Retail Sales November 2025

Discounts lift spending, not confidence

Jasleen Trehan

Share:

“November’s 1.3% rebound in retail sales shows consumers stepping back into the market but cautiously and selectively. Discounting lifted spending in food and everyday categories, while autos remained soft and e-commerce pulled back. Core sales improved, yet our Business Sales Tracker shows year-over-year card spending growth continuing to slow. With headline inflation ticking higher but underlying price pressures continuing to ease, and labour market momentum softening, the Canadian consumer remains resilient but constrained, a view reinforced by StatCan’s advance estimate pointing to a pullback in December, underscoring that recent strength is unlikely to mark a sustained acceleration in demand.”

Key Takeaways

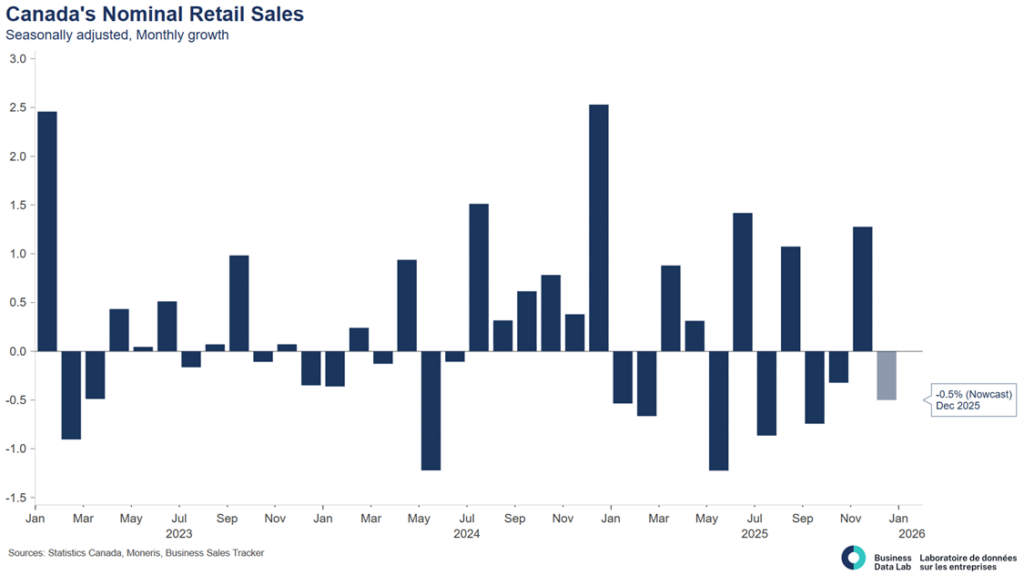

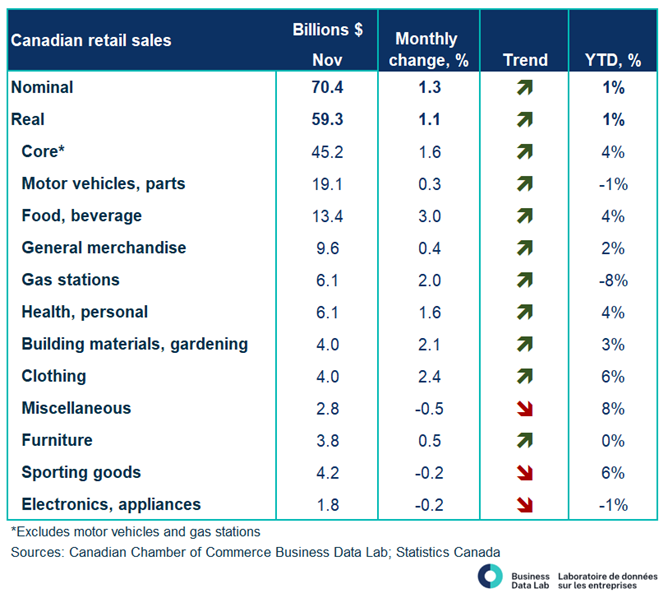

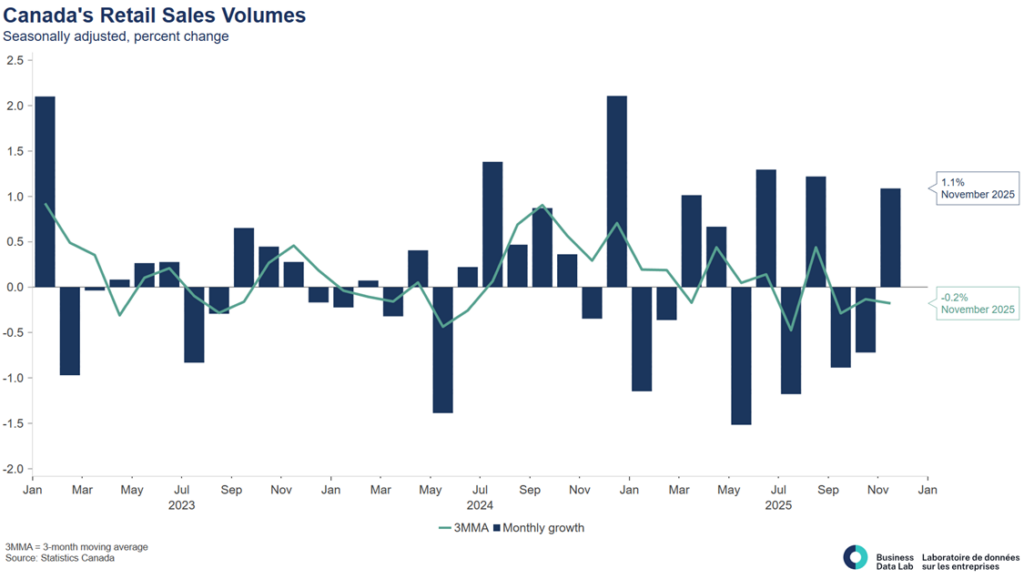

- Overall performance: Retail sales rose 1.3% m/m to $70.4B in November, snapping two months of declines. Real (volume) sales increased 1.1%, while core retail sales (ex-autos and gasoline) climbed a stronger 1.6%, pointing to a rebound concentrated in non-durable and everyday categories rather than a broad-based upswing in discretionary demand.

- Strengths: Food and beverage retailers led the gain, up 3.0% m/m, supported by grocery sales and a rebound in beer, wine and liquor following October labour disruptions. Clothing (+2.4%) and health & personal care (+1.6%) also improved, consistent with seasonal promotions drawing cautious consumers back into stores. However, BDL’s Business Sales Tracker shows nominal card spending growth easing steadily from 4.25% y/y in September to 3.46% in November signaling that headline retail strength is increasingly promotion-led rather than demand-driven.

