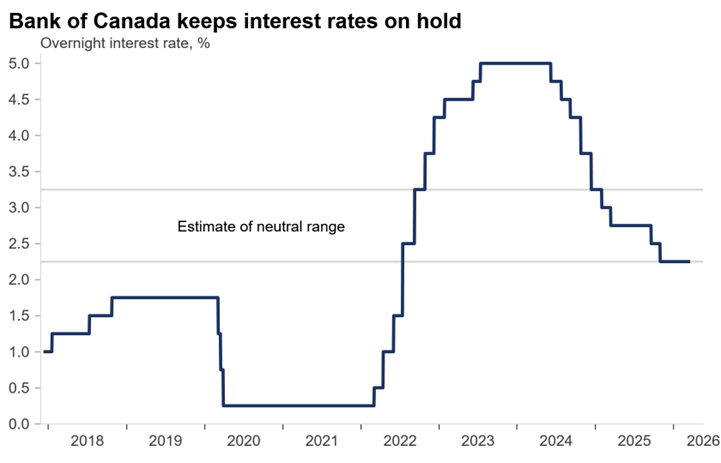

Bank of Canada holds interest rates on cloudy conditions downplaying oil price risk to inflation

Bank of Canada March 2026

Andrew DiCapua

Share:

The Bank of Canada may be holding rates today, but that position may not last long. Uncertainty remains the name of the game. Inflation risks remain low, despite elevated oil prices spiralling from the Middle East conflict adding real cost pressures for Canadians. The Governor acknowledged the asymmetric trade-off that higher oil prices create for the Canadian economy. The bigger issue right now is that the economy is tepid, with exports still at risk. We shouldn’t rule out the possibility of rate cuts this year. Two months of significant job losses, along with a pullback in consumer spending will dampen the case for any rate hikes in the near term. In his comments, the Governor of the Bank seems to sense this decision is like taking a pause before hitting a fork in the road.

Summary

There were two things widely expected going into this Bank of Canada decision. Rates would be held, and uncertainty would continue to cloud the Governing Council’s view.

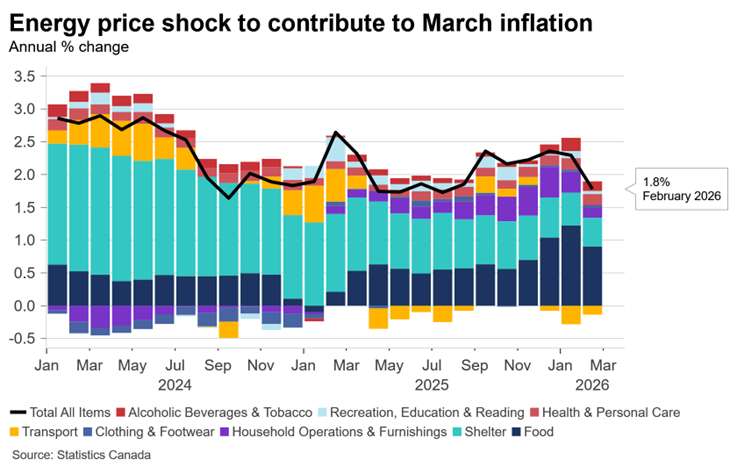

Since the last meeting in January, the Canadian economy has shown signs of weakness, while the war in the Middle East has now stretched into its third week. Benchmark oil prices have climbed to nearly 100 dollars per barrel, and gasoline prices are up about 30 percent since the start of the year. At the same time, February inflation came in at 1.8 percent, though that figure was influenced by the GST holiday a year ago.

In his opening remarks, Governor Macklem suggested the Bank will largely look through the oil price shock for now. Inflation will likely pick up in the near term, particularly in March. Our estimates suggest gasoline prices alone could add about 0.13 percentage points.

All of this shifts our view. Interest rates are no longer clearly in a holding pattern for all of 2026. There is a high degree of uncertainty, combined with weaker economic conditions, that the Bank may need to respond to. Our base case remains a hold for now, but that outlook is becoming less certain.

Markets had been pricing in rate hikes beginning in September. That expectation has not moved much, but the probability of hikes is still below 50 percent.

Excess supply is growing, albeit slowly, and is weaker than the Bank projected in January, largely due to inventory dynamics. There is little evidence of pent up demand in the economy, which limits upward pressure on growth.

The Governor also noted that financial conditions have tightened. Bond yields have risen, and equity markets have declined. That combination could weigh further on consumer sentiment and reinforce already softer economic conditions.

Implications

On balance, policy remains on hold for now, but the focus is shifting to timing. Comparisons to the inflation episode in 2022 came up, though the Governor pushed back, emphasizing that this time is different. That said, gasoline prices tend to feed into inflation expectations. Alongside elevated food prices, this could create additional pressure if the conflict persists for longer than expected.

Source: Statistics Canada

Other Blogs

Sticky hiring, but wage growth at its highest since 2024: Labour Force Survey March 2025

Volatile Imports Drive Wider Deficit Despite Export Rebound: Merchandise Trade February 2026

January 2026 GDP: Canada’s economy kicks off 2026 on decent footing

Strong Start to the Year, but Underlying Momentum Remains Fragile: Retail Sales January 2026

The dip before the spike, as base effects bring inflation below 2%

Labour market softens as job losses mount and youth unemployment climbs: Labour Force Survey February 2025

Auto Shutdowns Reverse Canada’s Export Momentum: Merchandise Trade January 2026

Inventory drawdown causes GDP to knee jerk into contraction despite improving fundamentals.