higher fuel costs — and with fertilizer prices already spiking, more expensive groceries are not far behind. This is a familiar inflation story that many Canadians will remember from 2021–2022, when pandemic-era supply chain disruptions, later compounded by Russia’s invasion of Ukraine, sent the cost of living to its highest level in a generation, prompting the Bank of Canada to raise rates sharply in response and leaving many households stretched thin. The context may be different, but higher inflation is almost certain.

Why the Strait of Hormuz closure matters to Canada

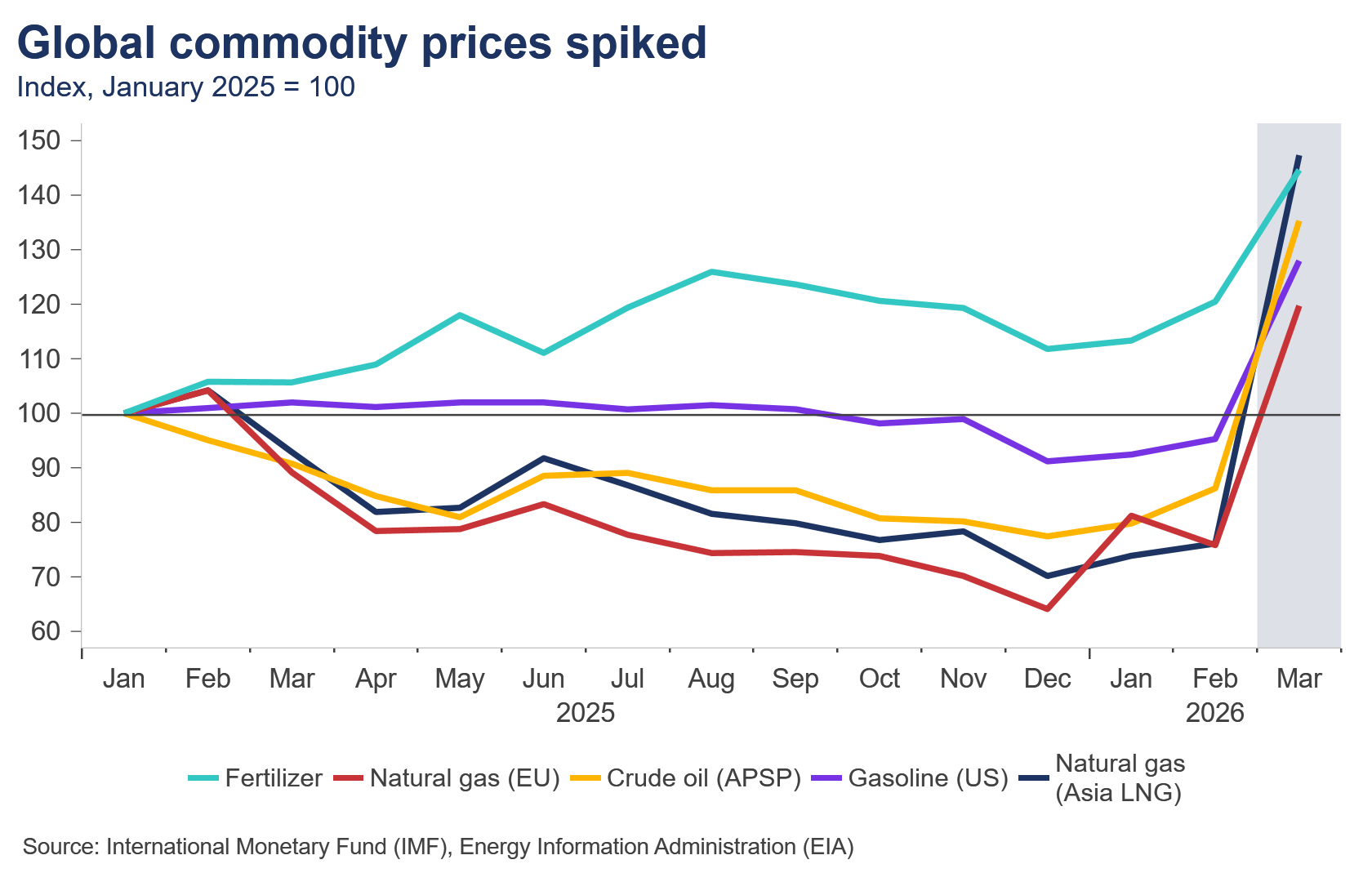

The Strait of Hormuz carries roughly 20 million barrels of oil a day through a chokepoint with almost no viable bypass. As the conflict intensified, tanker flows collapsed from nearly 60 per day to near-zero in early March, triggering the IEA’s largest ever coordinated emergency stock release.

Critically, 83% of Hormuz flows go to Asian markets — Japan, South Korea, India and China — the economies with the least supply diversification and highest physical dependence. Canada’s exposure is limited, but this scale of impairment has caused global energy prices to skyrocket, and a risk premium is placed on everything from shipping to government borrowing costs.

The disruption in global energy markets presents an opportunity for Canada to play a role in displacing lost supply, at least in the short-term. As a net energy exporter, higher benchmark oil prices will lead to higher revenues for Canada’s oil and gas sector. With new export capabilities off the west coast, offshore exports of crude oil and natural gas have reached record highs in recent months.

What happens when inflation doesn’t start at home

Most inflation debates start with demand putting upward pressure on the limits of the economy, but inflation can also be driven by supply if the world cannot produce — or ship — what it normally can because of sudden shocks.

