Pivot or Peril: Are Canadian Cities Diversifying or Doubling Down on America?

Canada’s trade diversification story is real but uneven. New localized data shows which cities are expanding trade with global markets and which remain most economically vulnerable to U.S. trade disruptions.

Patrick Gill and Jasleen Trehan

Share:

Canada’s trade story is changing.

Over the past year, Canadian exports have begun to shift away from the United States toward global markets. At the national level, this looks like progress — a long-discussed move toward diversification finally taking hold.

But the story is more complicated.

This shift toward diversification is not broad-based or being driven by new exporters or evenly distributed across the country. It is concentrated in a handful of firms, sectors and cities — leaving many parts of the economy still highly exposed to U.S. trade policy risk.

A year after tariffs and trade barriers: Exposure is translating into impact

Last year, the Business Data Lab (BDL) showed that U.S. tariffs and trade risks would not affect Canada evenly. Some cities, particularly those deeply integrated into U.S. supply chains, were far more exposed than others.

Which Canadian Cities are Most Exposed to U.S. Tariffs

Saint John, Calgary and Windsor topped that list of Census Metropolitan Areas (CMAs), reflecting the cross-country vulnerability. A year later, that exposure is seemingly showing up in economic outcomes locally, although it was not an exact match with who we expected could have been worst hit.

As expected, Canadian cities with greater exposure to U.S. trade are experiencing more local economic stress. Cities that are more dependent on the U.S. market are generally recording weaker trade performance, softer consumer spending, slower employment growth and lower business confidence, while more diversified economies are proving more resilient.

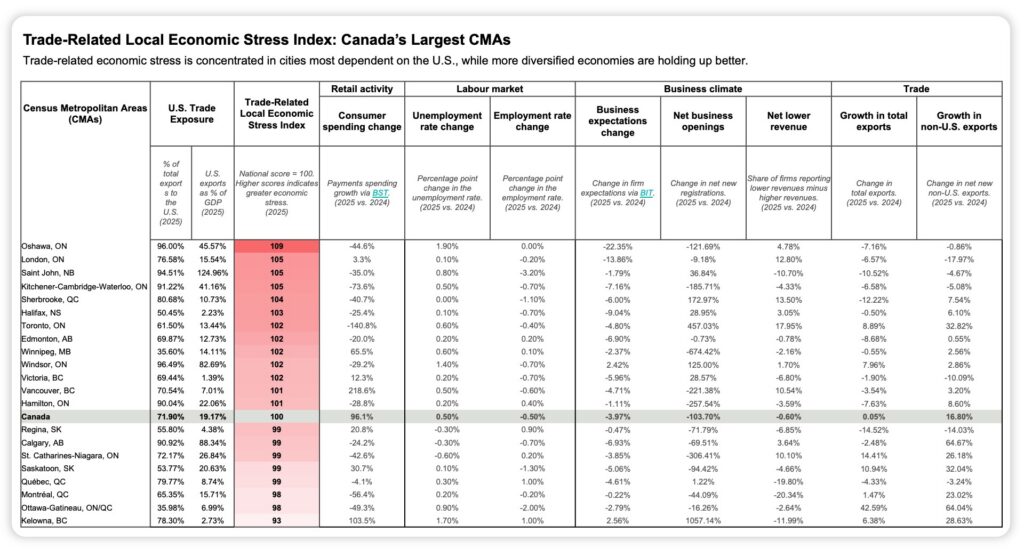

Where is trade-related economic stress springing up?

Notes: The Index equally weights standardized (z-score) changes in consumer spending, labour market conditions and business activity across CMAs (2025 vs. 2024). Higher values indicate greater trade-related local economic stress.

