Blog /

August 2024 GDP: More Tricks, Less Treats

This economy isn’t rising from the dead, despite a hint that growth picked up in September.

Andrew DiCapua

Share:

This economy isn’t rising from the dead, despite a hint that growth picked up in September. Per capita growth remains in decline, and while the Governor might be tricking us with talk about where the neutral interest rate could be, there’s no doubt Canadians need more treats to get things moving. The economy faces serious headwinds, and with growing uncertainty in the outlook, the Bank’s third-quarter forecast may be a little too optimistic.

- Andrew DiCapua, Senior Economist, Canadian Chamber of Commerce

KEY TAKEAWAYS

Headlines

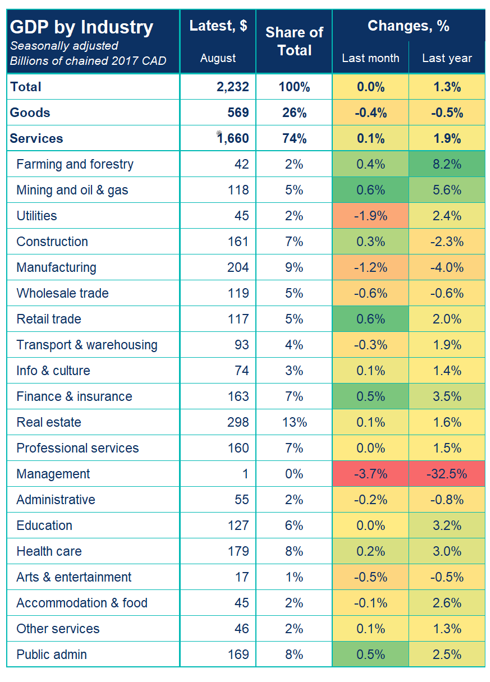

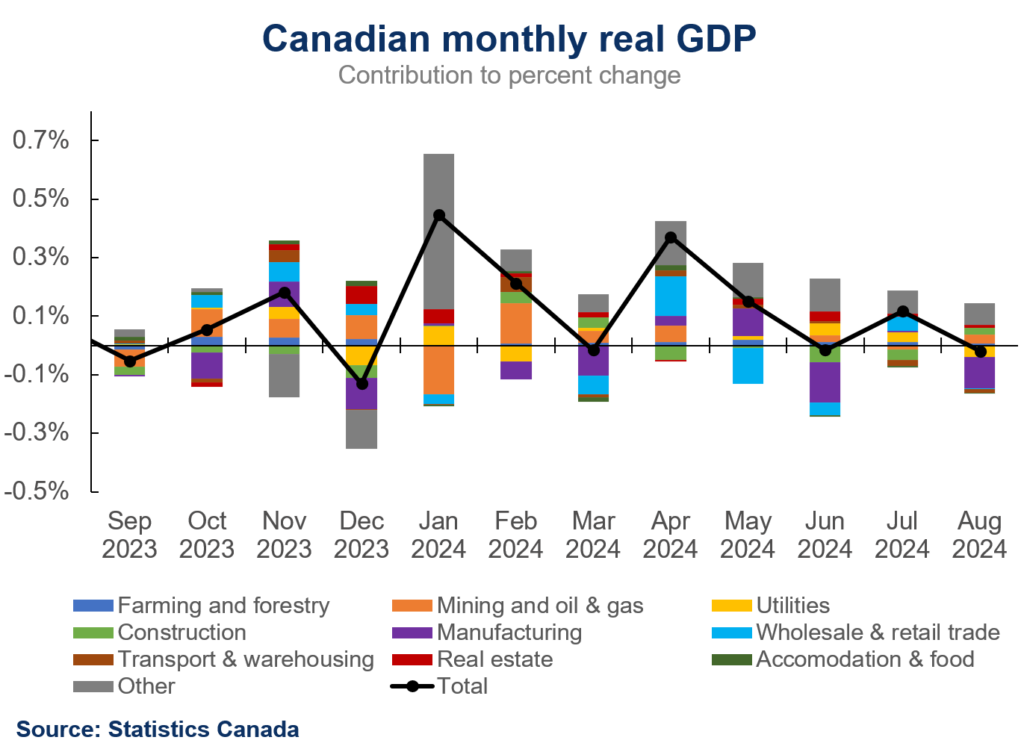

Real gross domestic product was flat in August, in line with consensus forecasts. Most sectors posted growth in August (12 of 20 sectors), but services led the month, growing 0.1%, with the goods sectors declining 0.4% m/m—the weakest since December 2021. The summer momentum doesn’t seem to have lasted with July GDP being revised down by 0.1%.

Movers and Shakers

- Manufacturing: The sector declined 1.2% in August, with both durable and non-durable goods experiencing drops. Chemical manufacturing decreased by 5%, reversing a four-month growth streak. Durable goods manufacturing has been on a downward trend since mid-2023, with a further 1% drop in August. Transportation equipment was a significant contributor to this decline, with several auto plants in Ontario undergoing retooling and maintenance.