The shutdown of a critical global waterway is one example of supply-led inflation. Higher oil prices feed directly into Canadians’ cost of living.

The inflation episode during 2021–2022 was also driven by supply exacerbated by pent-up demand following the pandemic pushing prices higher. This led to increased price sensitivity for Canadians and a hit to their purchasing power.

Supply shocks are more persistent and, critically, they cannot be resolved by rate hikes. Central banks cannot reopen a shipping lane, restore a fertilizer flow or make insurers comfortable with increased global risk; they are limited to interest rate increases to cool demand.

For Canada, the food channel makes this reality especially concrete. Bank of Canada research found that grocery inflation surged in the post-pandemic period largely because of imported cost pressures — with the pass-through into grocery prices taking six to nine months.

Canada does not import inflationary consequences from direct imports of Gulf oil but through global pricing, shipping costs, fertilizer and the grocery aisle. The commodity price spike visible in March is not just an energy story — fertilizer is already up sharply, and that cost will show up in Canadian food prices well into the summer and fall.

How global shocks reach Canadian households

Canada can feel this shock directly in its cost of living. The transmission runs through two channels: Gasoline, immediately and visibly felt at the pump; and food, slower but more persistent. Transportation accounts for 17.3% of Canada’s CPI basket and food for 16.7% — together over a third of what Canadians spend. Within transportation, gasoline alone carries a 3.7% weight, large enough that an energy shock moves headline inflation fast, even before it reaches the grocery aisle. Potential labour disruptions in rail and port logistics add a domestic layer on top; when those networks tighten, the pass-through into prices accelerates further.