- Weakness: Motor vehicle and parts dealers remained a drag, posting only a modest 0.3% gain and continuing to underperform year over year as higher borrowing costs weigh on big-ticket purchases. E-commerce sales fell 2.8% m/m, reinforcing that discretionary spending remains under pressure outside of discount periods. Building materials rose again (+2.1%), but gains remain modest and consistent with maintenance-related activity rather than a housing-led rebound.

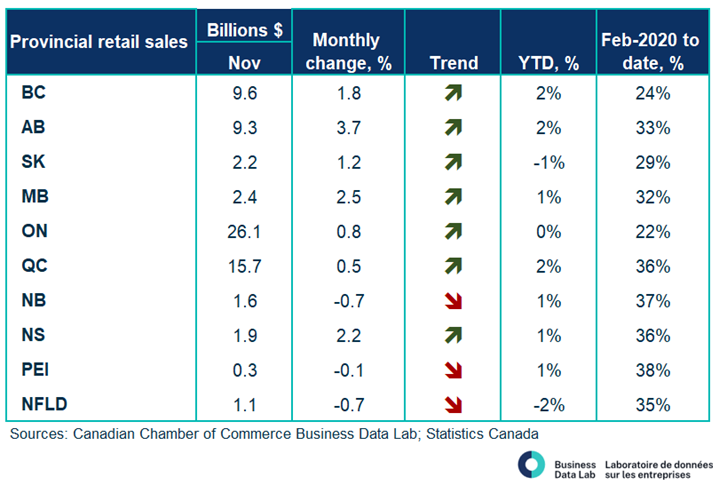

- Regional trends: Sales increased in seven provinces, led by Alberta (+3.7%). Ontario posted a modest 0.8% gain, with Toronto up 0.9%, while New Brunswick (-0.7%) was the weakest performer. Overall, provincial results continue to reflect uneven demand shaped more by population growth and necessities than broad discretionary strength.

- Advance estimate: StatsCan’s advance estimate points to a 0.5% decline in December, aligning with Business dales tracker data showing year-over-year spending growth slowing sharply to 1.78% in December.

November’s retail rebound was real, but it was deal-driven, not confidence-driven. Canadian consumers are still spending, but increasingly around necessities and discounts rather than big-ticket or discretionary purchases. With labour market momentum cooling and demand still fragile, consumer spending is likely to recover only gradually in 2026, offering stability but not a strong growth impulse for the broader economy.

Tables

Charts

Other Blogs

Inventory drawdown causes GDP to knee jerk into contraction despite improving fundamentals.

Momentum stalls as consumer shifts into a lower gear: Retail Sales December 2025

Diversification Gains Traction as Exports Close the Year Stronger: Merchandise Trade December 2025

6 Predictions for the Canadian Economy in 2026

Conflicting signals as both unemployment and employment rate declines: Labour Force Survey December 2025

Canada’s Productivity Gap Is a Vulnerability We Must Fix

Weak economic momentum could spell fourth quarter contraction.

Gold Payback and Auto Tariffs Push Canada Back into Deficit: Merchandise Trade November 2025