Blog /

Bracing for impact: The Bank of Canada cuts rates again before possible U.S. tariffs hit

Today, the Bank of Canada made the right call with a widely expected 25-basis-point rate cut to 3%.

Stephen Tapp

Share:

“Today, the Bank of Canada made the right call with a widely expected 25-basis-point rate cut to 3%. While Trump’s proposed tariffs on Canadian exports haven’t materialized yet, the threat alone is weighing heavily on Canadians and casting a shadow over the economic outlook. If these tariffs are ultimately imposed, the BoC and Canadians will face the challenging prospects of weaker growth and higher prices. The Monetary Policy Report sketched out the potential recessionary impacts of a trade war scenario, but the Bank ultimately did not tip its hand on the playbook to respond, citing significant uncertainty, while acknowledging the limitations of monetary policy, and the need for fiscal policy to provide additional targeted transitional support.”

- The Bank of Canada lowered its policy rate by 25 basis points to 3%. This is the sixth consecutive cut since June when the rate was much more restrictive at 5%. This move was widely expected ─ markets had priced in more than a 90% chance of this decision ─ and it comes on the heels of larger rate cuts at the last two meetings.

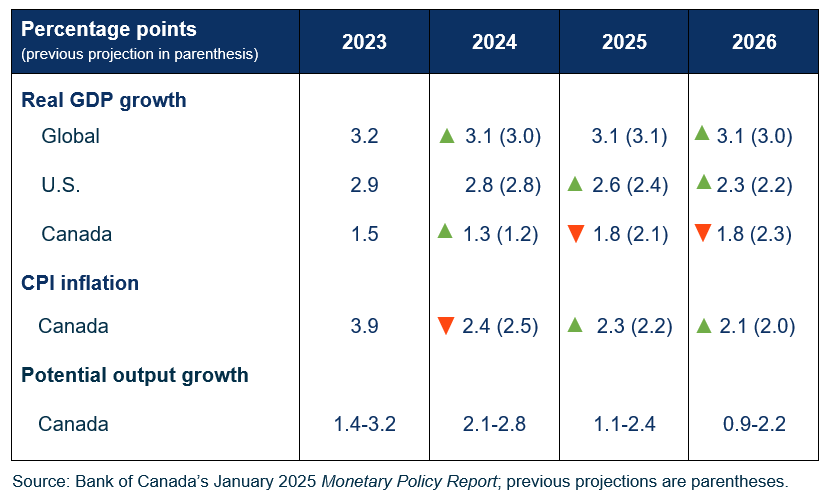

- Canada’s economic growth outlook was revised down to reflect slowing population growth even before tariffs: Canada’s economy has recently gained momentum thanks to lower interest rates, which are supporting consumer spending and the housing market. The main forecast change is a downward revision to economic growth from slower population growth that reflects government targets to reduce immigration. Business investment remains “weak” and the labour market “soft” with the economy operating below its potential. The Bank now expected real GDP growth to average 1.8% annually this year and next, assuming no new U.S. tariffs.

