Blog /

8 Predictions for Canada’s Economy in 2025

The Canadian Chamber’s Chief Economist looks to the year ahead.

Stephen Tapp

Share:

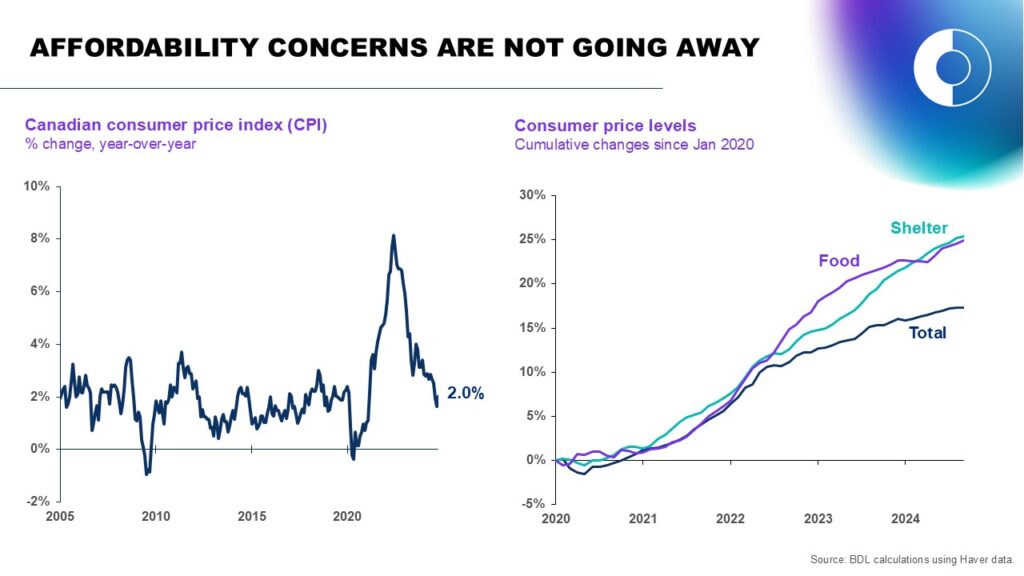

1. Affordability will remain a key consumer and political concern

A big story in 2024 was that inflation was tamed faster than expected. As a result, central banks in advanced economies have started cutting interest rates. The Bank of Canada kicked off the easing cycle among the G7 countries in June.

Inflation in Canada is now back at the Bank’s 2% target and has been inside the inflation control band for the past 10 months. For the time being, we can call this the “soft-ish landing” that few economists thought possible.

But there are no victory parties planned. With inflation targeting, central banks perpetually look ahead, so bygones are bygones. And we’ve just lived through a generational overshoot of the price level, which is up almost 16% since the start of the pandemic. It would have been closer to 8% if inflation was at target.

For some essential items, like food and shelter, prices have increased even more. This leaves many households struggling, and politicians searching for policy offsets — a trend that will continue in 2025 and will be a recurring theme in the upcoming federal election.

