GDP November 2025

Real GDP was unchanged in November providing no relief to the Canadian economy following a -0.3 contraction October.

Andrew DiCapua

Share:

While Canada’s GDP posted a negative reading in the fourth quarter, the economy showed more resilience as we close 2025. The weakness was largely driven by inventories; excluding that drag, growth would have been tracking close to a 1% annualized pace.

Last year was undeniably soft, with structural pressures from the trade war weighing on performance. But 2026 will be a year of recalibration, marked by meaningful policy shifts and population decline that will reshape the foundations of the economy.

Encouragingly, household consumption is recovering, even on a per-capita basis, exports are stabilizing, and we’ve now seen a second consecutive quarter of strong defence-related investment. Business investment still needs broader momentum, but the pickup in machinery and equipment spending is a constructive sign.

Summary

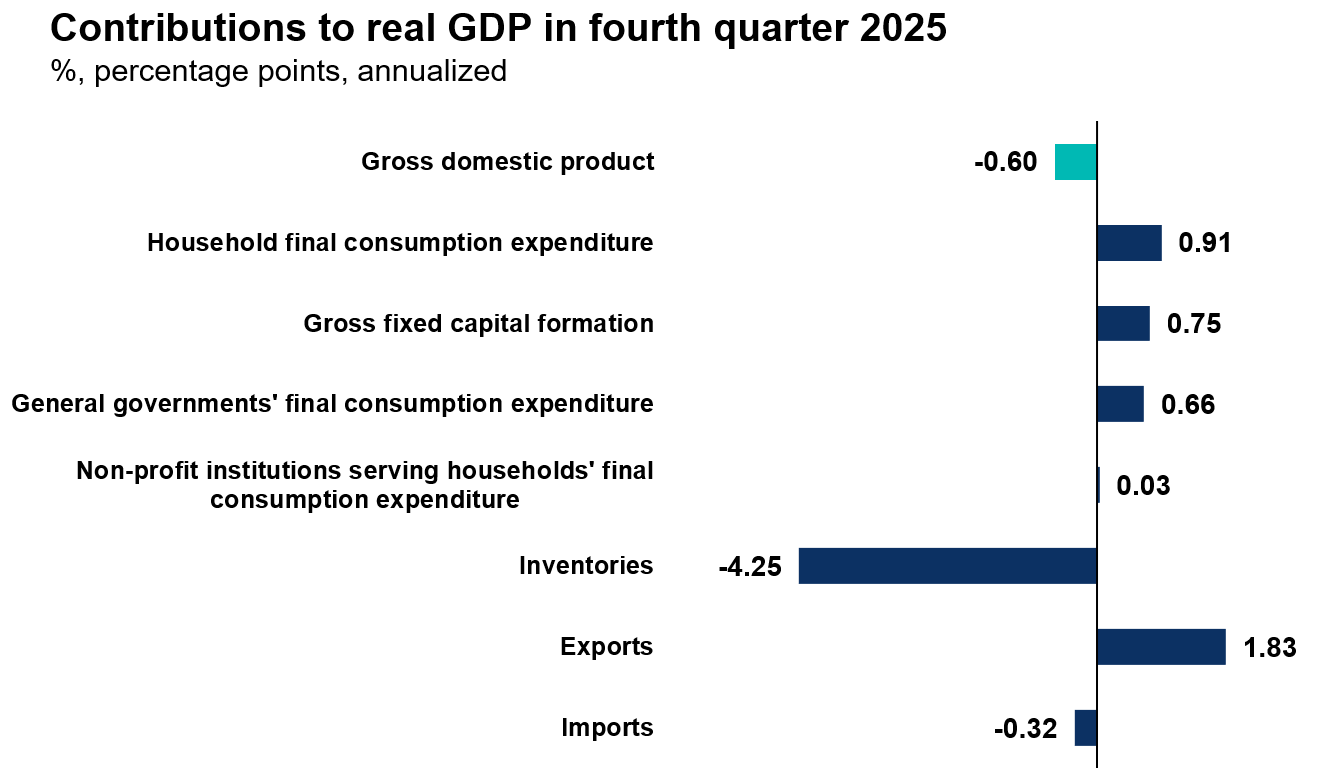

The Canadian economy contracted at a 0.6 percent annualized pace in the fourth quarter of 2025. The decline was driven by a significant drawdown in business inventories during what is typically a seasonally volatile period. As a result, full year 2025 GDP growth came in at 1.7 percent, one of the slowest expansions since 2020, reflecting substantial external pressures, particularly from U.S. tariffs.

Despite the negative headline, fourth quarter fundamentals were surprisingly solid. Final domestic demand recovered, supported by stronger investment and household consumption, alongside stabilization in net exports. While it is premature to declare a turning point, excluding inventories real GDP would have grown at roughly a 1 percent annualized pace in the fourth quarter, still below the annual average but far healthier than the headline suggests.

Household spending remained resilient, rising 1.7 percent annualized in the fourth quarter, even as Canada recorded its first net population decline since 2020. On a per capita basis, consumption improved further. Services spending led the gains, while durable goods remained soft as households continued to delay larger purchases such as vehicles.

After sharp swings in the second and third quarters, trade flows were more stable in the fourth quarter. Exports rose 6.1 percent annualized, driven by goods exports, while services exports declined. Metals, particularly gold and aluminum, supported growth, with shipments primarily to Europe. Imports increased 1 percent in the quarter. For 2025 overall, exports fell 1.7 percent, weighed down by US tariffs on Canadian goods. However, exports to non-US markets continued to strengthen, helping cushion the broader trade position.

Investment growth was driven largely by government capital spending, which increased 20 percent annualized in the fourth quarter, marking the second consecutive quarter of strong defence related investment. In contrast, business investment declined by 0.2 percent with residential largely the drag, while non-residential categories like machinery and equipment and intellectual property rose. Notably, government capital spending outpaced business investment for the third consecutive year in 2025.

Services industries led overall growth in 2025. Goods sector gains were concentrated in mining, oil, and gas, supported primarily by higher prices rather than volume growth. In the fourth quarter, output was led by health care, real estate, and finance and insurance.

Implications

The economy appears to be on firmer footing than the headline contraction implies. Inventories are volatile and don’t necessarily reflect underlying weakness.

Fourth quarter GDP came in below economists’ consensus of 0.2 percent growth and the Bank of Canada’s projection of flat growth. BDLNow had forecast 1.2 percent growth. Statistics Canada’s early estimate suggests January monthly GDP will be flat.

Financial markets have largely looked through the negative headline, with no rate changes currently expected this year.

Overall, the balance of risks to inflation and growth is becoming more even after a year marked by significant headwinds. Looking ahead, we should expect firmer fundamentals in 2026, though below potential growth is likely to persist as the economy continues to recalibrate and regain momentum.

Source: Statistics Canada

Other Blogs

Sticky hiring, but wage growth at its highest since 2024: Labour Force Survey March 2025

Volatile Imports Drive Wider Deficit Despite Export Rebound: Merchandise Trade February 2026

January 2026 GDP: Canada’s economy kicks off 2026 on decent footing

Strong Start to the Year, but Underlying Momentum Remains Fragile: Retail Sales January 2026

Bank of Canada holds interest rates on cloudy conditions downplaying oil price risk to inflation

The dip before the spike, as base effects bring inflation below 2%

Labour market softens as job losses mount and youth unemployment climbs: Labour Force Survey February 2025

Auto Shutdowns Reverse Canada’s Export Momentum: Merchandise Trade January 2026