A Solid Start, but Signs of Fatigue Emerging

Retail Sales February 2026

Jasleen Trehan

Share:

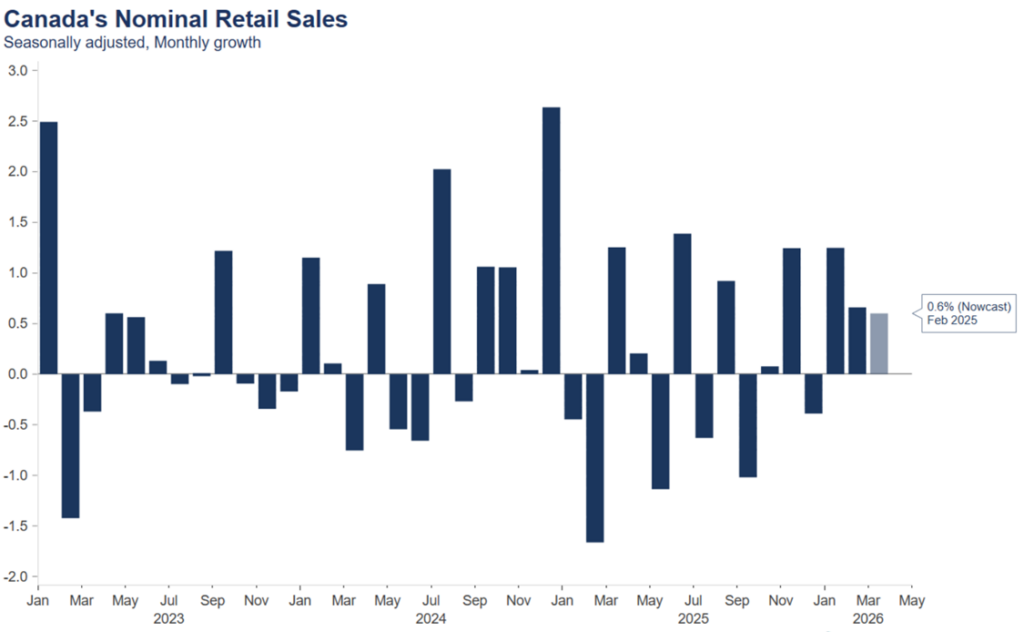

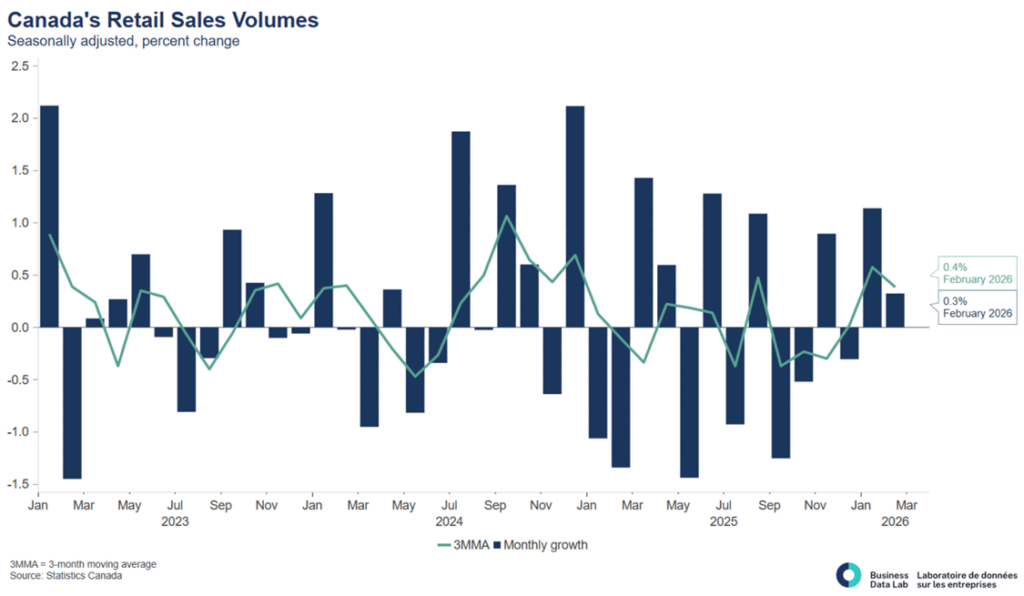

Retail sales rose 0.7% in February, marking a second straight monthly gain — but momentum is slowing. With volumes up just 0.3%, this is a consumer that’s staying afloat, not pushing ahead. The strength remains concentrated in autos, while core spending rose a modest 0.6%, suggesting underlying demand is steady rather than strong. Even with a rebound in grocery spending, the broader pattern is one of stabilization, not acceleration.