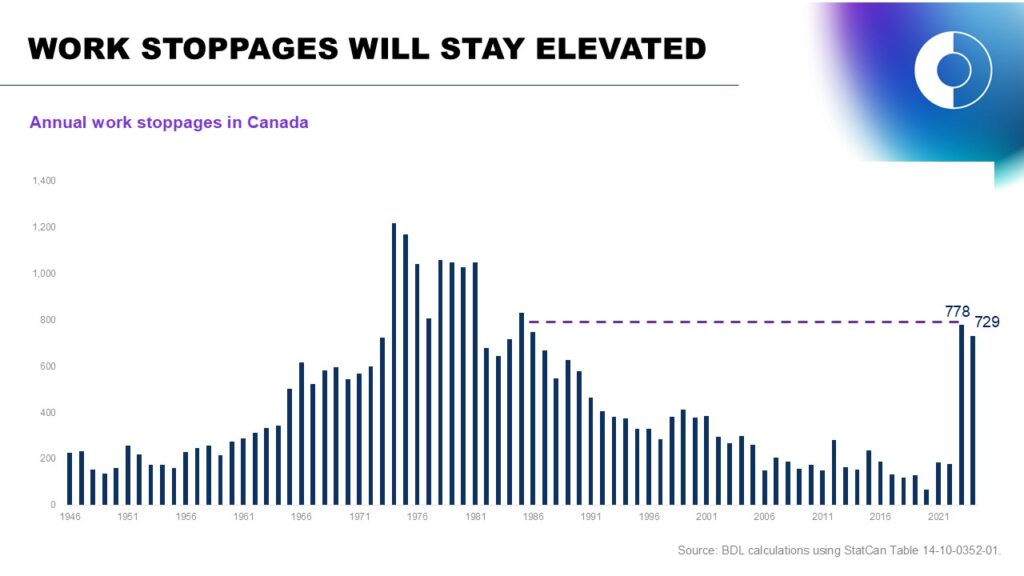

2. Work stoppages will remain elevated

With the overshoot in prices, pressure for wages to catch up followed — at a time when Canada’s labour productivity has been falling. Take rising unit labour costs for businesses, add in workers’ anxieties about affordability and automation, and the result has been a huge increase in work stoppages over the past two years. Alongside recent battles over postal services and public sector union contracts, several high-profile incidents have disrupted Canada’s supply chains through strikes or lockouts across ports, airports, and railways.

The last time we had this many work stoppages was almost 40 years ago. Given the persistent structural factors at play, expect this trend to continue in 2025.

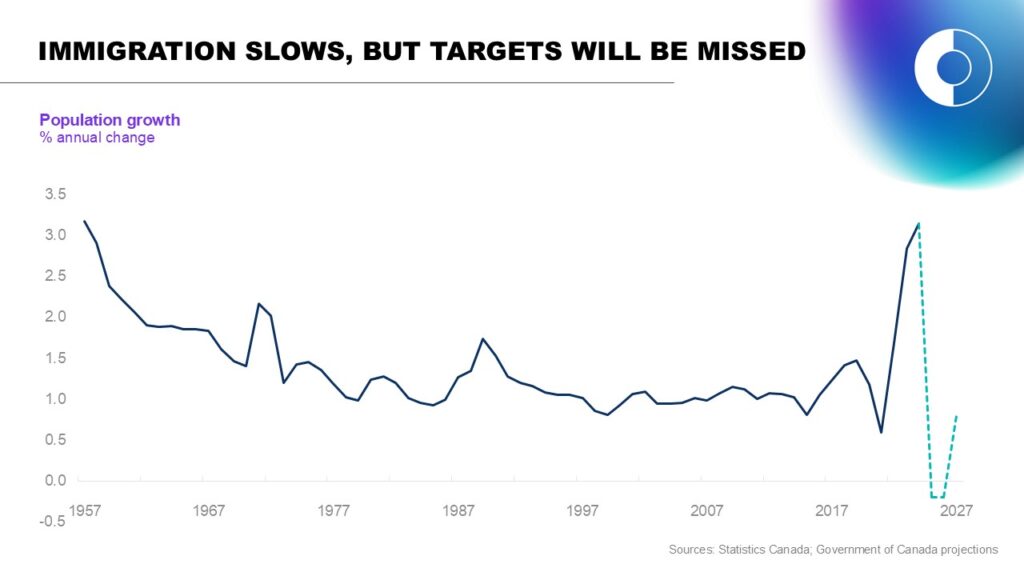

3. Immigration will slow down, but the government won’t hit its 2025 target

The federal government’s abrupt U-turn on immigration last fall is viewed by some as a potential “own goal”. After pandemic lockdowns lifted, Canada significantly increased immigration, led by non-permanent residents (i.e., international students and temporary foreign workers (TFWs)). We’ve recently had the fastest population growth in the last 60 years — over 3% annually, roughly three times faster than the typical growth over past decades.