What looks like diversification is actually concentration

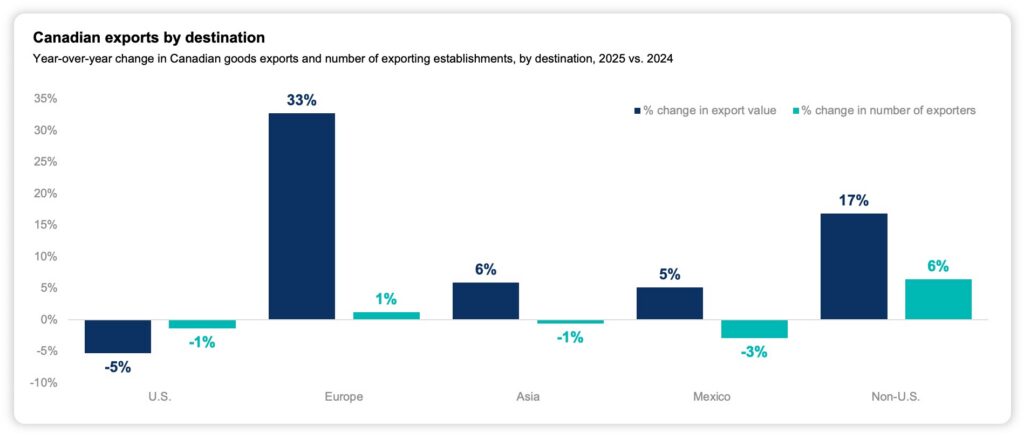

At the national level, exports to the U.S. declined between 2024 and 2025, while exports to the rest of the world increased sharply. On paper, this looks like a meaningful shift toward diversification. But the underlying structure of Canada’s trade economy is changing less than the headline numbers suggest. Canada’s export diversification is real, but – as mentioned – it is generally being driven by a concentrated group of firms, sectors and cities.

Export growth outside the U.S. is being driven primarily by existing exporters doing more, not by a broad expansion in the number of businesses exporting internationally.

Canada’s trade diversification is being driven by existing exporters doing more, not more firms exporting.

Note: Exporter counts reflect the number of establishments reporting exports; changes may reflect both market conditions and reporting thresholds.

Much of the growth in non-U.S. exports is concentrated in a relatively small number of CMAs:

- Toronto has seen one of the largest increases in exports to non-U.S. markets, reflecting both scale and sector diversity, broader economic conditions and trade-sensitive industries weighing on local performance.

- Calgary and Ottawa–Gatineau are showing some of the strongest gains in non-U.S. exports, suggesting parts of their trade base are becoming less reliant on the U.S. market.

- Montreal and Saskatoon are also recording solid growth in exports to global markets, supported by manufacturing, agriculture and commodity-linked activity.

- St. Catharines–Niagara and Kelowna have posted notable gains in exports outside the U.S., despite differing economic makeups.

Together, this relatively small group of cities account for a disproportionate share of Canada’s recent export diversification gains, reinforcing how uneven the country’s trade adjustment remains across regions.

Meanwhile, many other CMAs are not seeing the same shift. Several major CMAs, particularly highly U.S.-integrated manufacturing regions in Ontario, continue to face weaker overall trade performance and limited diversification momentum.