What’s becoming more important is the widening gap between nominal and real spending. As price pressures pick up, especially from energy, headline sales are increasingly overstating the true health of the consumer. Overall, the first quarter still looks resilient. But that resilience is starting to wear thin, and with a softer labour market and rising cost pressures, the outlook beyond that is becoming increasingly uncertain.

Key Takeaways

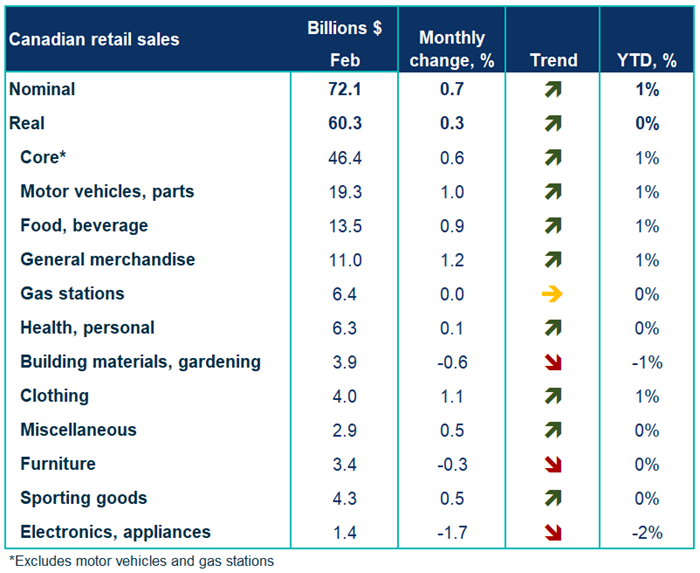

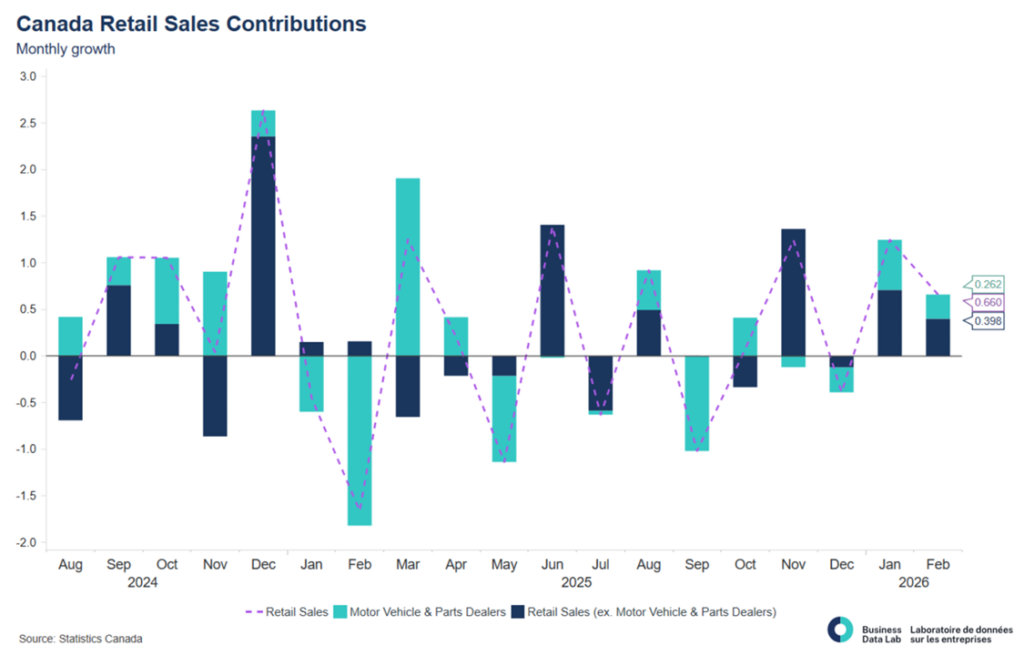

- Overall performance: Retail sales rose 0.7% m/m to $72.1B in February, with real (volume) sales up just 0.3%, marking a clear step-down from January’s pace. While core retail sales rose 0.6%, the modest volume gain suggests that much of the strength remains nominal rather than reflecting a meaningful pickup in real consumption. Taken together with January, household spending held up through Q1 — but the slowing momentum points to a consumer that is stabilizing rather than strengthening.

