Blog /

Q2 GDP sees exports fall off a cliff, while domestic economy holds ground.

Canada’s economy contracted by 1.6% on an annualized basis in Q2 2025 as the U.S. tariffs slam exports.

Andrew DiCapua

Share:

“The Canadian economy experienced a significant export shock in the second quarter as the receipts from the trade war were totalled up. This hit to growth also showed up in weak investment numbers that confirm the sentiment that businesses continue to wait for more clarity. The rebound in domestic final demand is a sign that there remain decent consumer spending humming beneath the surface. This result is weaker than the Bank of Canada was expecting and will certainly put a heavy hand on the Governing Council to resume interest rate cuts at their September meeting.”

KEY TAKEAWAYS

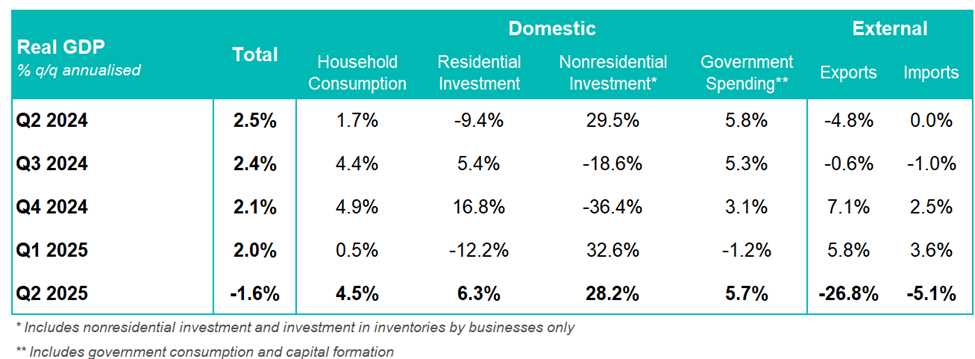

- Canada’s real domestic product (GDP) contracted at an annualized rate of -1.6% in Q2 2025, below economist expectations of -0.7% and the Bank of Canada’s July forecast (-1.5%).

- On a per capita basis, GDP reversed course, declining by -0.4% in the second quarter.

- June monthly GDP contracted by 0.1%, led by the manufacturing sector.

- Q1 GDP was revised down from 2.2% to 2%.

Exports took a big hit in the second quarter as U.S. tariffs on many Canadian goods led to the decline of 7.5% in Q2. The magnitude of this decline cannot be understated, as this is comparable to the export shock during the global financial crisis. The worst is likely behind us, but the export-dependent sectors will continue to face the new reality of higher tariffs.

Final domestic demand, which includes investment and household spending, rose 3.5% in Q2, driven by a 4.5% increase in household consumption. Higher spending on passenger vehicles, financial services, and food and beverage services contributed to the resilience of consumer spending. On a per capita basis, household consumption increased by a stronger 1.1%.

Residential investment also picked up as construction for new units and resale activity gained momentum, increasing the category by 1.5%. Business investment was down on the quarter in almost every category except for computer equipment, software, and R&D. Machinery and equipment investment experienced its steepest decline (-25%) since 2016 outside the pandemic. A further build-up in inventories also contributed to GDP and non-residential investment.