Given Canada’s weak underlying productivity, we likely wouldn’t have avoided a recession without such fast population growth juicing the headline economic numbers. But these exceptional population inflows came at a time when the country’s absorptive capacity was limited, thereby exacerbating housing shortages as well as healthcare and infrastructure challenges.

The government’s new targets are to reduce the non-permanent resident population share from over 7% to 5% by the end of 2026. A key concern about this change is not the policy objective, but the proposed speed of implementation. Slamming on the brakes this hard could be bad for business, hurting those that rely on TFWs, as well as exposing funding gaps in our post-secondary education system. With these announcements, Canada’s population growth is on track to go into reverse in 2025, causing a significant drag on headline economic growth. I would be surprised if, in an election year, the government hits the ambitious target to slow immigration this much, this fast.

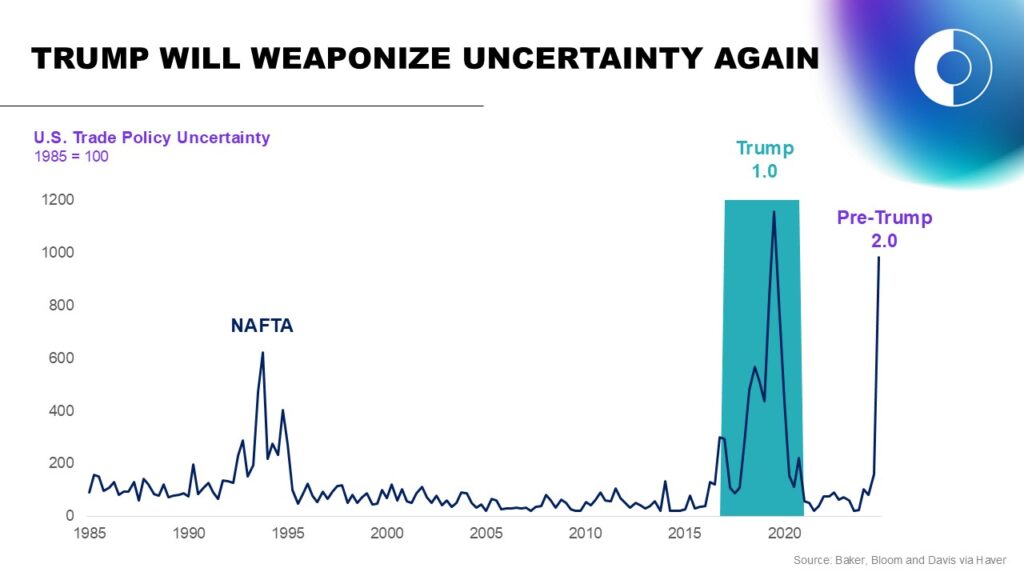

4. Trump will weaponize uncertainty and impose tariffs on Canada’s exports

In the coming year, President Trump will attract non-stop media attention, that much is obvious. But of all the uncertainties for Canada’s economy in 2025, the most consequential is whether Trump will impose tariffs on our exports.

While his tariff threat was launched sooner, and was larger than expected, this move is no surprise coming from the “Tariff Man”. This isn’t the first, and it won’t be the last tariff threat from Donald Trump. In his first term he famously tweeted that, “trade wars are good and easy to win”. He threatened to withdraw from NAFTA and imposed tariff threats on autos — following through on steel and aluminum — all while launching a trade war with China.

Trump’s objectives are to bully, destabilize and extract concessions. But what if he’s also looking for a way to raise revenue to partially fund his corporate tax cuts? That may be the most concerning of all his constantly shifting motivations.

My base case for 2025 is that Trump will impose tariffs on Canadian exports, almost immediately after his inauguration. Our BDL modelling suggests such a move would be disastrous for North America’s economy. Even the threat of tariffs will pause major investment decisions in Canada this year.

