Blog /

One more time: Bank of Canada hold rates as they assess trade war impacts

The Bank of Canada held its interest rate at 2.75%.

Andrew DiCapua

Share:

“No curveball today. Trade tensions take centre stage as the Bank of Canada holds rates, but Governing Council’s consensus makes it clear that they’re in a holding pattern until Canada’s mixed economic signals sharpen the overall outlook in the coming months. A deteriorating scenario paves the way for renewed rate cuts in the fall. The Bank is calculating carefully, given the realities of long-term tariffs have only begun to take hold.”

The Bank of Canada held its policy rate at 2.75 %, as widely expected. Governing Council struck a more dovish tone than anticipated, yet today’s unanimous decision underscores that the Bank is firmly in a holding pattern—ready to cut only once incoming data clearly weaken. Alongside the announcement, the Bank also released their July Monetary Policy Report.

Compared with January’s projections, the Canadian growth outlook has softened; yet it remains marginally stronger than April’s MPR. GDP growth is now expected in the mid‑to‑low 1 % range, while core inflation is forecast to average around 3.1 % in the second half of 2025 and remain elevated into 2026. The global outlook is slightly weaker, with GDP growth dipping below 3% in 2026.

Trade‑dependent sectors continue to bear the brunt of tariffs and uncertainty, with exporters reporting cost pressures and muted sales expectations. By contrast, domestically focused industries and consumer spending have held up surprisingly well, something that the BoC mentioned they’ll monitor for broader spillovers.

Recent U.S. import data for May shows that only about 55 % of U.S. imports from Canada entered under CUSMA preference, well-below the expectations that 95 % of CUSMA‑eligible goods remain tariff‑free. Embedding this optimistic assumption in the MPR underestimates the potential drag from trade frictions and reinforces downside risks to Canada’s export outlook.

Governor Macklem flagged mounting excess supply in the economy, potentially a counterbalance to higher core‑inflation forecasts. The depth and duration of that slack will dictate the scale and timing of future rate cuts. While today’s pause is appropriate, we maintain that additional easing will be necessary once tariff shocks spread beyond trade‑reliant sectors.

