Blog /

Q1 GDP growth offers hope ahead of trade war, despite weak domestic activity.

Canada’s economy grew by 2.2% on an annualized basis in Q1 2025.

Andrew DiCapua

Share:

“Canada’s economy kicked off the year with more momentum than expected, largely due to an anticipated boost from goods trade. But beyond that, there’s not much holding things up domestically. Consumer spending is doing a bit better than anticipated—resilient, yes, but clearly cooling off from previous highs. The housing market remains soft, and big-ticket purchases are being put on hold. That means domestic spending is likely to stay muted in the coming months. Meanwhile, signs of a second-quarter slowdown are already taking shape, especially as U.S. demand for Canadian exports drops off.”

In the first quarter, businesses warned that trade tensions were a problem. Now, they’re painting a much bleaker picture. Even though growth beat the Bank of Canada’s forecast, it’s hard to ignore the underlying weakness. The Bank should move to cut rates by 25 basis points at their next meeting to give the domestic economy a much-needed cushion.”

KEY TAKEAWAYS

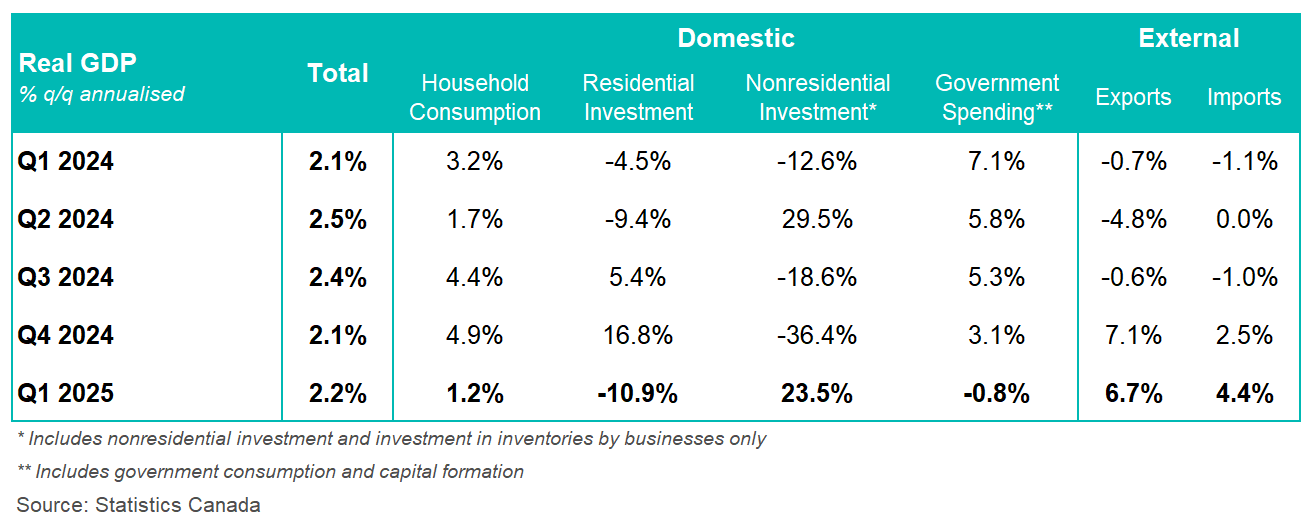

- Canada’s real domestic product (GDP) grew at an annualized rate of 2.2% in Q1 2025—well above the market expectations of 1.7%.

- On a per capita basis, the economy grew by 0.4% in the first quarter.

- March monthly GDP grew by 0.1%, led by a strong oil and gas extraction sector.

- Q4 2024 GDP was revised down from 2.6% to 2.2%.

Exports grew by 1.6% in Q1 as shipments of passenger vehicles and industrial machinery and equipment increased significantly. Offsetting some of the gains were lower exports of crude oil and refined energy products. Imports increased 1.1%, which put the net trade position in a decent position.