I expect some key sectors that will be majorly disrupted, such as energy and autos, will eventually receive exemptions from this self-defeating policy that will raise costs for U.S. businesses and consumers. But if Trump really is hell-bent on tariffs, then Canada is unlikely to get out of this unscathed in the short term. However, looking further down the road, I have much more conviction that the economic ties that bind us together will be strong enough that ultimately a trilateral North American trade pact will continue after Trump’s second term ends.

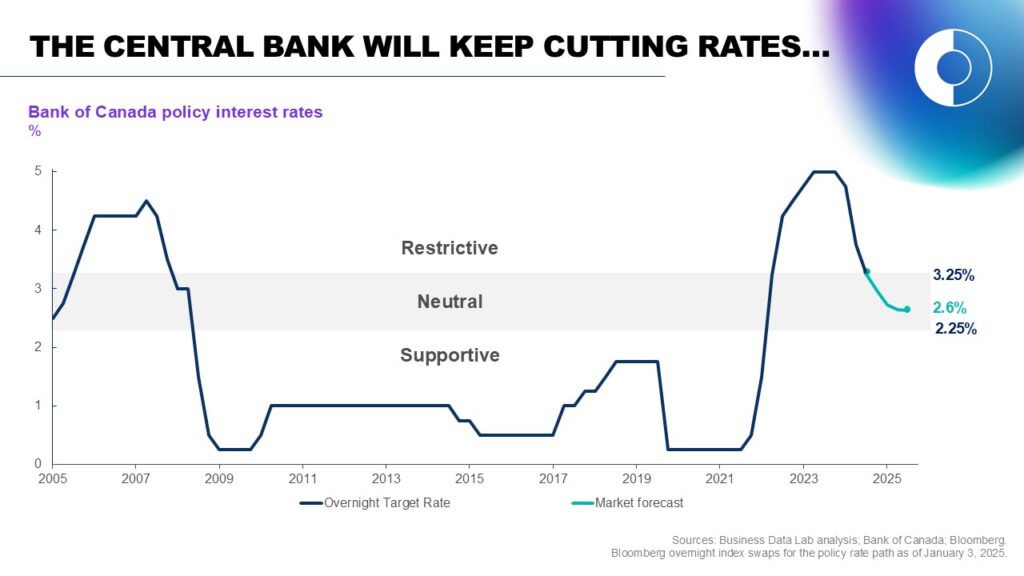

5. The Bank of Canada will continue cutting interest rates and the Canadian dollar will depreciate further

The Bank cut rates at its last five meetings of 2024, bringing its policy rate down from 5% to 3.25%. With inflation back under control, this finally brings policy from being “restrictive” to the top-end of the “neutral” zone (which the Bank estimates to be between 2.25% and 3.25% for its policy rate; a rate that neither stimulates nor restricts economic activity).

