Blog /

Budget 2023: Mo’ Problems; Mo’ Money

The 2023 federal budget is a signal that a mild recession is still in the cards. Slowing growth and higher interest rates have put the federal government between a rock and a hard place. A key takeaway here is just how hard it is to craft effective fiscal policy in the shadow of the pandemic, supply chain disruptions, and the war in Ukraine.

Business Data Lab

Share:

The 2023 federal budget revised down the economic outlook and now incorporates a mild recession in Canada this year. But that didn’t stop the government from introducing another $43 billion in net new initiatives over the projection. For Canadian businesses there are mixed signals in this budget: on the one hand, the government is encouraging private-sector investment in the green economy and taking a harder look at previous spending commitments; but on the other hand, the government is introducing new taxes that will discourage economic activities for high-earners and businesses.

Stephen Tapp, Chief Economist, Canadian Chamber of Commerce

KEY TAKEAWAYS

- Difficult Context: Budget 2023 comes at a difficult time. The lingering pandemic is still having adverse economic impacts. Russia’s war is raging in Ukraine. Geopolitical tensions risk balkanizing global supply chains, all while recent financial market turmoil has increased uncertainty.

Here at home, Canadian businesses and consumers are struggling with rising costs and affordability challenges. Our economy faces long-standing competitiveness and growth challenges, as the world moves towards a net-zero economy. The combination of slowing growth and higher interest rates brings new fiscal headwinds. All told, it’s a tough time to be a fiscal policymaker.

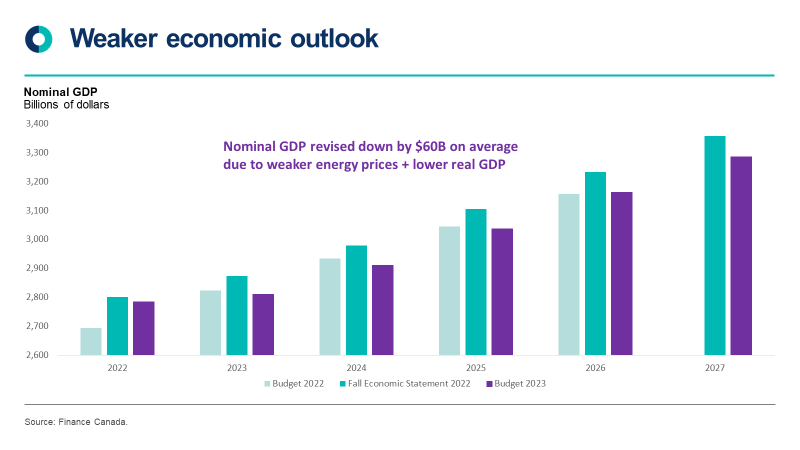

- Weaker Economic Outlook: Not surprisingly, the private-sector economic forecast was downgraded in Budget 2023.

This primarily reflects two factors:

- First and most consequential for the fiscal projection,with weaker global growth and softer commodity prices, Canada’s GDP inflation forecast was lowered for this year (from 1.8% to 0.6%).

- Second, and more likely to attract headlines, Canada’s forecasters now expect a mild recession featuring three consecutive negative quarters of growth to start 2023. If realized, this would be a shallow recession (if not a soft landing, certainly “softish”) with real GDP growth only lowered from 0.7% to 0.3% this year.

This double-whammy is effectively a one-time hit for the economy that drags down the expected pathfor nominal GDP — the broadest measure of the government’s tax base — by an average of $60 billion (or 2%) over the projection. So fiscal policymakers face a worse starting point.