- Finance and Insurance: This sector led monthly contributions to GDP growth among services, expanding by 0.5% in August. Significant trading activity in fixed-income markets is attributed to the expanded activity in the sector.

- Retail: Retail expanded again in August, with a 0.6% increase primarily driven by a 4.1% rise in new car purchases. Excluding motor vehicles, however, retail sales spending declined by nearly 1% month-over-month.

- Public sector: The sector posted a 0.2% increase, with municipal administration (+0.6%) and healthcare and social assistance (+0.2%) as the main contributors.

- Utilities: The sector contracted 1.9%, reversing a three-month growth streak. Lower electricity demand for cooling, following heightened demand in July in Western Canada, drove electric power generation down by 2.6%.

- Transportation and Warehousing: This sector declined 0.3% in August, marking its second consecutive contraction. Temporary rail disruptions in July and a bridge collapse in Fort Frances, Ontario, impacted rail traffic. July’s wildfires in Jasper also led to a 4% decline in the sector last month.

OUTLOOK AND IMPLICATIONS

The advanced estimate for real GDP in September is 0.3%, putting the third quarter on track for annualized 0.8%, which is still much lower than the Bank of Canada’s 1.5% Q3 forecast in its latest Monetary Policy Report.

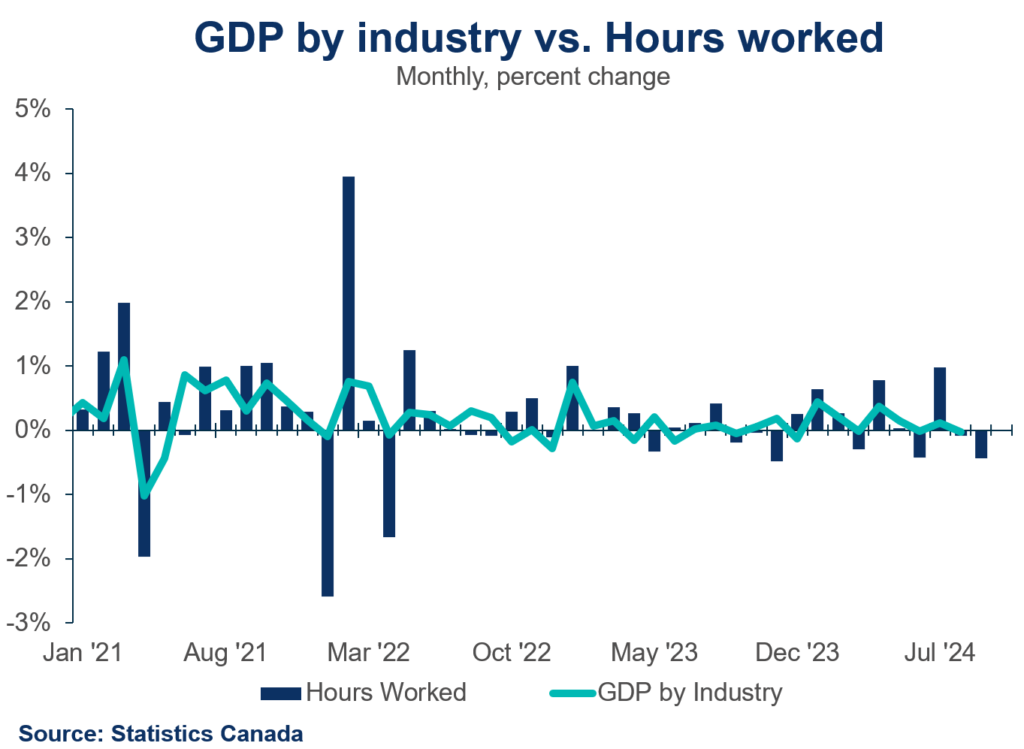

With the Labour Force Survey showing a decline in hours worked in September, the expected growth rebound by the September estimate may be tempered, signaling further slowing and risk to the Q3 forecast. Additionally, recently announced immigration targets add significant population growth pressures, which has been a key economic driver.

The hope is that per person consumption will pick up, but more time will be needed to see this trend reverse course. Governor Macklem continues to highlight in recent speeches that an increasingly uncertain outlook poses risks to the Canadian economy. The bottom line is that economic growth in August wasn’t the treat we were hoping for, but the bigger prize is on its way with the Bank expected to lower its policy rate again in December, just in time for Christmas.

SUMMARY TABLE

CHARTS

Other Blogs

Canada’s economy on pace to rebound in the first quarter

Use it while you can: The federal government spends its growth-driven fiscal windfall

A Solid Start, but Signs of Fatigue Emerging: Retail Sales February 2026

Inflation rises on energy shock, but underlying price pressures muted.

Sticky hiring, but wage growth at its highest since 2024: Labour Force Survey March 2025

Volatile Imports Drive Wider Deficit Despite Export Rebound: Merchandise Trade February 2026

January 2026 GDP: Canada’s economy kicks off 2026 on decent footing

Strong Start to the Year, but Underlying Momentum Remains Fragile: Retail Sales January 2026