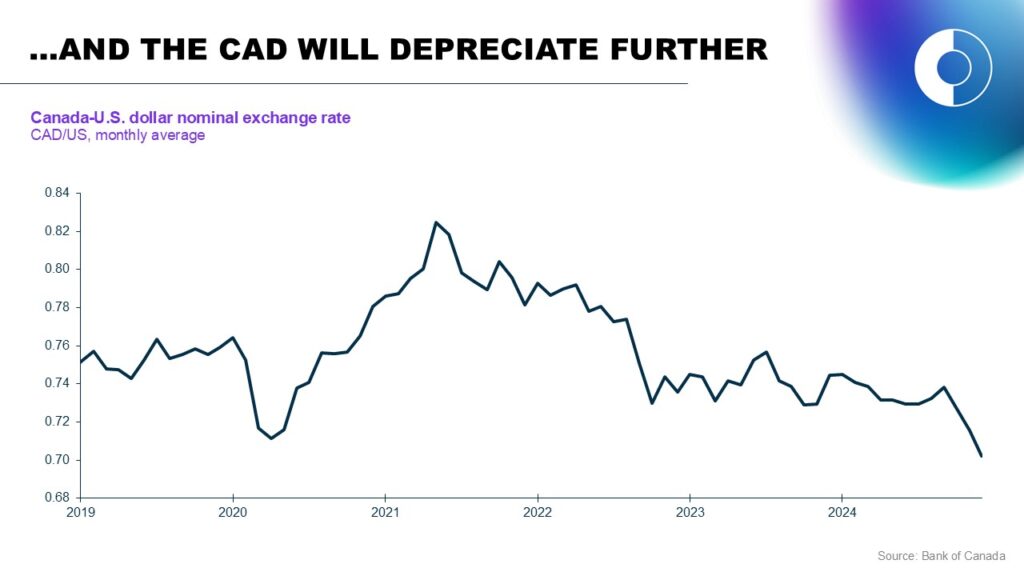

Financial markets have priced in a few more rate cuts, bottoming out around 2.6%. I think that will probably prove to be too optimistic, given the potential for the two large negative shocks noted above: 1) Trump’s tariffs; and 2) slower immigration. If the tariff threat alone is realized, then short-term Canadian interest rates need to go much lower to support activity. Given a diverging outlook for monetary policy relative to the U.S., the Canadian dollar would have further to fall, which will partially cushion the blow, but that will raise import prices and make Canadians rethink their travel plans to the U.S. this year.

6. Canadian trade will initially outperform expectations

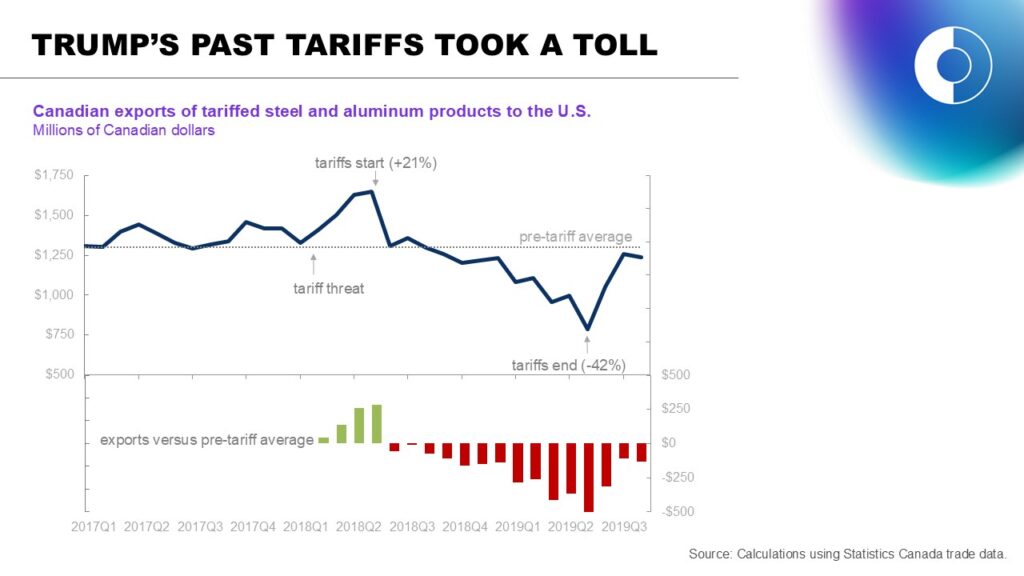

The unfortunate experience of steel and aluminum tariffs — which Trump used in his first term to extract concessions during NAFTA renegotiations — offers some guidance on the potential impacts if tariffs are imposed again.

In that case there was an initial period when businesses “stockpiled” inventories before the tariffs came into force. We expect a similar dynamic this time around. Indeed, in my recent presentations to local chambers, several business owners have noted this strategy at play.

As such, I expect Canadian exports to outperform expectations, at least very early in 2025, as U.S. importers rush to avoid potential tariffs. And if/when tariffs are enacted, a further depreciation of the Canadian dollar will provide some offset.

