Strong Start to the Year, but Underlying Momentum Remains Fragile

Retail Sales January 2026

Jasleen Trehan

Share:

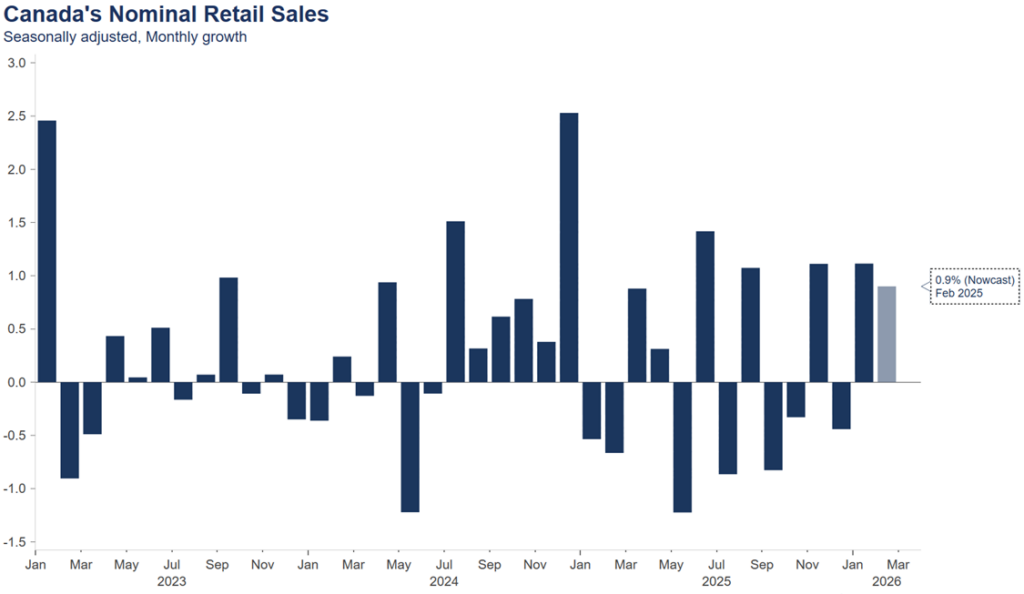

Canadian retail sales rose 1.1% in January with every province advancing. This broad-based rebound suggests December’s weakness was transitory. Autos led the monthly gain with core spending still up nearly 1%, grocery sales fell 0.7%, signaling that Canadians are potentially loosening up. Gasoline station sales slipped in January. Rising oil prices and Middle East conflict risk are poised to add inflationary pressure at precisely the wrong moment for stretched household budgets. Statistics Canada’s advance estimate points to a further gain in February. But the real test lies ahead as trade tensions, a cooling labour market, and energy price pressures become visible in the data.

