Blog /

Retail Sales June 2025: Broad-based rebound as core sales strengthen

Quarterly momentum improved: Q2 retail sales rose 0.4% in nominal terms and 0.7% in volume—an improvement on Q1’s softer profile—signaling a firmer goods-consumption lift to Q2 GDP, though the July advance estimate points to a muted start to Q3.

Jasleen Trehan

Share:

“Canadian retail sales strengthened in June, with gains spanning every major subsector and real spending moving higher—clear evidence of momentum. Core categories led the improvement as food held up and discretionary items firmed, while earlier drags faded with gasoline recovering and autos stabilizing. With fewer retailers citing trade-tension headwinds and a modest tilt back toward in-store shopping, the goods backdrop looks healthier—even as early signals point to some giveback in July.”

Key Takeaways

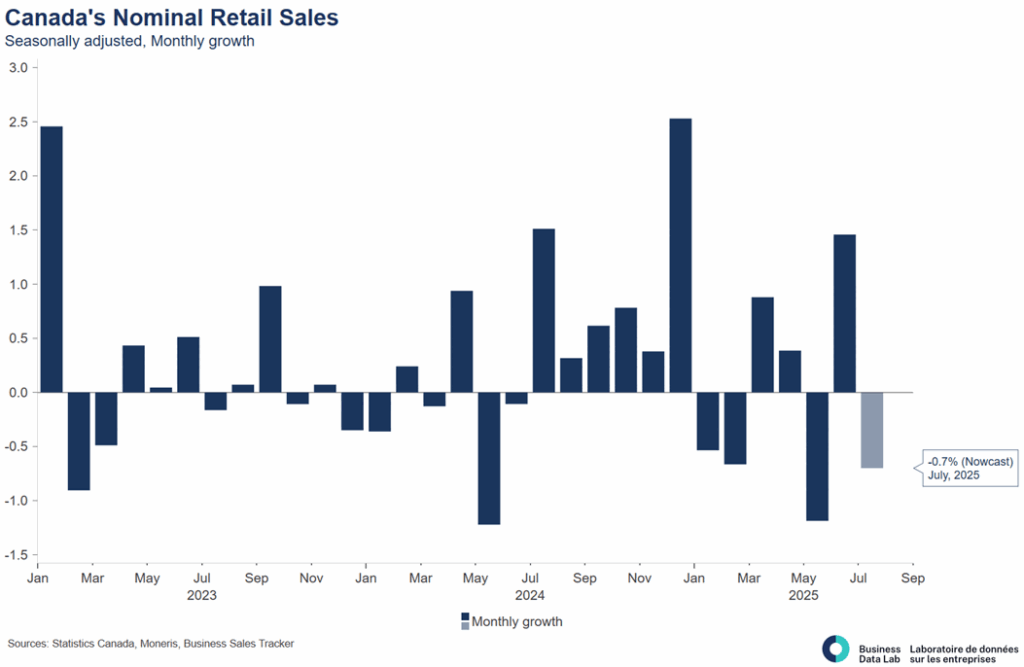

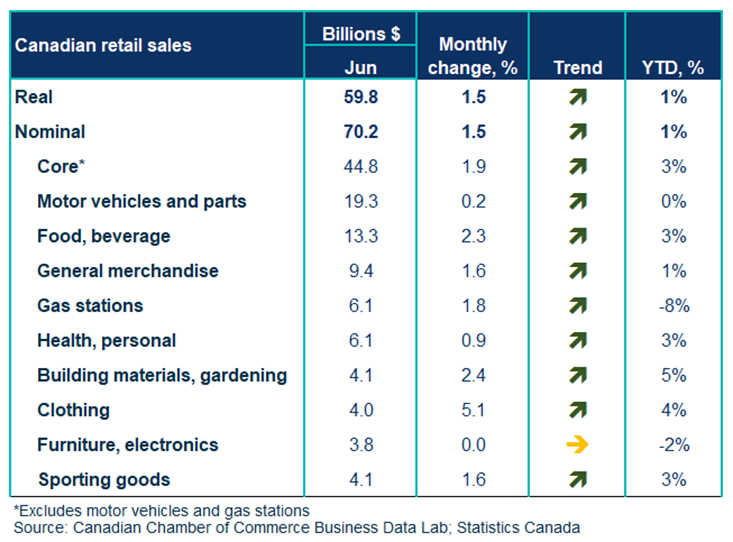

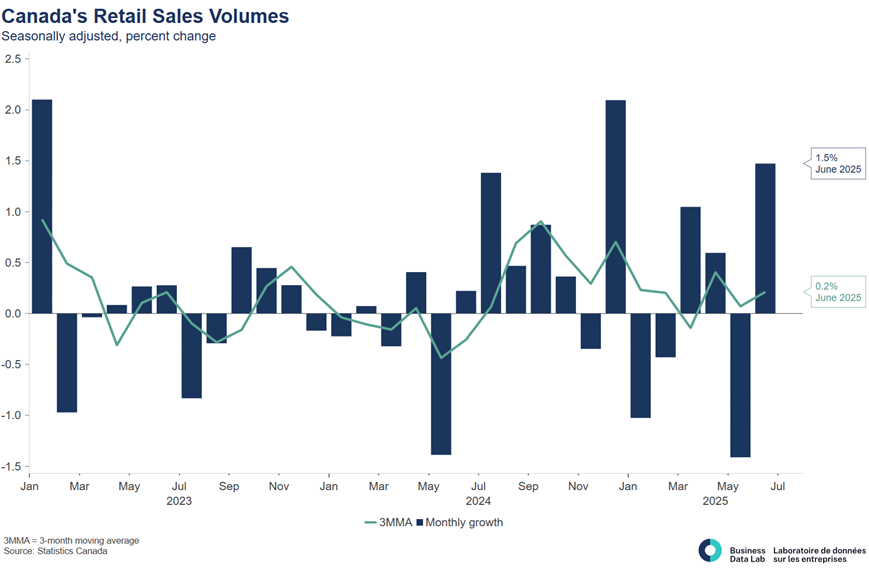

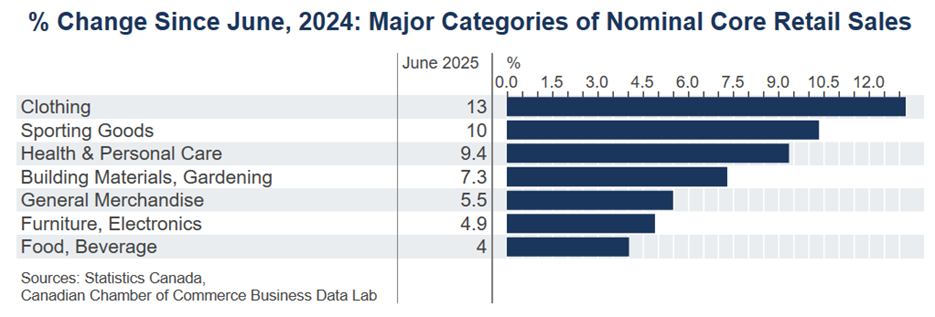

- Overall performance: Retail sales rose 1.5% m/m to $70.2B, with all nine subsectors advancing. Volumes also rose 1.5%, indicating real; not price-driven-gains. Core sales (ex-autos and fuel) increased 1.9%, underscoring breadth beyond energy and vehicles.

- Quarterly momentum improved: Retail momentum firmed in Q2, real retail sales +0.7% q/q (vs. +0.2% in Q1) pointing to a stronger goods-consumption lift to Q2 GDP, while nominal eased to +0.4% (vs. +1.2% in Q1) amid softer prices.

- Breadth beyond essentials: Core sales rose 1.9%, and overall, all nine subsectors advanced, led by food & beverage (+2.3% m/m) (grocers +1.8%, beer/wine/liquor +4.3%, convenience & vending +5.3%). Discretionary outlays firmed (clothing & accessories +5.1%, general merchandise +1.6%). Earlier drags eased: gasoline stations +1.8% (volumes +2.7%) and motor vehicle & parts +0.2% (new cars +0.1%, used +0.7%, parts & tires +1.1%). Building materials and garden equipment +2.4% m/m, consistent with recent firmness in home resales and housing starts, hinting at improving residential investment momentum.