Gasoline

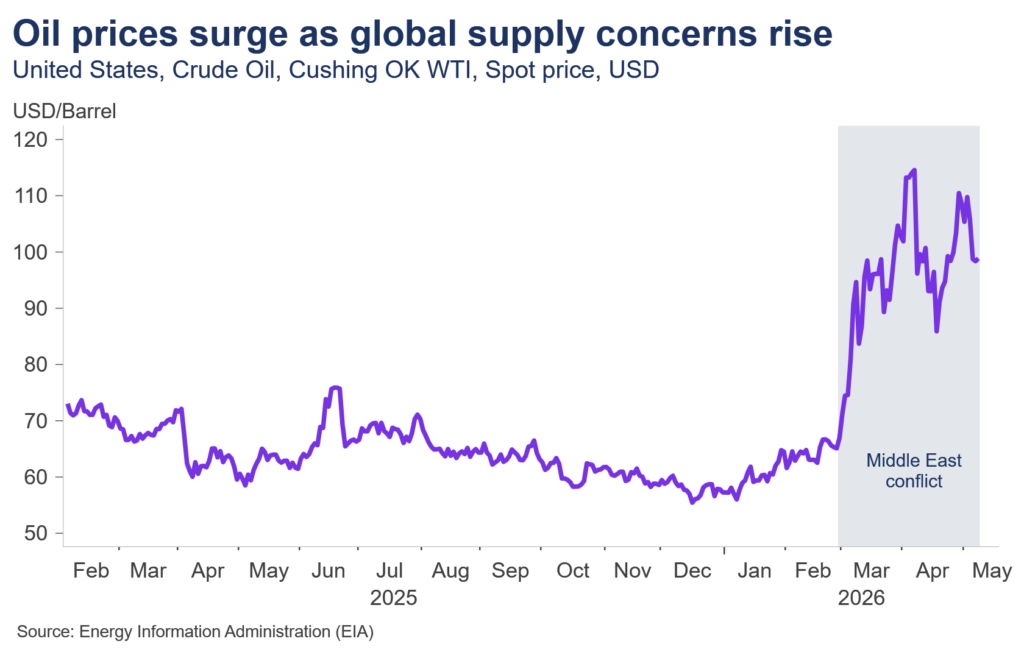

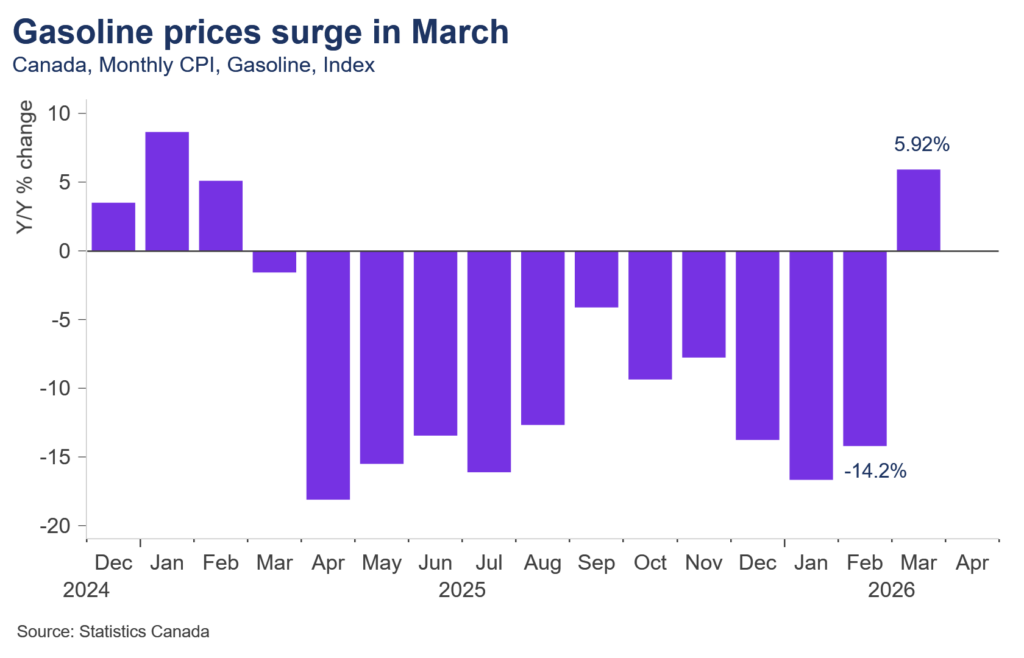

Canadian inflation in March rose to 2.4% year-over-year, up from 1.8% in February, driven explicitly by energy prices. As the WTI chart shows, benchmark crude surged from around $60 in late 2025 to over $100 in March 2026 — a rise of almost 70% in the weeks following the onset of the conflict. That crude price shock fed directly into Canadian pump prices, which posted the largest monthly price increase on record at +21.2% month-over-month. The year-over-year gasoline reading of +5.9% understates the shock’s severity as it reflects the fact that prices were already somewhat elevated a year ago; the monthly figure is the truer signal.