Key Takeaways

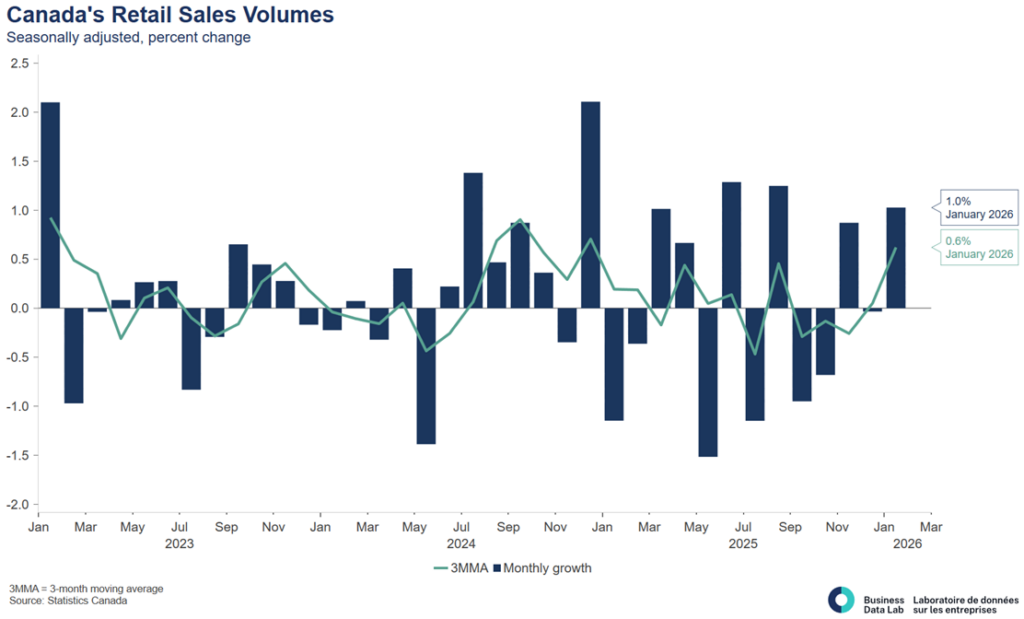

- Overall performance: Retail sales rose 1.1% m/m to $70.7B in January, with real (volume) sales up 1.0%, confirming a solid start to the year driven by genuine activity rather than price effects. The rebound from December suggests the late-year slowdown was likely temporary. Core retail sales rose 0.9%, indicating moderate but steady underlying demand.

- Strengths: Gains were broad-based across six of nine subsectors, with motor vehicle and parts dealers (+2.0%) leading the rebound after December’s decline. General merchandise (+3.0%), sporting goods/miscellaneous (+2.6%), and health & personal care (+1.2%) also advanced, pointing to continued resilience in both discretionary and essential spending categories.

- Weakness: The composition of growth remains uneven. Core momentum was moderate, and food and beverage sales declined (-0.6%, grocery -0.7%), suggesting some pullback in essential spending. Gasoline sales (-0.4%) also fell. The reliance on autos to drive headline gains highlights that broader consumer demand remains cautious rather than accelerating.

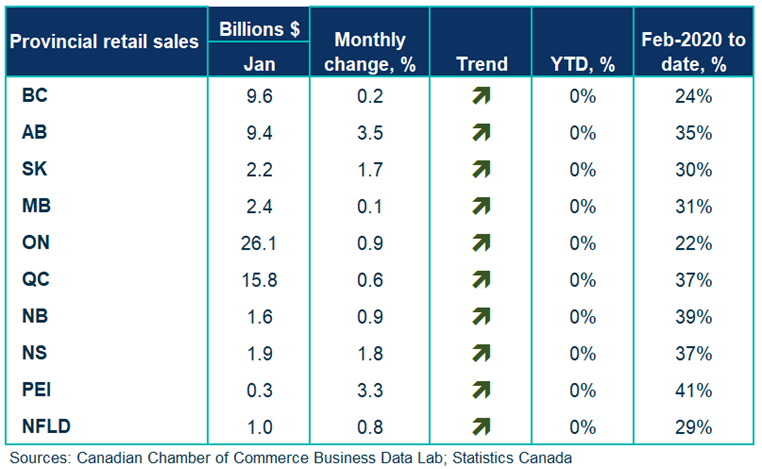

- Regional trends: Sales increased in all provinces, marking a shift from December’s more uneven performance. Alberta (+3.5%) led gains, while Ontario (+0.9%) and Quebec (+0.6%) posted more modest increases. The breadth of gains indicates a synchronized national rebound rather than region-specific strength.

- Advance estimate: StatCan’s advance estimate suggests a further +0.9% m/m increase in February, pointing to continued near-term resilience in retail activity.

After a weak finish to 2025, retail activity has rebounded early in the year, but the composition of growth points to a consumer that remains cautious. With rising energy prices, trade uncertainty, and a cooling labour market, current resilience is likely to face increasing pressure as real purchasing power becomes more constrained.

Tables

Charts

Other Blogs

Consumers Return to the Checkout with Broader Spending

Inflation cools ahead of the summer months

The Bank of Canada gains more confidence in growth prospects despite inflation risk

Canada’s labour market finally caught a bit of a break in June: Labour Force Survey May 2026

Record Exports Signal a Broader Trade Story: Merchandise Trade May 2026

Canada’s economy starts the second quarter with firmer footing

The Inflation Gap Widens as Price Pressures Spread Beyond Energy: May 2026 CPI

Consumers Keep Spending, but the Menu Is Narrowing