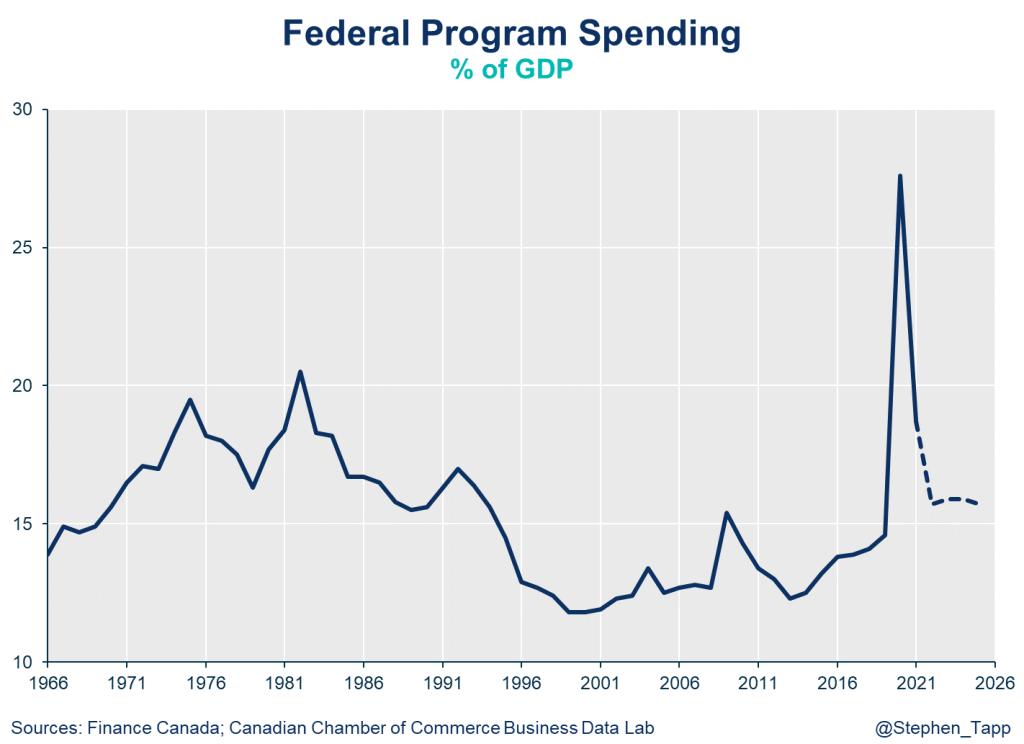

- New Measures: With the weaker economic outlook, the federal government appears to be rethinking and reallocating many previous spending commitments, but they didn’t hesitate to ramp up spending. Budget 2023 adds roughly $43 billion in net new measures over the six-year projection period (i.e., after accounting for new tax measures and spending reallocation). While there are many ways to break down these moves, I “follow the money” to identify five big-ticket categories

- Health care (with additional transfers to provinces/territories) and dental care (scaling up the new program) were the biggest combined area of new spending at more than $31 billion.

- Next is the roughly $16 billion for various investment tax credits to help spur private-sector investment to build Canada’s clean economy — ostensibly the government’s response to recent and massive green subsidies south of the border.

- While the tax credits should encourage companies to invest, on the other side of the ledger are new tax measures worth $14 billion targeting high-earning companies and individuals. This included movement on the global minimum corporate tax (part of the OECD’s two-pillar approach, along with renewed commitment to impose a digital sales tax, if needed), revamping the “alternative minimum tax” on high-earners, and new taxes on share buybacks as well as bank dividends. These measures are likely to discourage economic activity on the margin.

- Right behind the tax moves are the many budget line items that total around $13 billion which also help the government’s bottom line by reallocating previous spending in many areas and departments (including spending cuts for external consultants and government travel).

- Finally, I lumped a variety of “other” moves together with a total price tag of over $25 billion. This includes reconciliation, affordability (with another one-time top-up of the GST credit for lower-income households, in this case notionally directed to groceries).

