GDP November 2025

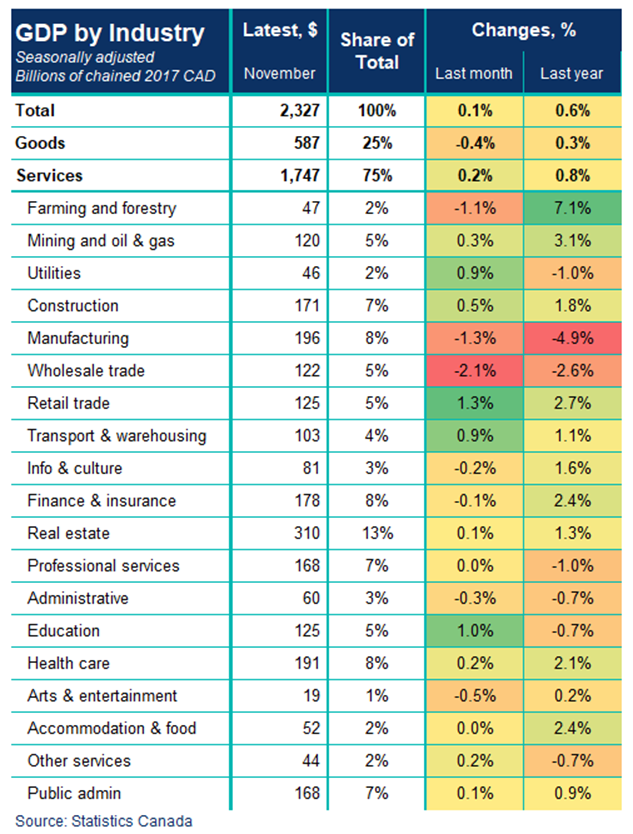

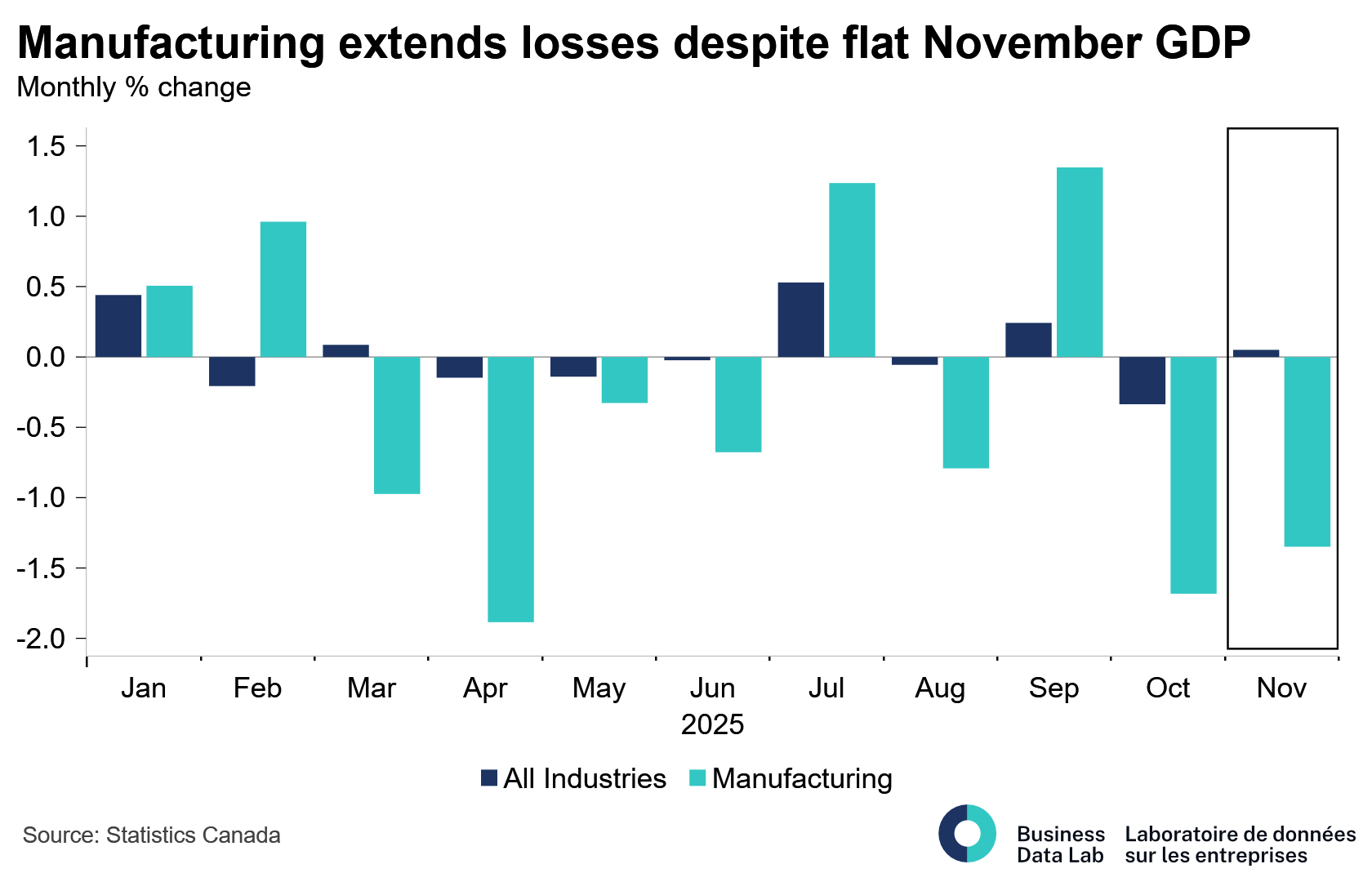

Real GDP was unchanged in November providing no relief to the Canadian economy following a -0.3 contraction October.

Andrew DiCapua

Share:

The Canadian economy likely ended the year without momentum to launch into 2026. November GDP suggests the trade war showed accelerated weakness in the manufacturing sector with little rebound in December. With recent export weakness in manufacturing, it is likely this story isn’t over. While today’s GDP report was mixed, overall growth in the fourth quarter now appears likely to come in below both the Bank of Canada’s latest forecast and BDL’s nowcast.

Key takeaways

Real GDP was unchanged in November providing no relief to the Canadian economy following a -0.3 contraction October. November’s GDP was pushed down by goods-producing sectors which declined 0.3%, while services were up only 0.1%. The goods sector posted its third monthly decline in four months, signaling weakness in manufacturing in the final months of 2025. All together, GDP for 2025 is expected to grow 1.3%, below current consensus forecasts.

The manufacturing sector was a key source of weakness, with a 1.3% drop driven by both durable and non-durable goods segments. Transportation equipment, machinery, and fabricated metal manufacturing all weakened alongside ongoing supply chain pressures, including semiconductor shortages that hampered automotive output. Non-durable goods also contracted, reflecting softer food and plastics production.

The wholesale trade sector also weakened, falling 2.1%, the largest drop in many months, largely due to lower activity in motor vehicle and building material wholesaling. Together, these patterns reflect persistent slack in the industrial and distribution backbone of the Canadian economy.