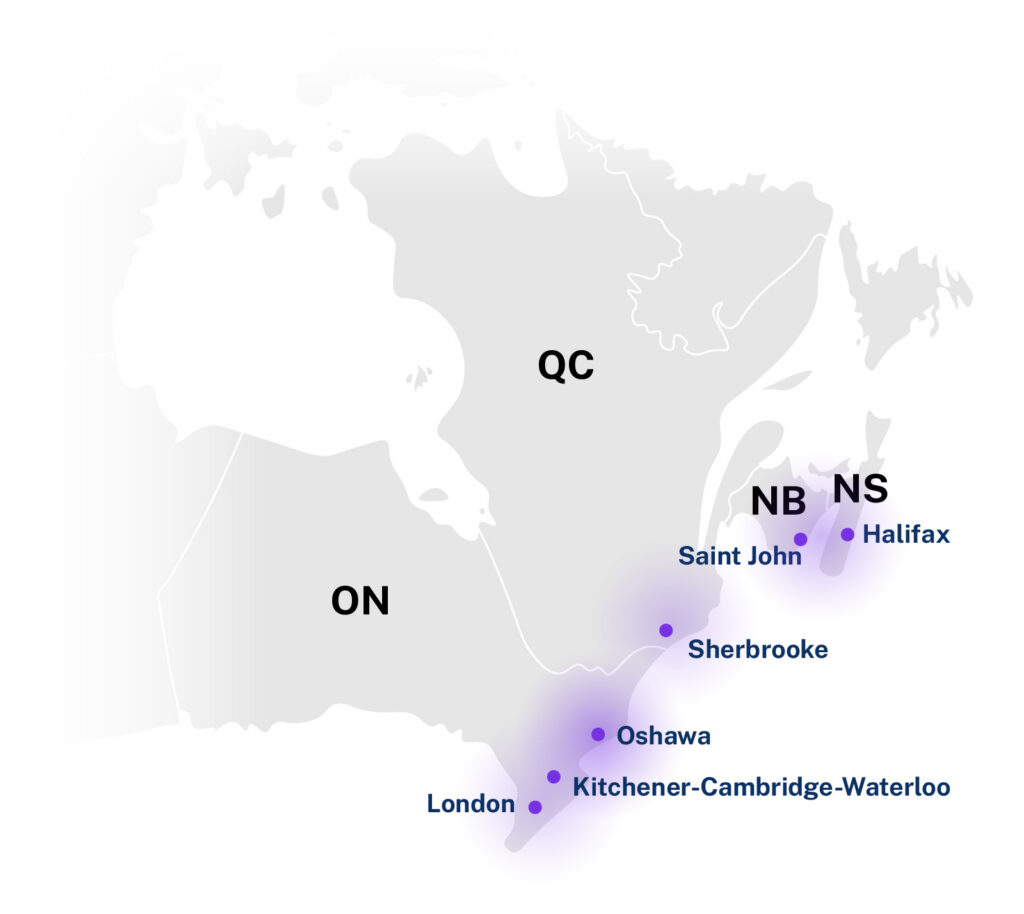

Top CMAs facing trade-related economic stress

Highly U.S.-integrated manufacturing regions, including Oshawa, London and Kitchener-Cambridge-Waterloo, are showing some of the clearest signs of trade-related economic stress. These cities remain heavily tied to the U.S. market, while growth in exports outside the U.S. has been limited or insufficient to offset broader weakness in trade activity and local economic conditions.

More broadly, the data points to a growing divergence in local trade performance across Canada. Some cities are successfully expanding into global markets and building more diversified export bases, while others remain more exposed to U.S. demand, trade disruptions and policy uncertainty.

Why is Canada’s trade diversification still so concentrated?