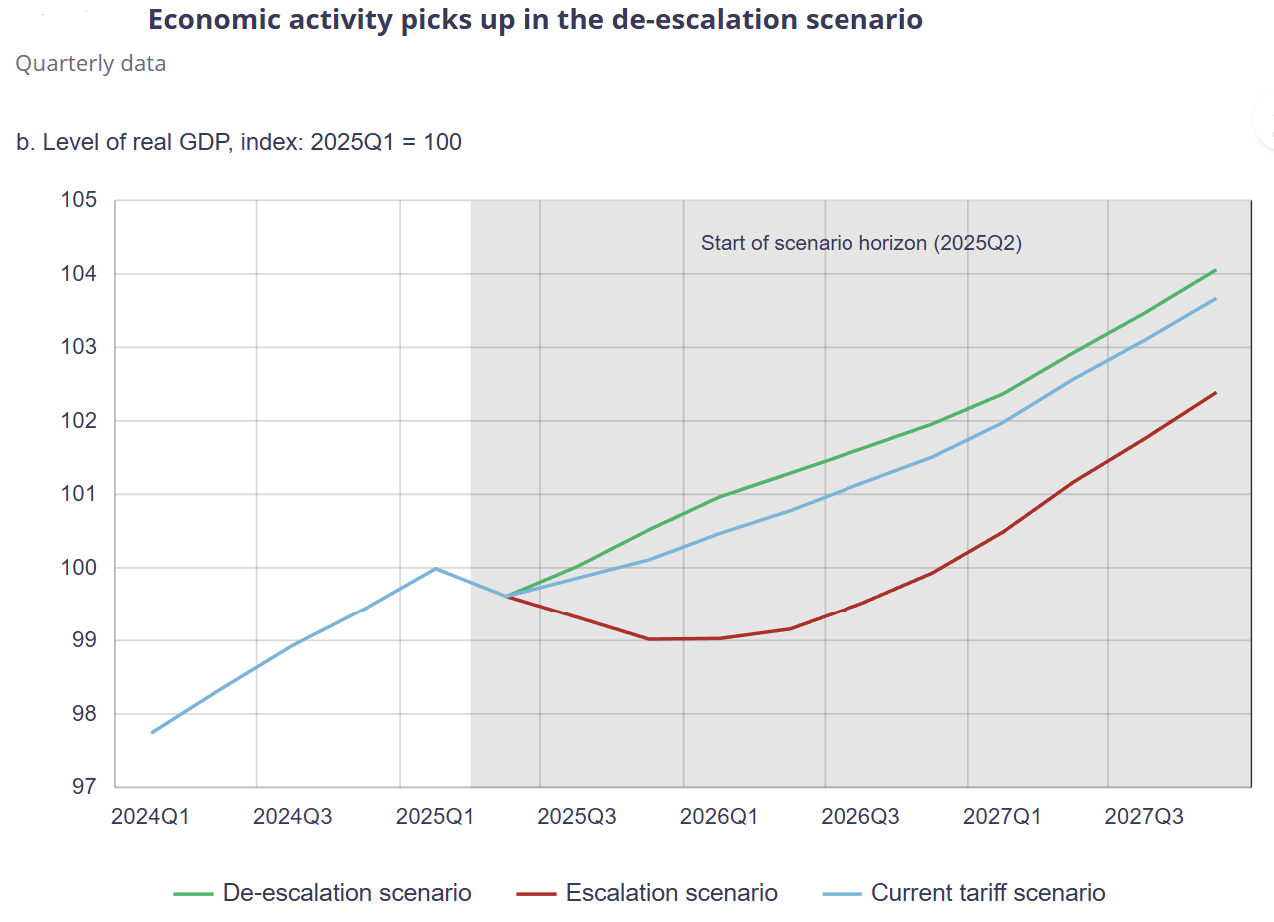

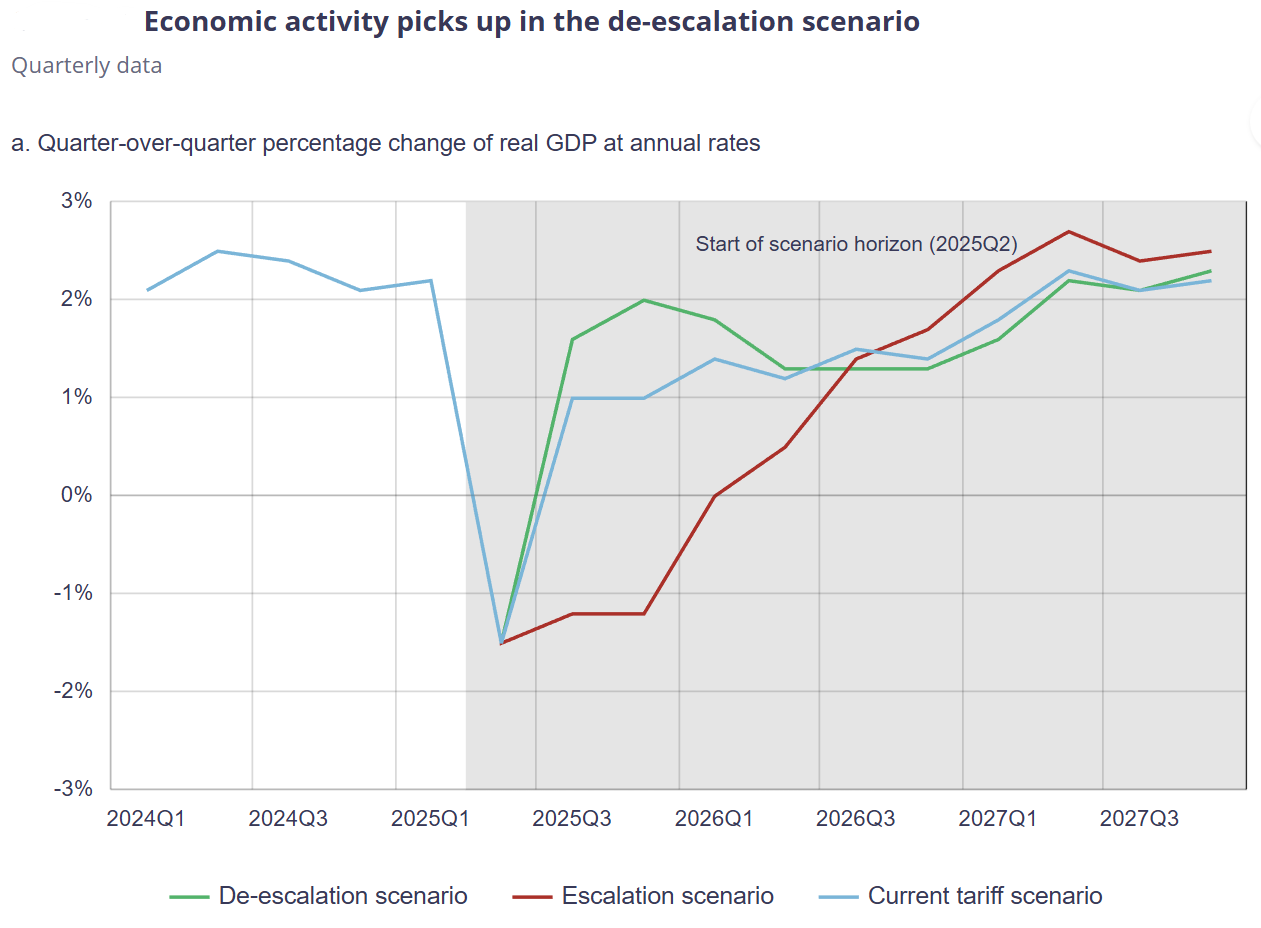

Charts from the July Monetary Policy Report

Other Blogs

Strong Start to the Year, but Underlying Momentum Remains Fragile: Retail Sales January 2026

Bank of Canada holds interest rates on cloudy conditions downplaying oil price risk to inflation

The dip before the spike, as base effects bring inflation below 2%

Labour market softens as job losses mount and youth unemployment climbs: Labour Force Survey February 2025

Auto Shutdowns Reverse Canada’s Export Momentum: Merchandise Trade January 2026

Inventory drawdown causes GDP to knee jerk into contraction despite improving fundamentals.

Momentum stalls as consumer shifts into a lower gear: Retail Sales December 2025

Diversification Gains Traction as Exports Close the Year Stronger: Merchandise Trade December 2025