Bank of Canada Decision January 2026

Bank of Canada holds rates as “heightened uncertainty” once again kicks off a new year.

Andrew DiCapua

Share:

The Bank of Canada holding rates at 2.25% was widely expected and reflects its view that policy is already close to neutral. But the message from the governing council is pretty clear: the Canadian economy is still underperforming. Growth continues to disappoint, and uncertainty around U.S. tariffs remains a real concern, even a year later. We think the Bank is likely to stay on the sidelines for now, keeping rates on hold as weak growth outweighs inflation risks. Despite some recent optimism about the economy, it doesn’t look like minds are convinced at the Bank. Looking ahead, there are still major challenges looming, from the CUSMA review to demographic pressures and softer consumer spending.

The Bank of Canada held its policy interest rate at 2.25%, a decision widely expected by economists. The Bank does not appear to be buying the recent resilience in the economic data.

Uncertainty is back front and centre, with Governor Macklem stressing that uncertainty remains “high,” citing renewed geopolitical concerns. This is consistent with the Bank’s updated forecast, which anticipates Canada’s GDP growing just 1.1% in 2026—below market expectations. For context, the International Monetary Fund recently released its latest assessment of the Canadian economy, forecasting 1.6% growth this year.

The Bank released its January Monetary Policy Report (MPR) alongside the decision, showing that the Canadian economy is now 1.5% smaller than projected last year.

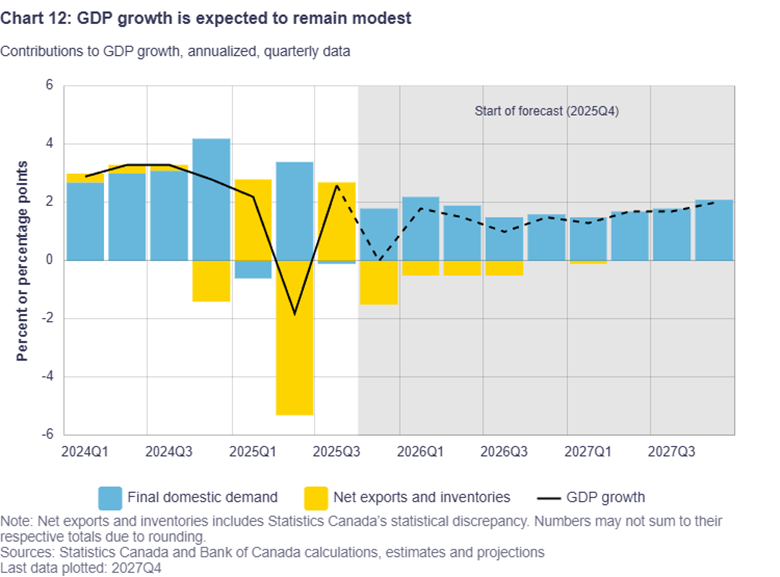

Weak economic growth in 2026

The Canadian economy is expected to grow 1.1% in 2026, following GDP growth of 1.7% in 2025, with the fourth quarter on track to provide a weak handoff. Weaker growth this year will be driven in part by slower population growth.

Business investment is now expected to make a modest contribution (0.1 percentage points) to GDP growth, supported by incentive measures in Budget 2025 and an assumption that firms will gradually adjust to the new U.S. tariff environment. A small rebound in residential investment is also expected to support growth. It remains unclear how the Bank is measuring the extent to which CUSMA renewal uncertainty is weighing on business investment.

Goods exports continue to recover from the export shock, with diversification into other markets supporting some of the rebound. Exports to non-U.S. markets are up roughly 13%. The durability of this trend will depend on how effectively firms can shift supply chains, as exports remain on a lower trajectory due to U.S. tariffs.

Final domestic demand is expected to improve in 2026, with consumption per person picking up. Overall consumption will be one of the main contributors to GDP growth, though weak consumer sentiment and a significant volume of mortgage renewals in 2026 pose key challenges.