Food

Food inflation has been stubbornly above headline for over six months. In March, food prices remained elevated, with fresh vegetables up nearly 8% — the steepest rise since August 2023, as import supply tightened. With fertilizer prices also being impacted, the effects are likely not over and will probably feed into food prices in the fall.

Believing it makes it real

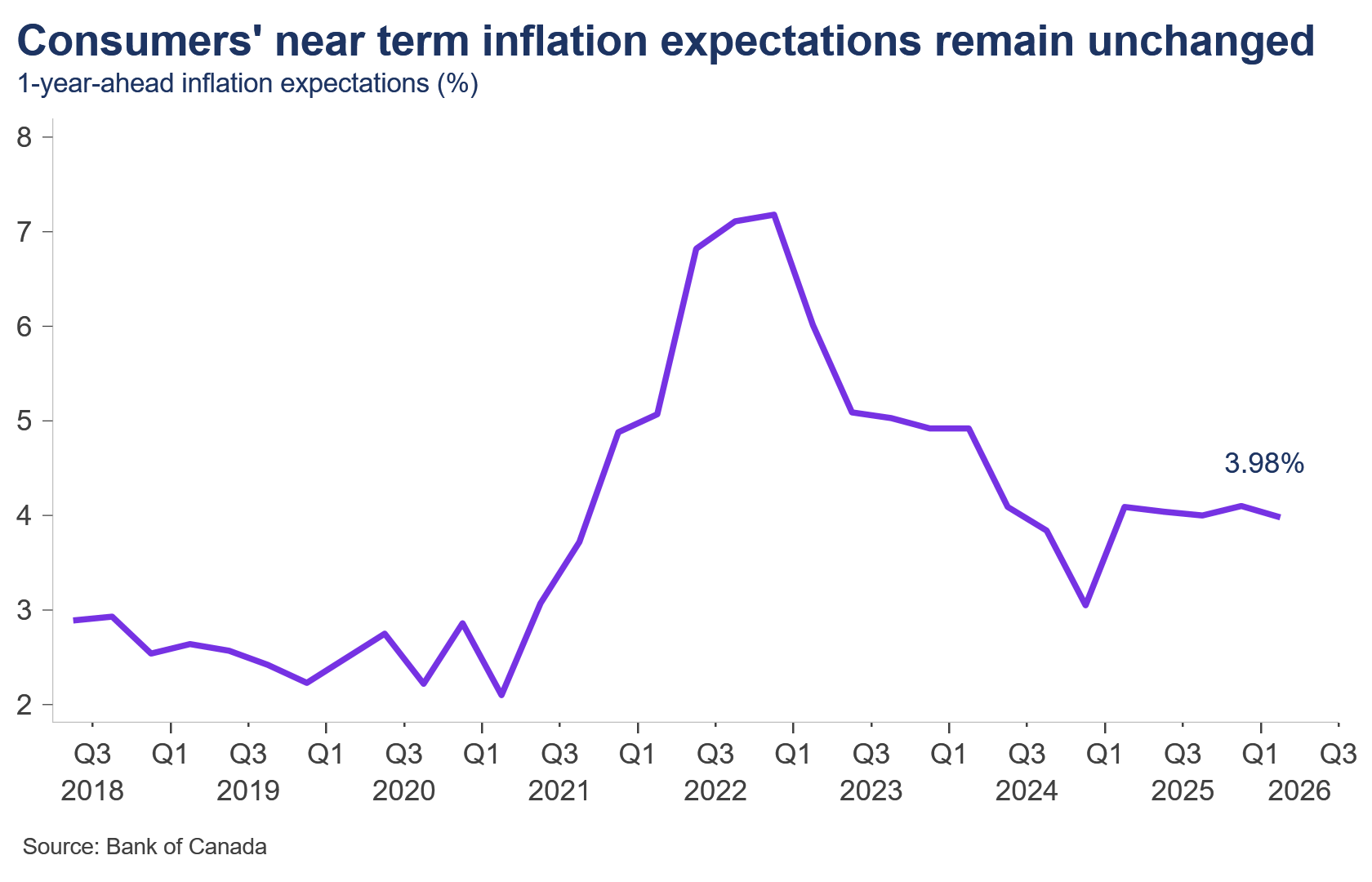

First-quarter survey data from the Bank of Canada shows consumers’ one-year-ahead inflation expectations still stand at nearly 4%. This matters beyond the basket arithmetic: When households expect higher inflation; they demand higher wages to offset the additional costs. Businesses have higher operational costs and pass it along to consumers. That is how a supply shock becomes entrenched. Gasoline prices are the most visible price signal in the economy, and right now they are telling Canadians that inflation is coming back.

The bill is coming due

The BDL estimated* that gasoline alone would add 0.7 to 0.9 percentage points to headline CPI in a short disruption. If the disruption extends beyond six months, the combined gasoline-and-food impact may reach 1.5 to 2 percentage points, as fertilizer, shipping and imported food costs continue working through the grocery aisle over the coming months.

The global backdrop reinforces the concern. The International Monetary Fund’s (IMF) April 2026 World Economic Outlook cut global growth to 3.1% for 2026, down from 3.4% in 2025. Canada is expected to grow 1.5% this year, with Asia’s largest economies, Japan (0.7%) and China (4.4%), bearing the sharpest downgrades given their direct exposure. Applied to the current shock using the IMF’s rule of thumb**, BDL estimates global inflation to increase by 1.3–2.1% and GDP to take a hit of –0.5 to –0.8% under the assumption that Brent crude oil prices remain between $95–110.

