Blog /

Merchandise Trade August 2025: Tariffs, Gold Swings, and Lumber Duties Sink Canada’s Exports – Trade Gap Hits 18-Month High

Tariffs are taking a toll, and trade diversification isn’t yet delivering. Canadian exporters are still overwhelmingly relying on the U.S. market, even as new tariffs bite into shipments of aluminum, machinery and lumber. The Business Data Lab's Q3 analysis show that only 1 in 4 Canadian merchandise exporters are planning to diversify their sales markets in the year ahead, with most focused instead on finding new suppliers. That imbalance limits how fast Canada can pivot in an increasingly protectionist world.

Jasleen Trehan

Share:

Canada’s trade position weakened sharply in August as exports fell across most sectors while imports rose, driven by gold volatility and higher consumer goods. Steep declines in metals, machinery, and lumber – amplified by new U.S. duties erased the modest gains seen in July. The trade gap widened to its largest level since early 2023, underscoring how fragile Canada’s external balance remains amid tariff pressures, global demand softness, and limited progress in diversifying export markets.

Headline

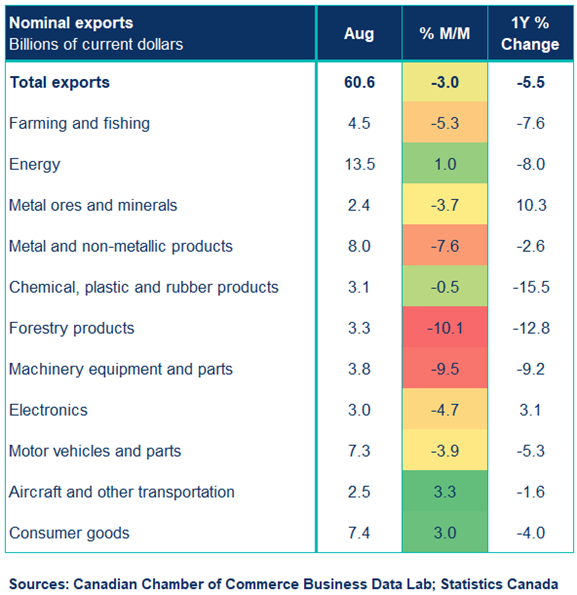

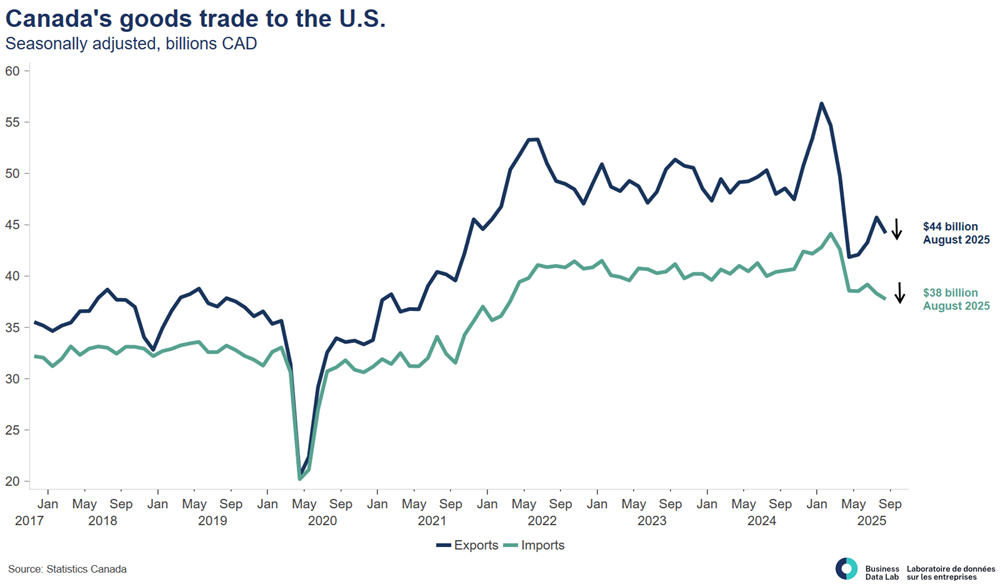

In August, merchandise exports fell 3.0% to $60.6 billion, marking the first decline since April, while imports rose 0.9% to $67 billion. As a result, Canada’s goods trade deficit widened from $3.8 billion in July to $6.3 billion. Exports to the United States dropped 3.4% to $44.2 billion, while imports from the U.S. declined 1.4% to $37.8 billion, narrowing the bilateral surplus to $6.4 billion. Exports to non-U.S. markets fell 2%, while imports from those countries rose 4.2%, pushing the non-U.S. trade deficit to a record $12.8 billion. Including services, Canada’s total trade deficit widened to $6 billion, up from $3.5 billion in July.

Key Takeaways

- Exports declined across 8 of 11 sectors. The largest declines came from metal products (7.6%), industrial machinery (9.5%), and forestry products (10.1%), reflecting the U.S. raising anti-dumping and countervailing duties on softwood lumber. Real export volumes fell 2.8%, erasing July’s gains.

- Imports were up nearly 1% (to $67 B) driven almost entirely by a 24% increase in metal and non-metallic mineral products, led by a 351.7% surge in unwrought gold imports from South Africa and Switzerland. Excluding gold, total imports fell 2%. Energy imports declined 12.8%, while consumer goods rose 2.3% on higher pharmaceutical imports.