Hiring intentions among firms surveyed by the Bank remain muted. Despite this, the Canadian economy added 190,000 jobs last year. Sectors with higher reliance on U.S. demand experienced employment losses of about 30,000 jobs, based on latest payroll data.

The global economy is forecast to grow 3.2% in 2026, up 0.3 percentage points from October’s report. Once again, the Bank expects stronger growth in key economies. U.S. GDP received the largest upward revision for 2026, now projected at 2.6%, up 0.4 percentage points from October.

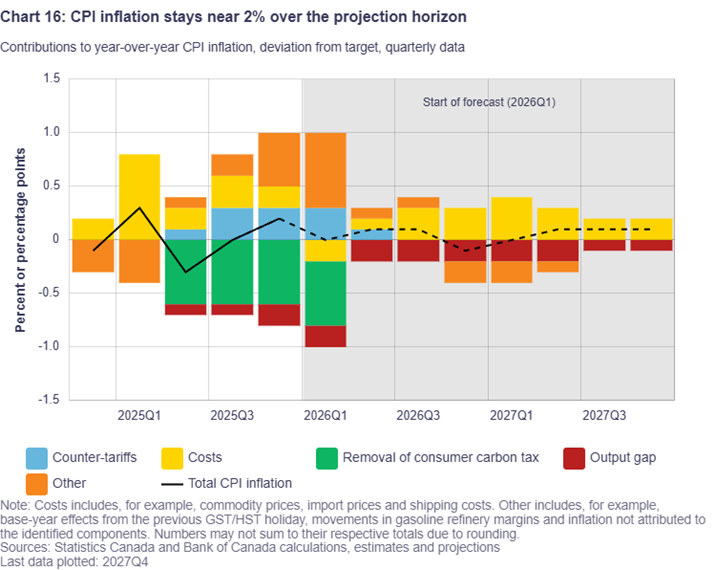

Inflation near the 2% target

Inflation is forecast to be on target this year. Surprisingly little attention was paid to inflation during the press conference with Governor Macklem and Senior Deputy Governor Rogers. While the Bank notes that core measures are improving, it rightly points out that some components remain above target—particularly food and services inflation, which continue to run hot.

It will be important to monitor how these pressures evolve and how the Bank treats them, especially as affordability remains a key concern for households. The share of the CPI basket growing above 2% now stands at 60%.

That said, weaker growth should help keep price pressures subdued, assuming little change to the Bank’s estimate of potential output, which will be revisited in April. Notably, potential GDP growth was revised up to 2.3% from 1.6%, suggesting the economy remains in excess supply.

In a rare move, Governor Macklem also addressed central bank independence, noting that the criminal charges against Fed Chair Jerome Powell were concerning. “He is doing a good job at leading the Fed based on evidence, based on facts … I hope it stays that way. That’s going to be important for everyone.”

Implications

The Bank of Canada is expected to remain on the sidelines following a long and aggressive rate cycle. Given the weakness in the Canadian economy, the next move is more likely to be a rate cut, though inflation dynamics will remain critical to watch.

The BDL’s nowcast expects fourth-quarter growth of 0.8%, above the Bank’s forecast of flat growth. Markets have priced in the first rate cut no earlier than the December meeting. The execution of Budget 2025—particularly in delivering capital investment—will be key to buffering the economy and supporting growth.

Other Blogs

Inventory drawdown causes GDP to knee jerk into contraction despite improving fundamentals.

Momentum stalls as consumer shifts into a lower gear: Retail Sales December 2025

Diversification Gains Traction as Exports Close the Year Stronger: Merchandise Trade December 2025

6 Predictions for the Canadian Economy in 2026

Conflicting signals as both unemployment and employment rate declines: Labour Force Survey December 2025

Canada’s Productivity Gap Is a Vulnerability We Must Fix

Weak economic momentum could spell fourth quarter contraction.

Gold Payback and Auto Tariffs Push Canada Back into Deficit: Merchandise Trade November 2025