- Strengths: Gains were broad-based across seven of nine subsectors, led again by motor vehicle and parts dealers (+1.0%), marking a second consecutive increase. Core categories showed improvement, with general merchandise (+1.2%), food and beverage (+0.9%), and clothing (+1.1%) all advancing. The rebound in grocery sales (+1.6%) suggests some stabilization in essential spending.

- Weakness: The underlying picture remains soft. Volume growth was limited (0.3%), reinforcing the gap between nominal spending and real consumption. Rate-sensitive categories continued to underperform, with building materials (-0.6%) and furniture/electronics (-0.3%) declining — consistent with the ongoing drag from elevated borrowing costs and a weak housing backdrop. Gasoline sales were flat, providing no boost to headline growth despite rising energy price risks, further highlighting the lack of broad-based momentum.

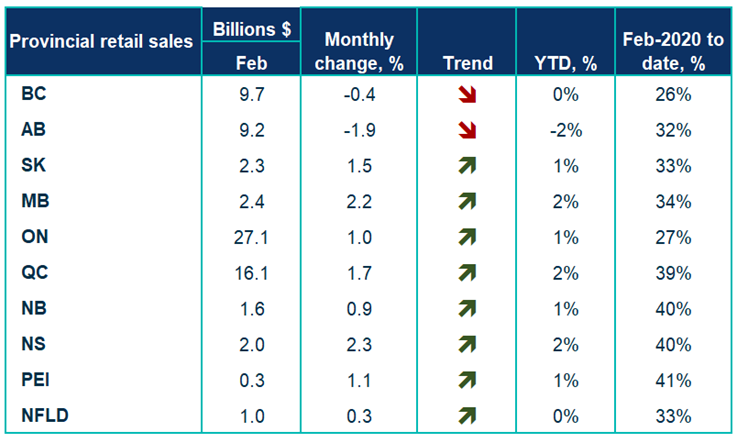

- Regional trends: Sales increased in eight provinces, but the pattern was less synchronized than in January. Ontario (+1.0%) and Quebec (+1.7%) drove much of the growth, supported by autos and core retail, while Alberta (-1.9%) declined, reflecting volatility in vehicle sales and sensitivity to energy-related shifts. This divergence suggests that the rebound in consumer spending is becoming more uneven across regions.

- Advance estimate: StatCan’s advance estimate points to a further +0.6% m/m increase in March, indicating that retail activity likely remained positive through the end of Q1. However, the moderating pace reinforces the view that growth is losing momentum rather than building.

With gains in January and February and another increase signalled for March, retail activity is on track for a solid first quarter, supported in part by earlier price relief and resilient nominal spending. However, the composition of growth and weak volume gains suggest underlying demand remains fragile.

This is consistent with card spending data from BDL’s Business Sales Tracker, which shows that while nominal spending continues to rise, real per-capita consumption is softening — highlighting growing pressure beneath the surface.

As energy-driven inflation pressures amid rising oil prices and Middle East tensions begin to build alongside a cooling labour market, real purchasing power is likely to come under renewed strain, making the outlook beyond Q1 increasingly uncertain.

Tables

Charts

Other Blogs

Canada Needs More Than “Steady”: Key Findings from Business Insights Quarterly (Q1 2026)

Falling employment masks a deeper worry, with full-time jobs being replaced by part-time work: Labour Force Survey April 2025

Price-Driven Surge Pushes Canada Back into Surplus: Merchandise Trade March 2026

Canada’s economy on pace to rebound in the first quarter

The Bank of Canada sees current interest rate “appropriate” despite energy shock.

Use it while you can: The federal government spends its growth-driven fiscal windfall

Inflation rises on energy shock, but underlying price pressures muted.

Sticky hiring, but wage growth at its highest since 2024: Labour Force Survey March 2025