Blog /

April 2025 GDP: The shoe drops as the economy shows trade impacts.

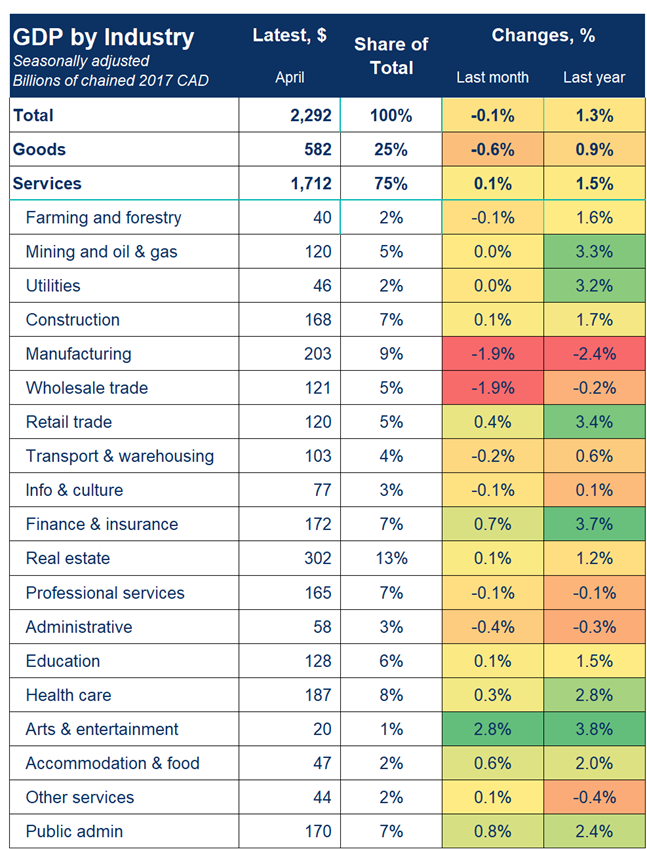

Real gross domestic product dropped 0.1% in April, below expectations of flat growth.

Andrew DiCapua

Share:

“The shoe has dropped, and the Canadian economy is set to contract this quarter. The focus now is assessing just how big that shoe will be. After months of mixed signals and soft survey data, the anticipated slowdown is showing up in the numbers. Trade-exposed sectors like manufacturing are sliding into a second straight month of decline, with no rebound in sight. The Bank is bracing for a weak second quarter, even as it grapples with stubborn inflation. At this juncture, they may soon come to realize that the downside risks will prevail.”

In the first quarter, businesses warned that trade tensions were a problem. Now, they’re painting a much bleaker picture. Even though growth beat the Bank of Canada’s forecast, it’s hard to ignore the underlying weakness. The Bank should move to cut rates by 25 basis points at their next meeting to give the domestic economy a much-needed cushion.”

KEY TAKEAWAYS

Real gross domestic product dropped 0.1% in April, below expectations of flat growth. This decline was driven lower by 10 of 20 sectors, with goods-producing sectors declining 0.6%, and the services sector edging up 0.1%.