The Bank of Canada faces an uncomfortable position with growth already under pressure from elevated U.S. trade uncertainty. A supply-led inflation spike could force it to hike rates, even as the economy slows — the classic stagflationary trap that monetary policy is least equipped to resolve. It can suppress demand, but it cannot fix supply.

Resilience is not optional

Supply shocks are no longer rare events and are increasingly driven by geopolitics rather than market cycles. This moment is a reminder that resilience is not optional and treating supply chains as a core national priority means investing in export capacity, securing critical inputs like fertilizer, diversifying food supply sources, and coordinating internationally to respond to disruptions in real time.

Notes:

*Canada CPI calculated through two channels:

- Gasoline: oil shock × 53% (crude-to-pump factor (NRCan/MJ Ervin)) × 3.71% basket weight (StatsCan 2025).

- Food: oil shock × 14% (pass-through to food) × 16.72% basket weight based on 2022 precedent where +84% fertilizer led to +11.4% food CPI over 26 weeks (StatsCan Table 18-10-0004-01).

**IMF Rule of Thumb: Every 10% rise in oil prices adds +0.4 pp to global inflation and subtracts –0.15% from global output. Applied to the current shock, BDL estimates a base-case disruption (Brent $95–110) implies +1.3 to 2.1% added global inflation and –0.5 to –0.8% GDP drag.

Other Blogs

Inflation cools ahead of the summer months

The Bank of Canada gains more confidence in growth prospects despite inflation risk

Canada’s labour market finally caught a bit of a break in June: Labour Force Survey May 2026

Record Exports Signal a Broader Trade Story: Merchandise Trade May 2026

Canada’s economy starts the second quarter with firmer footing

The Inflation Gap Widens as Price Pressures Spread Beyond Energy: May 2026 CPI

Consumers Keep Spending, but the Menu Is Narrowing

The Bank of Canada faces a dilemma as it extends its holding pattern