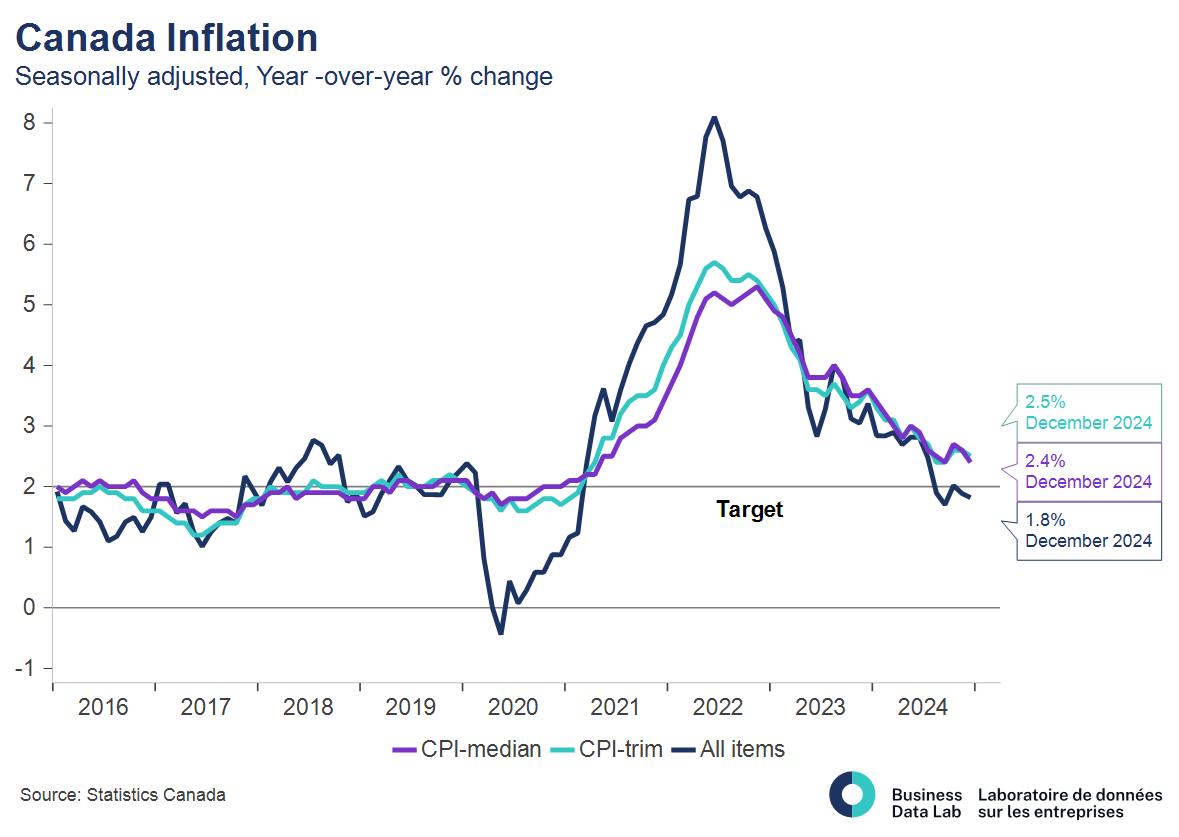

- Canada’s inflation, headline currently below target, but short-run core pressures creeping up: Headline inflation in Canada came back under control in 2024. The temporary consumption tax changes will introduce some short-term volatility for headline numbers, but recent trends for core inflation have increased with the economic uptick. That caused the Bank to nudge up its inflation forecast to run slightly above the 2% target over the next two years (again not including any tariff impacts).

- The U.S. tariff threat looms large: Notably the Bank’s baseline forecast doesn’t include new U.S. tariffs ─ the threat of which, has significantly raised uncertainty for businesses, consumers, and policymakers, making planning much more difficult.

In an illustrative trade war scenario, the Bank’s modelling suggests that Canada’s economy would fall into a recession (which is consistent with, but slightly more severe than the BDL’s updated modelling). The price pressures from tariffs and a weaker dollar put upward pressure on prices, leaving the BoC in a very difficult spot.

Personally, I think it would be wise to lean into supportive mode, cut rates to backstop confidence, and let the exchange rate depreciate to act as shock absorber. This is one way to help ease the economic transition and help struggling Canadian workers and businesses deal with a significant external shock. Of course, I acknowledge this carries the risk of inflation expectations rising quickly, after the big pandemic inflation price level overshoot we just lived through. But the Bank’s own numbers are not too worrying on the inflation pressures. Fiscal and trade policy are other critical parts of our macro response if a big tariff storm comes.

The Bank’s analysis also finds that tariff threats are largely responsible for the Canadian dollar’s 6% depreciation versus the U.S. dollar in recent months.

- The U.S. Federal Reserve announces its interest rate decision later today. Markets expect the Fed to hold steady, and are pricing in only one rate cut in the first half of 2025. If true, this would push Canadian rates further below those in the U.S., which would weigh further on the Canadian dollar.

- Finally, the Bank also announced plans to end its quantitative tightening program, which was expected, and will normalize its balance sheet going forward.

Other Blogs

Strong Start to the Year, but Underlying Momentum Remains Fragile: Retail Sales January 2026

Bank of Canada holds interest rates on cloudy conditions downplaying oil price risk to inflation

The dip before the spike, as base effects bring inflation below 2%

Labour market softens as job losses mount and youth unemployment climbs: Labour Force Survey February 2025

Auto Shutdowns Reverse Canada’s Export Momentum: Merchandise Trade January 2026

Inventory drawdown causes GDP to knee jerk into contraction despite improving fundamentals.

Momentum stalls as consumer shifts into a lower gear: Retail Sales December 2025

Diversification Gains Traction as Exports Close the Year Stronger: Merchandise Trade December 2025