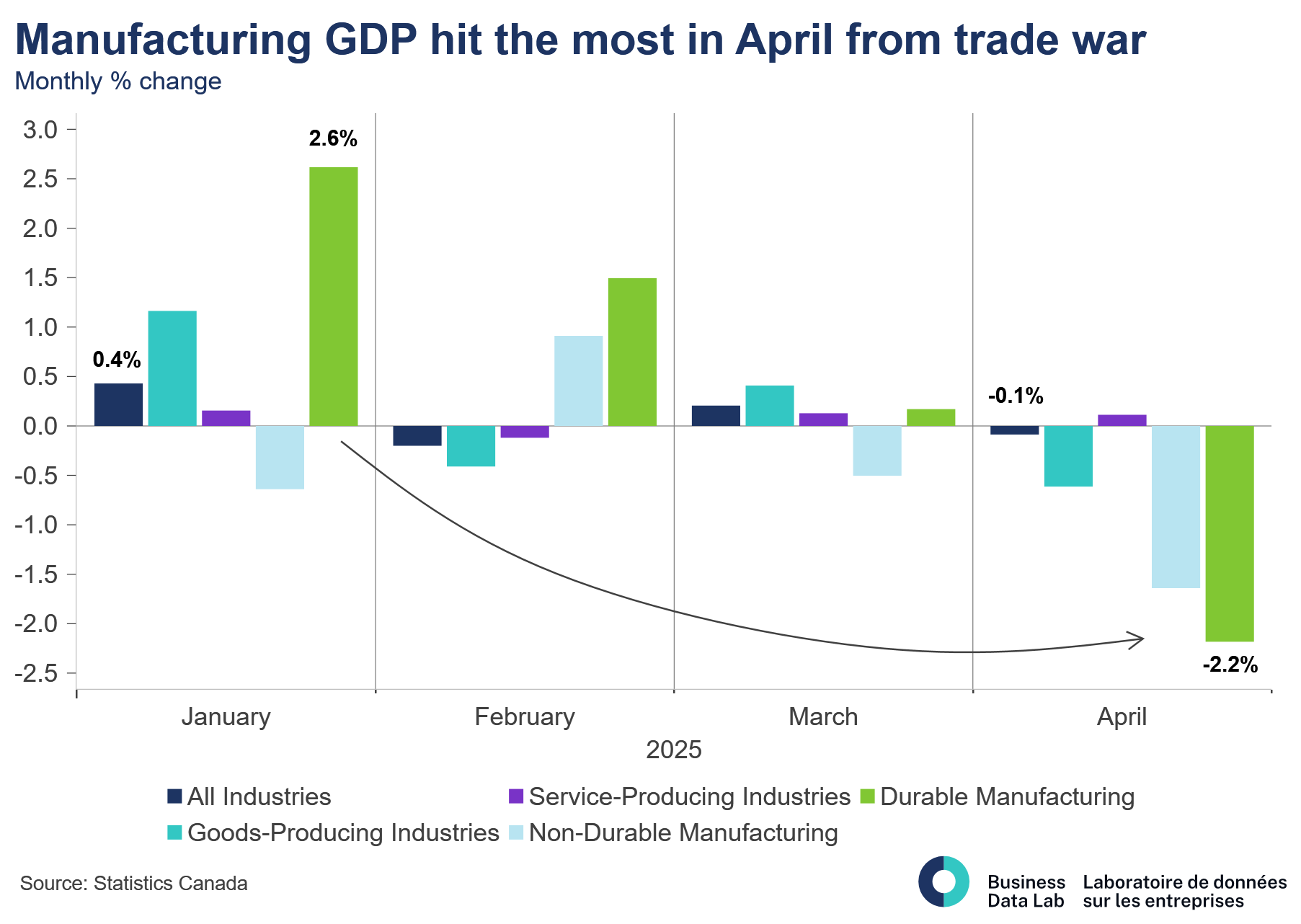

Bigger isn’t better here. The data confirm what we’ve been saying for months: the shoe has finally dropped and Canada’s economic resilience is fading. With momentum slowing, Q2 is now set to contract—led squarely by trade-exposed sectors like manufacturing, wholesale trade and transportation.

Manufacturing experienced a broad-based decline, contracting 2%. The third monthly decline for the sector was led by transportation, which was down 22% as production scaled back as uncertainty mounted due to U.S. tariffs.

Wholesale trade contracted 2% in April mostly because of less activity in the autos sector and trading of machinery and equipment. Trade in these goods fell significantly in April, resulting in weaker economic activity.

Mining, oil, and gas extraction was unchanged in April. Support services for grew on the month by 5%, offsetting the 0.6% decline in oil and gas extraction. Slower production volumes were impacted by pipeline ruptures and maintenance of key sites.

A notable mention to the public sector, which expanded in April by 0.4% driven by higher activity associated with the federal election. Public administration expanded for the first time in nine months.

OUTLOOK AND IMPLICATIONS

The advance estimate for real GDP in May came in at –0.1%, which puts Q2 on track for a mild 0.3% annualized contraction. That’s a touch weaker than what the Bank of Canada sketched out in their milder April Monetary Policy Report scenario, when they saw Q2 growth between flat and –1.25%.

It’ll be important to pin down how much of manufacturing’s decline is just pulled-forward demand versus deeper, structural challenges due to tariffs. Hours worked were essentially flat in May, and early signs show both manufacturing and wholesale trade slipping again—setting us up for another soft monthly GDP reading in May.

In June, the Bank of Canada held its policy rate steady because the Governing Council didn’t see clear signals to move. This new data pushes downside risks higher on their radar, even as inflation stays front of mind. They will get a clearer read on the domestic picture soon, moving them to lower interest rates once again in July.

Other Blogs

Inventory drawdown causes GDP to knee jerk into contraction despite improving fundamentals.

Momentum stalls as consumer shifts into a lower gear: Retail Sales December 2025

Diversification Gains Traction as Exports Close the Year Stronger: Merchandise Trade December 2025

6 Predictions for the Canadian Economy in 2026

Conflicting signals as both unemployment and employment rate declines: Labour Force Survey December 2025

Canada’s Productivity Gap Is a Vulnerability We Must Fix

Weak economic momentum could spell fourth quarter contraction.

Gold Payback and Auto Tariffs Push Canada Back into Deficit: Merchandise Trade November 2025