- Pockets of softness, not a pullback: E-commerce −1.7% to $4.2B, trimming its share to 5.9% (from 6.1% in May). Within stores, declines were narrow: furniture −1.8%, other motor-vehicle dealers −0.1%, Jewellery/luggage/leather −0.1%. Netting these against widespread gains leaves June consistent with normalization rather than renewed weakness.

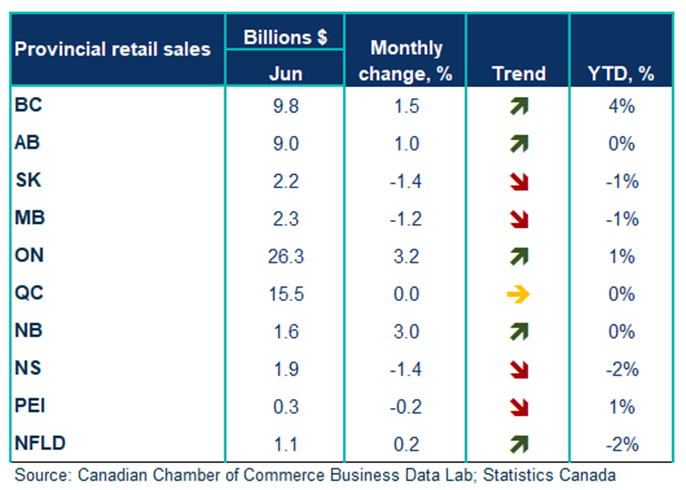

- Regional patterns were mixed but not weak: Sales rose in six provinces, led by Ontario (+3.2%) and New Brunswick (+3.0%). Declines in Saskatchewan (−1.4%) coinciding with wildfire evacuations along with Nova Scotia (−1.4%) and Manitoba (−1.2%) tempered the aggregate; Quebec was flat. The pattern points to localized shocks rather than a national demand rollover.

- Trade-tension lens: The share of retailers citing Canada–US trade-tension impacts fell to 27% in June (from 32% in May), signaling a marginal easing of price, demand-shift, and supply-delay headwinds.

- July giveback likely: Looking ahead, Statistics Canada’s -0.8% m/m advance estimate for July (broadly in line with -0.7% forecast), suggests Q3 consumption may be muted unless subsequent months firm.

Tables

Charts

Other Blogs

Inventory drawdown causes GDP to knee jerk into contraction despite improving fundamentals.

Momentum stalls as consumer shifts into a lower gear: Retail Sales December 2025

Diversification Gains Traction as Exports Close the Year Stronger: Merchandise Trade December 2025

6 Predictions for the Canadian Economy in 2026

Conflicting signals as both unemployment and employment rate declines: Labour Force Survey December 2025

Canada’s Productivity Gap Is a Vulnerability We Must Fix

Weak economic momentum could spell fourth quarter contraction.

Gold Payback and Auto Tariffs Push Canada Back into Deficit: Merchandise Trade November 2025