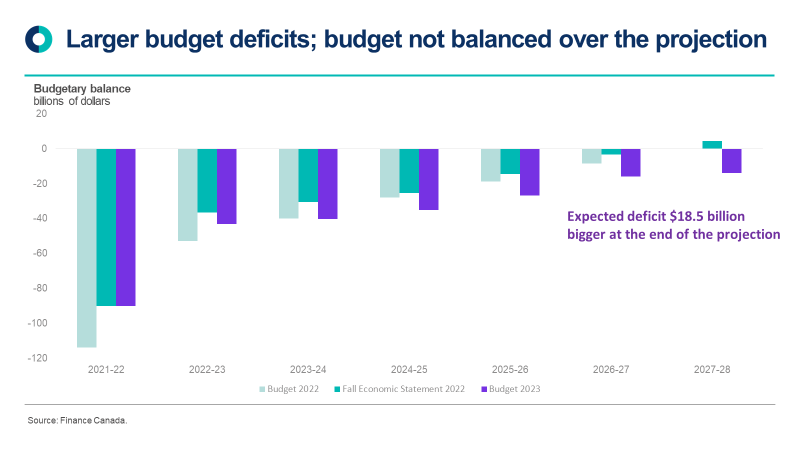

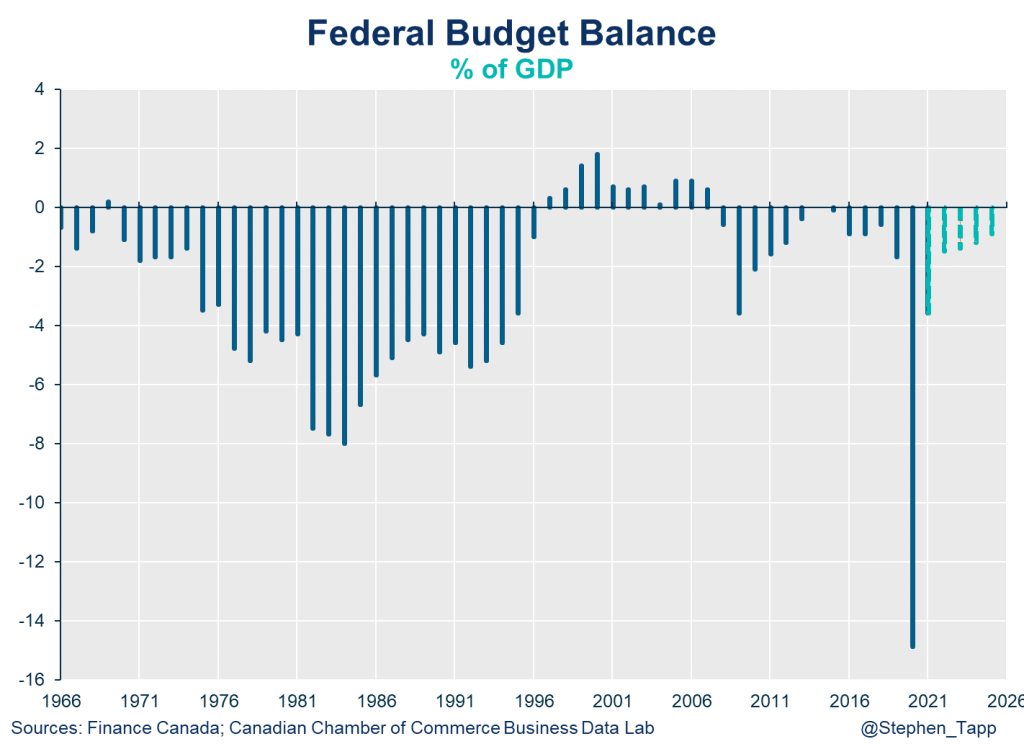

- Fiscal Outlook: With a weaker economy and net new spending, the fiscal outlook worsened.

- Deficits: The federal deficit is $18.5 billion bigger by the end of the projection. Notably, the government abandoned its plans to balance the budget over the projection. As a share of GDP, deficits remain manageable, but are still likely to concern some fiscal watchers. These deficit ratios are expected to shrink modestly each year from 1.5% in the current fiscal year, trending around the 1% range, and ending the forecast at 0.4% of GDP.