- Trade with the United States weakened, with exports down 3.4% and imports down 1.4%, narrowing Canada’s surplus to $6.4 billion from $7.4 billion in July as lower gold and aluminum shipments offset modest import declines.

- The non-U.S. trade deficit reached a record $12.8 billion, as exports fell 2.0% and imports rose 4.2%, due to lower oil and fuel exports to Germany, Japan, and Singapore. Canada’s export diversification has yet to deliver meaningful results.

- The 50% U.S. aluminum tariff placed on Canadian imports in June have put Canadian aluminum exports 24% below 2024 levels. While shipments to the Netherlands, Italy, and Poland are rising, they still represent a small share of total exports.

- According to BDL’s Q3 2025 Business Insights Quarterly, only 1 in 4 exporters plan to enter new international markets in the coming year, while over half are diversifying suppliers instead.

- Services trade, exports edged down 0.2% to $18.7 billion while imports were unchanged at $18.4 billion, leaving the services trade balance slightly positive at $0.3 billion. Canada’s overall trade deficit widened to $6 billion from $3.5 billion in July, underscoring the drag from external demand and tariff-related disruptions heading into the fall.

Implications

- The August report marks a reversal of July’s improvement, with renewed export weakness tied to tariffs on lumber and aluminum, industrial machinery, and precious metals.

- Despite Canada’s removal of most retaliatory tariffs, U.S. tariffs on Canadian aluminum continue to suppress exports.

- Gold trade volatility continues to distort monthly figures, obscuring the underlying slowdown in goods trade volumes.

- Combined with softer August labour and inflation data, this August’s deterioration highlights that the impacts to the Canadian economy are not over.

Sources: Statistics Canada; Canadian Chamber of Commerce Business Data Lab

Other Blogs

Momentum stalls as consumer shifts into a lower gear: Retail Sales December 2025

Diversification Gains Traction as Exports Close the Year Stronger: Merchandise Trade December 2025

6 Predictions for the Canadian Economy in 2026

Conflicting signals as both unemployment and employment rate declines: Labour Force Survey December 2025

Canada’s Productivity Gap Is a Vulnerability We Must Fix

Weak economic momentum could spell fourth quarter contraction.

Gold Payback and Auto Tariffs Push Canada Back into Deficit: Merchandise Trade November 2025

Bank of Canada holds rates as “heightened uncertainty” once again kicks off a new year.