Last time around, after tariffs came into force, steel and aluminum exports fell fast, from 20% above the pre-tariff level to 40% below them. All told, we estimate that exports of these products fell about 16% (or $2.4 billion) over the 13 months of the tariffs.

We also expect Canada to impose retaliatory tariffs on U.S. imports.

7. Housing prices will rise again

With lower borrowing costs, combined with new mortgage rules to extend amortizations, along with the painfully slow process to raise housing supply, I expect average home prices in Canada to rise above $700,000 in 2025, causing more concern for first-time home buyers. This price level was only seen for a few months at the start of 2022. New record highs in the next few years shouldn’t be ruled out.

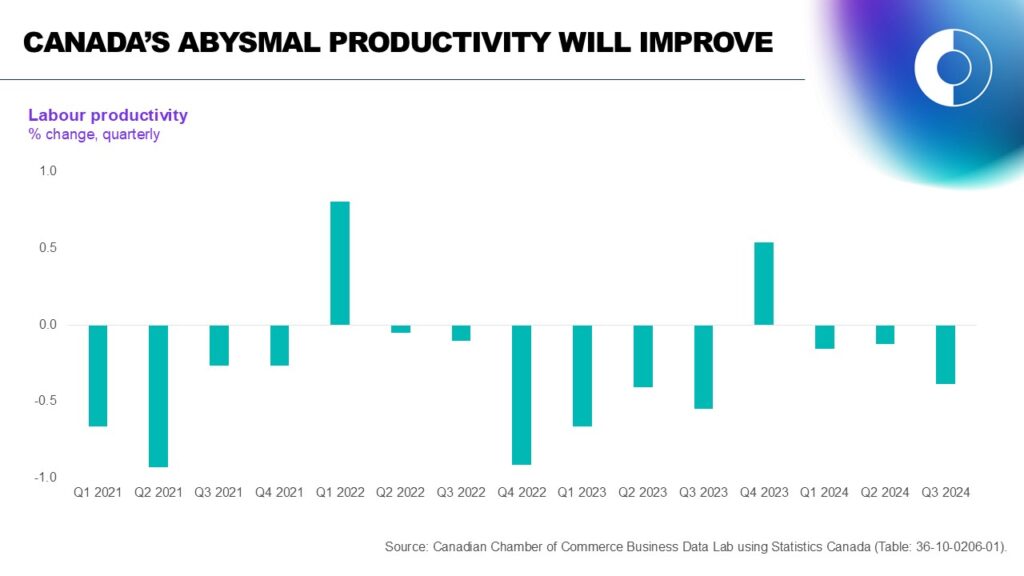

8. Canadian productivity will be less awful

I’ll end with a mildly optimistic outlook for Canada’s productivity — if only because it’s been so bad for the last few years that I hope things can’t get worse in 2025.

The latest data show that labour productivity fell for the third consecutive quarter and has dropped 15 times in the last 17 quarters!

Canadians are working harder, not smarter. We’re putting in more hours. Unfortunately, output growth isn’t keeping pace. The result is less output produced per hour.

Here’s hoping that this year, with lower borrowing costs, businesses and workers will ambitiously invest in new technologies to uncover better, faster and cheaper ways to create value. It’s desperately needed and something everyone can raise a glass to!

Other Blogs

Volatile Imports Drive Wider Deficit Despite Export Rebound: Merchandise Trade February 2026

January 2026 GDP: Canada’s economy kicks off 2026 on decent footing

Strong Start to the Year, but Underlying Momentum Remains Fragile: Retail Sales January 2026

Bank of Canada holds interest rates on cloudy conditions downplaying oil price risk to inflation

The dip before the spike, as base effects bring inflation below 2%

Labour market softens as job losses mount and youth unemployment climbs: Labour Force Survey February 2025

Auto Shutdowns Reverse Canada’s Export Momentum: Merchandise Trade January 2026

Inventory drawdown causes GDP to knee jerk into contraction despite improving fundamentals.