Retail trade posted a solid gain as all subsectors expanded, helping offset some of the manufacturing drag. Meanwhile, the public sector buoyed by a rebound in educational services and steady growth in health care and administration contributed positively. Transportation and warehousing also saw growth, aided by a rebound in postal services.

However, these gains, while important, were not enough to lift overall monthly growth meaningfully,

Implications

Statistics Canada’s flash estimate for December GDP is +0.1%, which would put the fourth quarter on track to contract 0.5% on an annualized basis. The Bank of Canada in their latest January Monetary Policy Report in forecasting flat Q4 GDP growth. BDL’s nowcast is tracking a more positive quarter, expecting 0.8% growth, but this is expected to be weaker. It is likely the quarter will be positive but muted.

All together, the Bank of Canada holding interest rates this week was an expected move as they enter a year where structural forces will test the resilience of the Canadian economy. The Bank of Canada will likely be on hold for the next few meetings, but trade-exposed sectors will continue to experience weak performance. of Budget 2025—particularly in delivering capital investment—will be key to buffering the economy and supporting growth.

Other Blogs

The Inflation Gap Widens as Price Pressures Spread Beyond Energy: May 2026 CPI

Consumers Keep Spending, but the Menu Is Narrowing

The Bank of Canada faces a dilemma as it extends its holding pattern

Canada’s Trade Story Finds New Supporting Cast: Merchandise Trade April 2026

It is green across the board for May’s labour market: Labour Force Survey May 2026

Where Canada’s defence debate goes next

Recession or Resilience? An unexpected first-quarter GDP contraction points to an uphill battle.

Pivot or Peril: Are Canadian Cities Diversifying or Doubling Down on America?