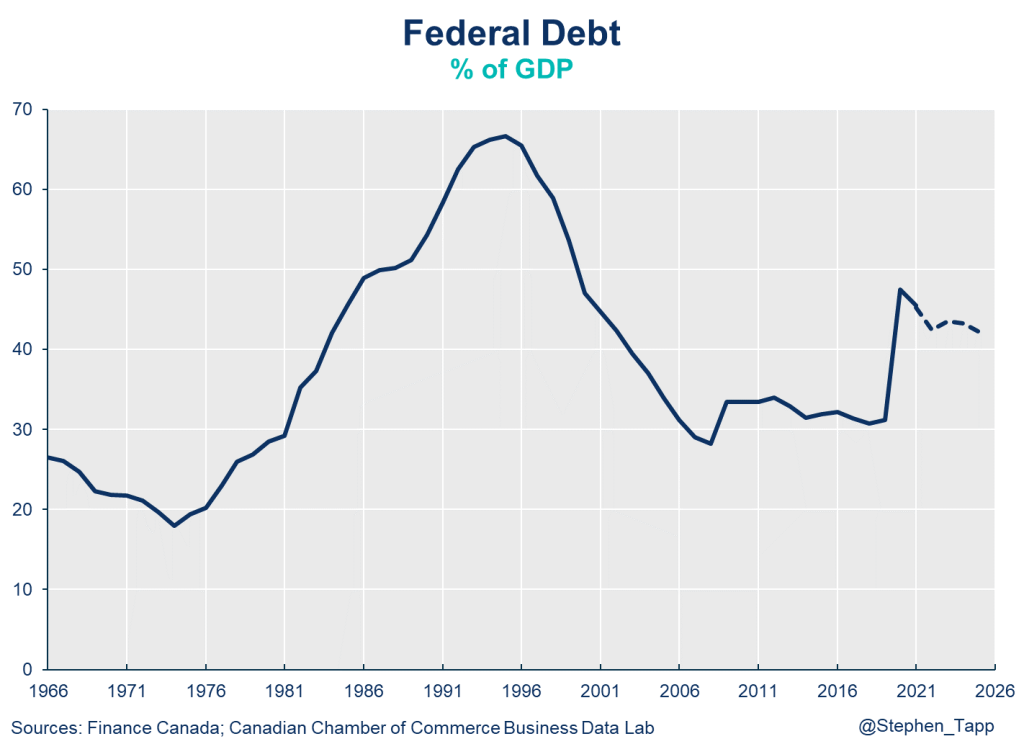

- Debt: Federal debt increased by $132 billion over the projection to $1.3 trillion five years out. As a share of GDP,federal debt starts at 42%, and is expected to rise a few percentage points over the next few years, before ending the forecast modestly improved at 40% in 2027-28.