Household spending though decreased from a strong Q4 2024, grew by 0.3% in Q1. This was mainly due to rental fees, with spending on passenger vehicles down. On a per capita basis, household consumption increased a merely 0.1%.

Residential investment reversed progress from the fourth quarter, declining 2.8% in Q1 as the resale market experienced weaker demand. Business investment was mixed, declining overall 1.6%. Machinery and equipment investment grew 5.3% with every category advancing, which is a strong sign despite trade tensions chilling other investment activity. Nonresidential investment grew a healthy 5.8%, reversing a downward trend.

Inventories were largely built up in the durable goods wholesale sector.

OUTLOOK AND IMPLICATIONS

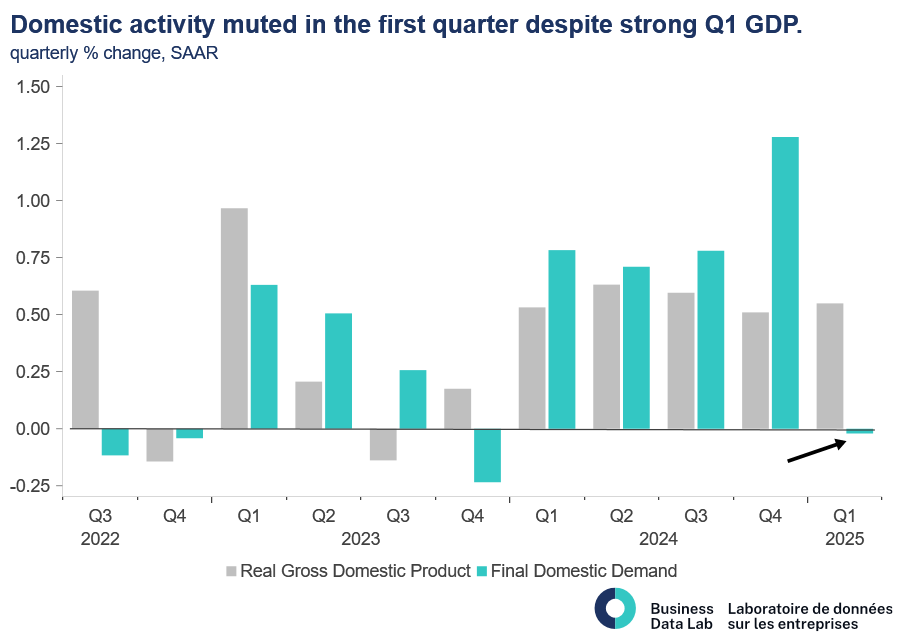

The Canadian economy hasn’t tumbled yet, despite significant uncertainty from U.S. tariffs. Overall GDP growth of 2.2% is above the Bank of Canada’s Q1 expectation of 1.75%. Statistics Canada estimates that April GDP is expected to grow 0.1%, initial signs that tariffs have yet to impact growth. This combined with better economic data from the U.S., provides some optimism that U.S. consumer demand will support Canadian exports. Final domestic demand was flat in Q1, with underlying weakness on the back of a weaker handoff from Q4 2024 (revised down to 2.2%).

Markets are expecting the Bank of Canada to hold interest rates at their June 4 meeting. Although we believe that the Bank should continue to lower its policy rate amid weak fundamentals, they are more likely to hold interest rates and resume cuts at their July meeting.

Other Blogs

Consumers Return to the Checkout with Broader Spending

Inflation cools ahead of the summer months

The Bank of Canada gains more confidence in growth prospects despite inflation risk

Canada’s labour market finally caught a bit of a break in June: Labour Force Survey May 2026

Record Exports Signal a Broader Trade Story: Merchandise Trade May 2026

Canada’s economy starts the second quarter with firmer footing

The Inflation Gap Widens as Price Pressures Spread Beyond Energy: May 2026 CPI

Consumers Keep Spending, but the Menu Is Narrowing