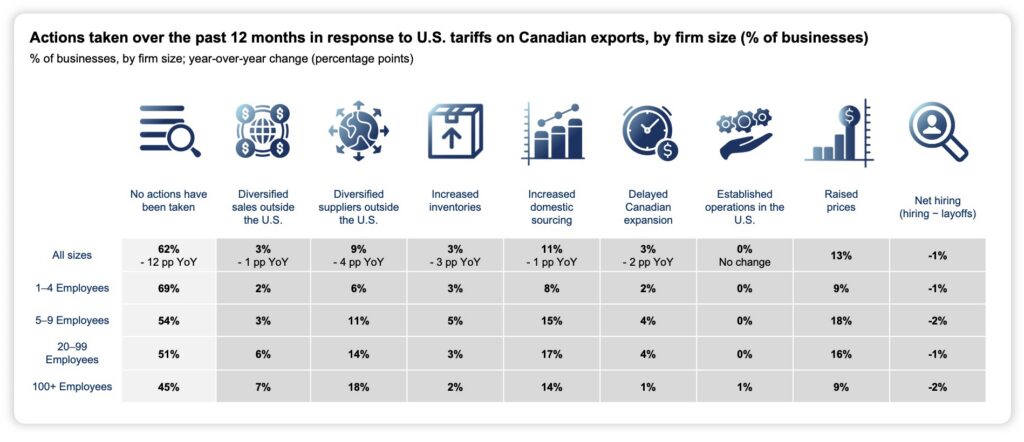

Recent Statistics Canada data on business responses to U.S. tariffs suggests many Canadian firms are adapting cautiously rather than fundamentally repositioning their operations. While fewer businesses report taking no action compared to a year ago, relatively few are actively diversifying sales or suppliers outside the U.S. Instead, firms are more likely to be raising prices, increasing domestic sourcing or delaying expansion plans.

Are businesses betting on a return to normal with the U.S.? This data suggests many businesses still expect Canada–U.S. trade conditions to eventually stabilize and return closer to the pre-tariff status quo, despite growing signs that the global trading environment is becoming more fragmented and less predictable. Such an attitude stands in contrast to Prime Minister Mark Carney’s recent warnings that the world is undergoing “a rupture, not a transition” and that the old model of deep economic integration can no longer be taken for granted.

The risk is that Canadian firms may be underinvesting in longer-term diversification at precisely the moment when resilience and market expansion are becoming more important to competitiveness and growth.

If Canada wants diversification to become structural, more firms — especially SMEs — will need to participate in global trade.

A year after “Liberation Day,” inaction is falling, but firms are raising prices instead of diversifying.