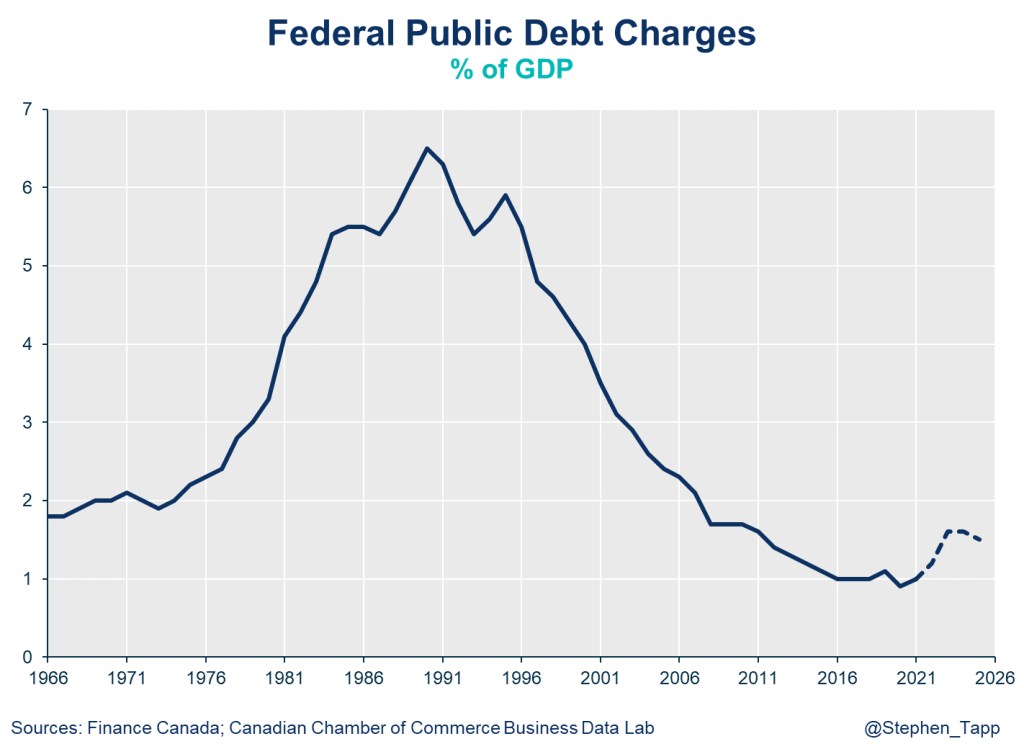

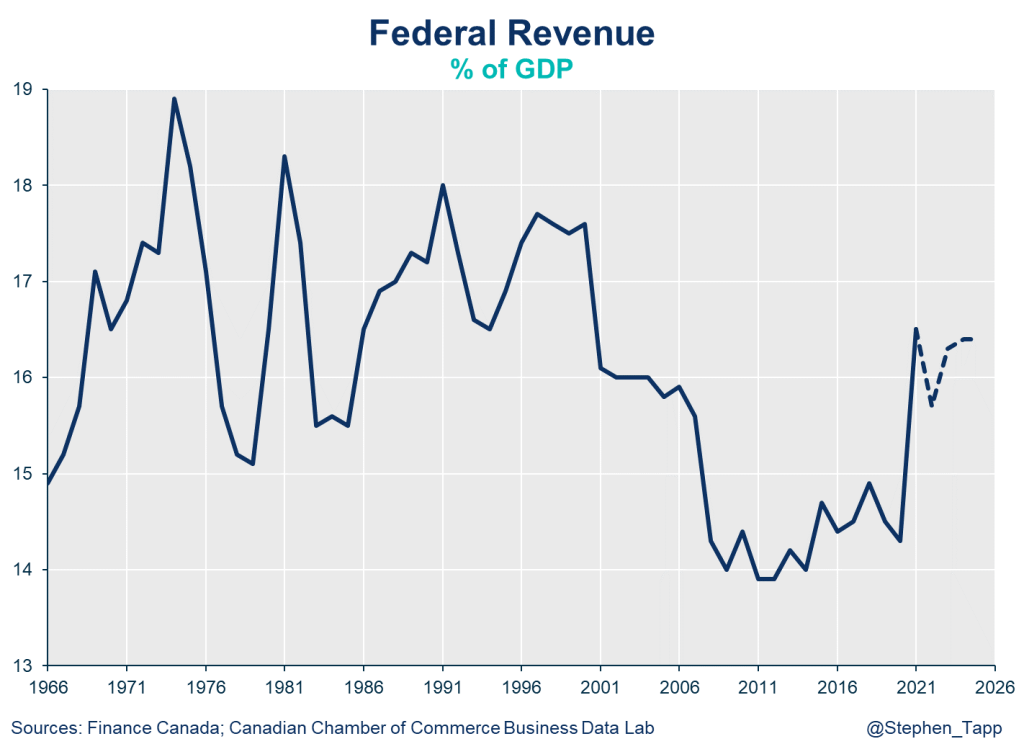

- Fiscal anchors and long-run sustainability: Previously, the government stated its “fiscal anchor” was to: 1) unwind COVID-related deficits; and 2) reduce the federal debt ratio over the medium term. Budget 2023 dropped any reference to deficit elimination. In its baseline scenario, the federal debt ratio is expected to rise for a few years but is anticipated to eventually fall over this projection. However, in the downside forecast scenario, the debt ratio is higher for four years, and is only modestly improved by the fifth year.Looking further out, Finance Canada’s long-term projections show the status quo federal debt ratio is on track to decline steadily over the next 30 years, even in the downside scenario. However, this assumes no additional spending beyond the status quo, but in reality, this government has tended to increase spending in each successive budget. Moreover, the Parliamentary Budget Office estimates that the outlook is notably weaker for the provinces, given their increased exposure to health care costs which are expected to rise as the population ages.

- Risks: Given the elevated level of uncertainty, this budget included an upside and a downside scenario. The forecaster survey occurred in February before the recent financial market turmoil. At this point, it looks like Canadian real GDP will be positive in Q1 2023, but a recession remains a real risk (probably a 50%-65% likelihood in 2023). If global conditions deteriorate further, it’s easy to imagine scenarios far worse than the downside scenario modelled. That said, this constitutes a reasonable basis for fiscal planning. But I see the risks still tilted to the downside, just like they were in Budget 2022.

MORE FISCAL CHARTS

Other Blogs

Strong Start to the Year, but Underlying Momentum Remains Fragile: Retail Sales January 2026

Bank of Canada holds interest rates on cloudy conditions downplaying oil price risk to inflation

The dip before the spike, as base effects bring inflation below 2%

Labour market softens as job losses mount and youth unemployment climbs: Labour Force Survey February 2025

Auto Shutdowns Reverse Canada’s Export Momentum: Merchandise Trade January 2026

Inventory drawdown causes GDP to knee jerk into contraction despite improving fundamentals.

Momentum stalls as consumer shifts into a lower gear: Retail Sales December 2025

Diversification Gains Traction as Exports Close the Year Stronger: Merchandise Trade December 2025