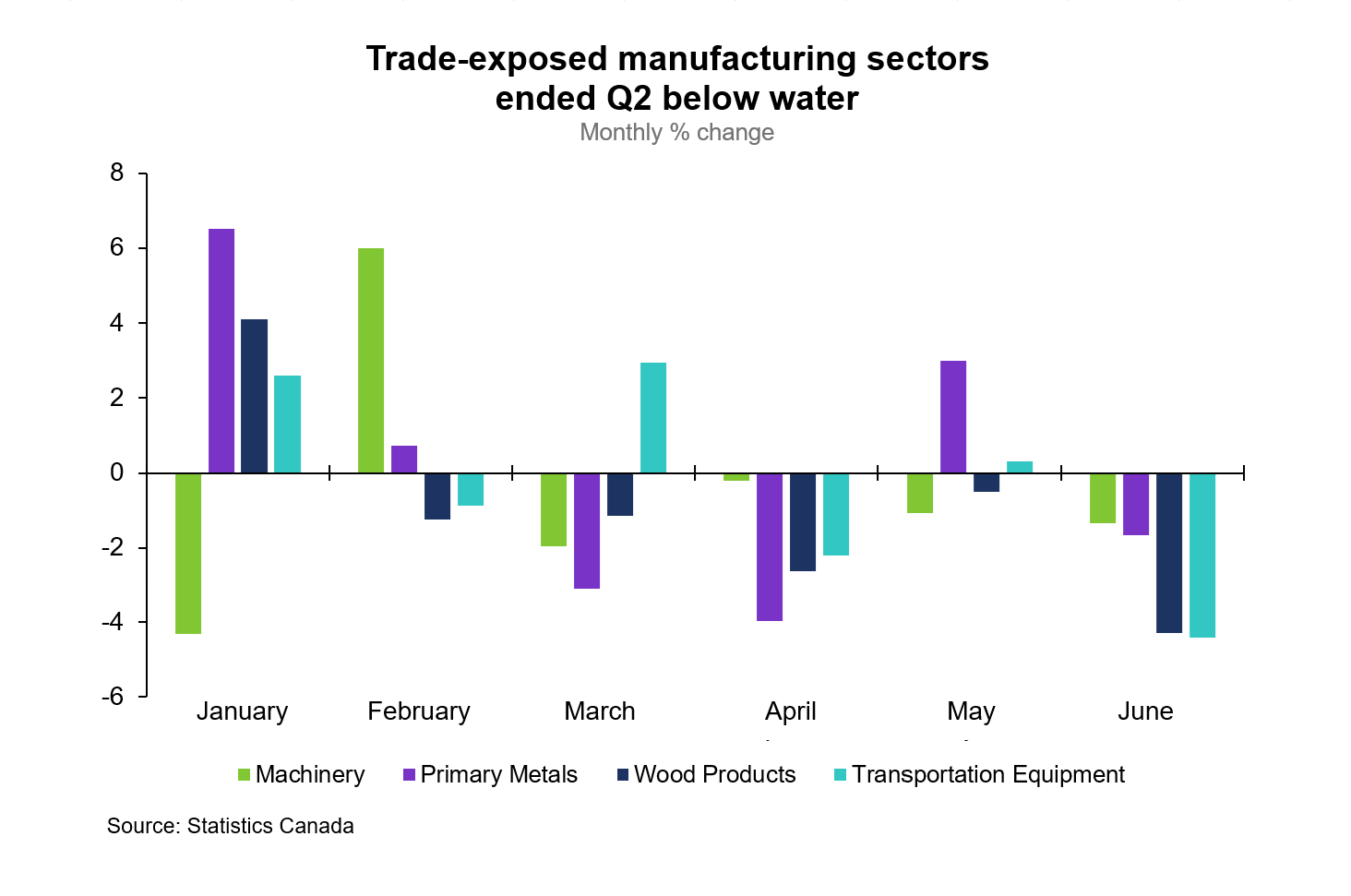

Manufacturing, wholesale, utilities, and mining, oil, and gas sectors were hit the most in the second quarter. June monthly GDP declined by -0.1%, led by widespread declines in the manufacturing sector, which posted its third monthly decline of the last four months. Two-fifths of manufacturers were impacted by U.S. tariffs in June according to Statistics Canada.

OUTLOOK AND IMPLICATIONS

The silver lining in the Q2 GDP numbers was the resilience of the consumer and tepid residential investment that underpin final domestic demand. Official GDP numbers were close to the Bank of Canada’s Q2 forecast of -1.5%, but below economist estimates of -0.7%. Statistics Canada estimates that July GDP is expected to grow 0.1%, with some indication of a rebound in some sectors.

Will Canada avoid a recession? This will depend on the degree to which Canada’s trade will be able to rebound with tariff exemptions and the resilience of Canadian households. With a declining savings rate and weaker income growth, less purchasing power could risk future domestic strength. Markets are 50/50 on whether the Bank of Canada will cut rates in September. The growth risks are clearly to the downside, but the removal of retaliatory tariffs by the Canadian government should reduce inflation risks and convince the Bank to lower interest rates once again.

Other Blogs

Bank of Canada holds interest rates on cloudy conditions downplaying oil price risk to inflation

The dip before the spike, as base effects bring inflation below 2%

Labour market softens as job losses mount and youth unemployment climbs: Labour Force Survey February 2025

Auto Shutdowns Reverse Canada’s Export Momentum: Merchandise Trade January 2026

Inventory drawdown causes GDP to knee jerk into contraction despite improving fundamentals.

Momentum stalls as consumer shifts into a lower gear: Retail Sales December 2025

Diversification Gains Traction as Exports Close the Year Stronger: Merchandise Trade December 2025

6 Predictions for the Canadian Economy in 2026