Diversification will require a broader exporter base

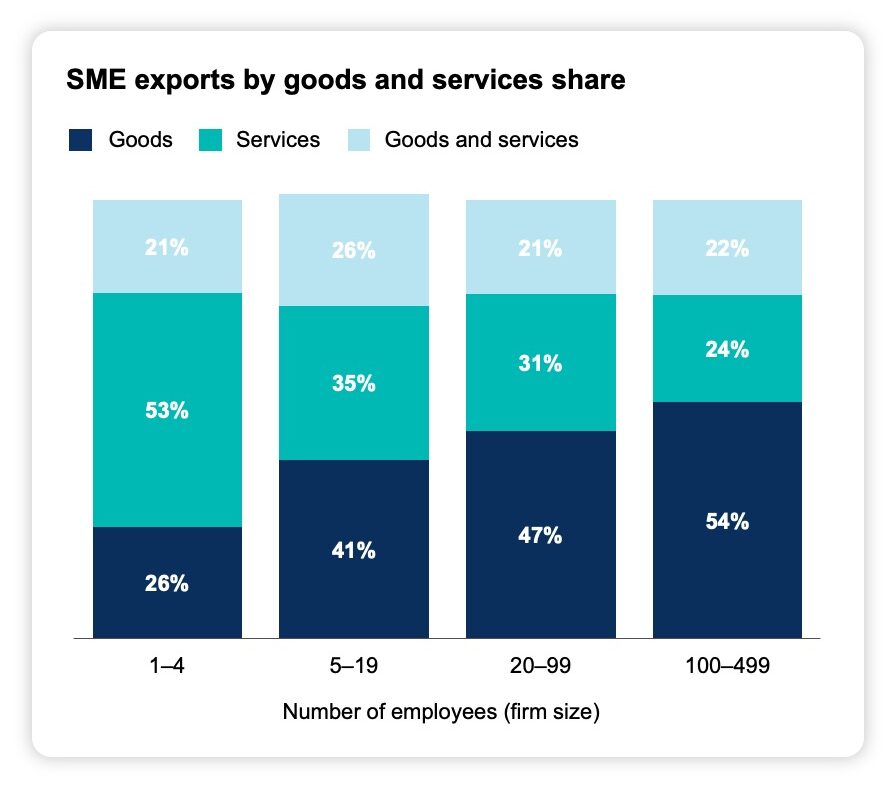

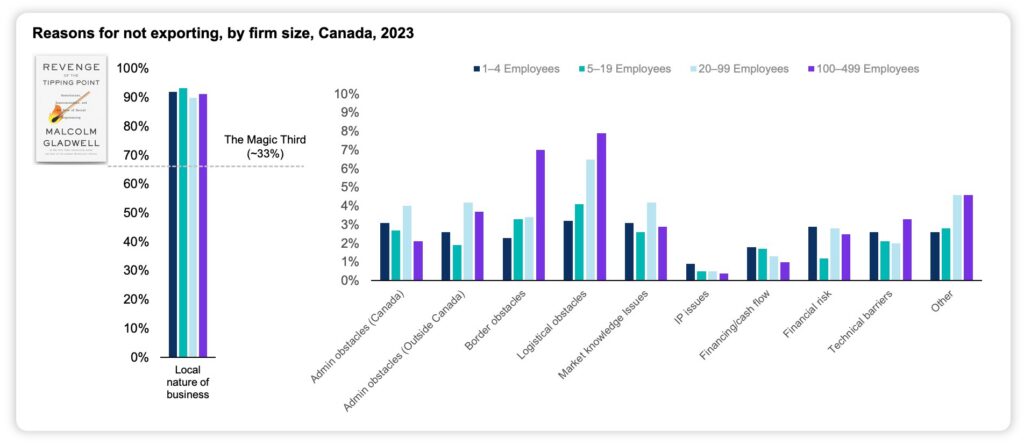

Canada already has a sizeable base of SME exporters, and export participation rates have been gradually rising across firm sizes over the past decade, including among micro firms (1–4 employees). Yet roughly 90% of non-exporting businesses still describe their operations as “local” in nature, even though many may produce goods or services with international potential.

This matters because many of the traditional barriers to exporting — distance, logistics and scale — are becoming less restrictive in parts of the global services economy. While goods exports have weakened recently, services exports continue to grow, and smaller firms are already disproportionately represented in services trade.

Canada’s diversification challenge, therefore, is not just about market access or geography. It is also about helping more businesses see global growth as achievable and increasingly necessary in a more fragmented global economy.

SMEs can help lead trade diversification in services.

The domestic comfort trap: ~90% of non-exporters see their business as local.

Moving even ~20% more SMEs toward export ambition could push the system toward a critical mass.

Sources: BDL analysis. Statistics Canada, Survey on Financing and Growth of Small and Medium Enterprises (2023).

What this means for businesses and policymakers

Trade conditions are likely to remain more volatile, more uncertain and more uneven than in the past. The ability to adapt increasingly depends on where firms operate, what they produce and how dependent they are on a single market.

Canada’s recent export adjustment is real, but it is not yet broad-based. Much of the country’s diversification progress is still being driven by a concentrated group of firms, sectors and cities — leaving many businesses and local economies exposed to U.S. demand and trade policy risk.

For policymakers, the findings reinforce the importance of helping more Canadian businesses scale internationally and compete in a wider range of markets. Canada does not just need more trade — it needs more traders, which means helping more firms break out of the “domestic comfort trap” and better understand where global demand for Canadian goods and services already exists.

To support that effort, the Business Data Lab is developing a new trade diversification tool that will help Canadian businesses identify international market opportunities and better understand where their products may be competitive globally. Because in a more fragmented global economy, diversification is no longer just a growth strategy. It is increasingly a resilience strategy.

Other Blogs

Where Canada’s defence debate goes next

Retail sales defy expectations, but spending may be running out of gas.

Inflation becoming more of an isolated energy story, for now : April 2026 CPI

Narrow Strait, Wide Impact: How a Global Shock Reaches Canada

Canada Needs More Than “Steady”: Key Findings from Business Insights Quarterly (Q1 2026)

Falling employment masks a deeper worry, with full-time jobs being replaced by part-time work: Labour Force Survey April 2025

Price-Driven Surge Pushes Canada Back into Surplus: Merchandise Trade March 2026

Canada’s economy on pace to rebound in the first quarter