Blog /

Q3 2025 GDP: Technically no recession as strong growth masks underlying weakness.

Canada’s economy blew past expectations, growing by 2.6% on an annualized basis in Q3 2025.

Andrew DiCapua

Share:

“Canada’s headline growth looks better on paper than reality. Despite exceeding BDLNow’s forecast of 2.2%, external conditions will continue to put pressure on the economy. We’ll need strong domestic demand to carry more of the load, but it simply wasn’t there in third quarter GDP. The sickly economy barely improved its trade position, mostly due to a record decline in imports. Households and businesses are still holding back, and the economy hasn’t found the momentum it needs to shift into a higher gear. The Bank of Canada will welcome the stronger growth but will monitor the details around domestic demand. This doesn’t tip the scale towards another interest rate cut at the December meeting.”

KEY TAKEAWAYS

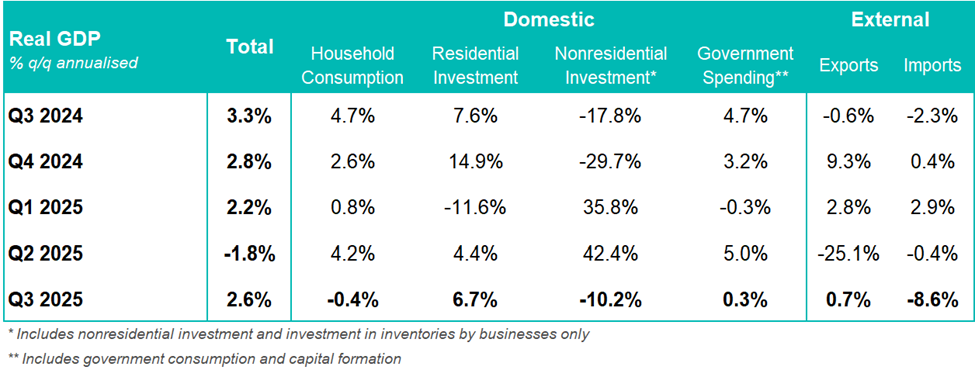

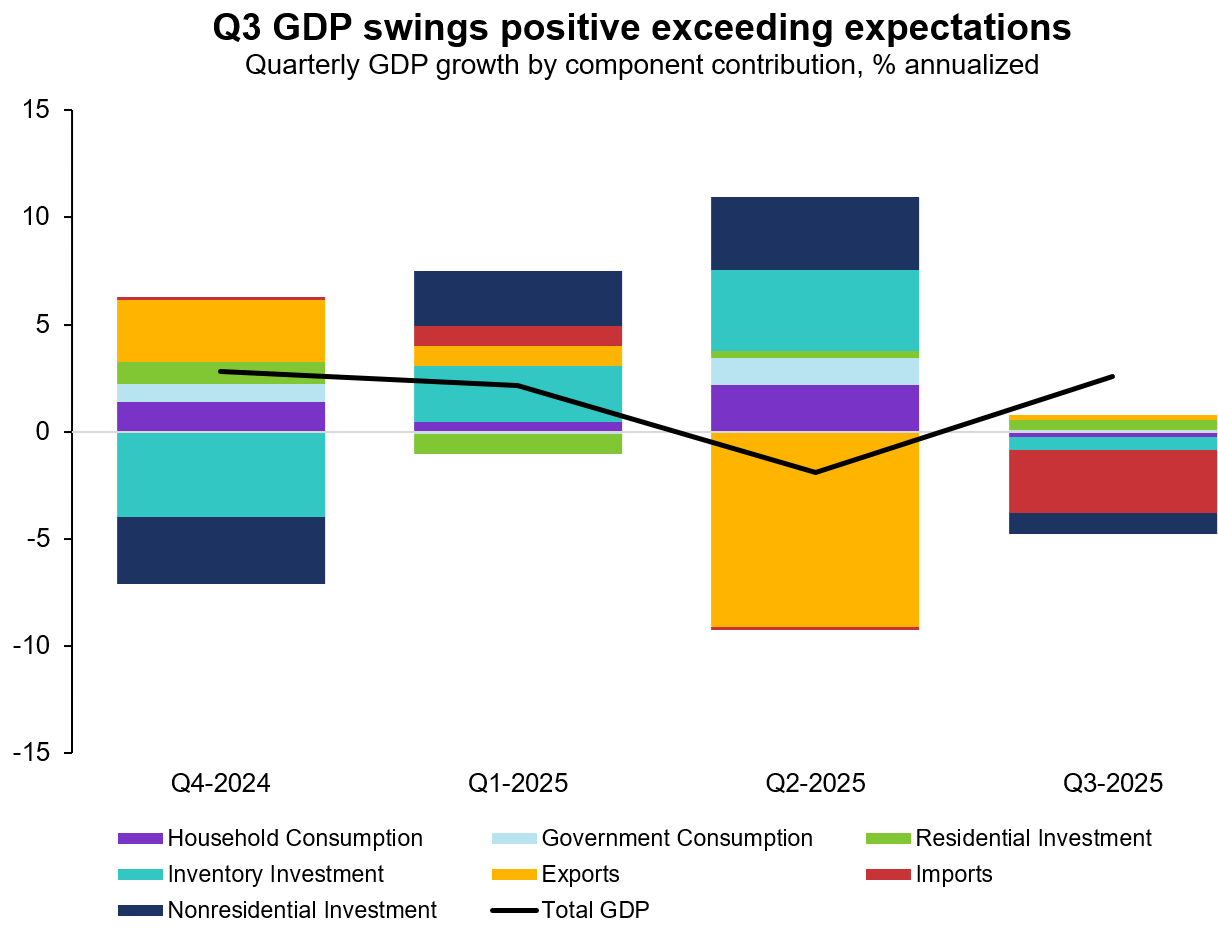

- Canada’s real domestic product (GDP) rebounded at an annualized rate of 2.6% in Q3 2025, well-above consensus expectations and the Bank of Canada’s forecast of 0.5%.

- On a per capita basis, GDP expanded by 0.5% in the third quarter.

- September monthly GDP rose by 0.2%, led by a rebound in the manufacturing sector.

- Q2 GDP was revised down from -1.6% to -1.8% contraction.

Exports only slightly recovered in the third quarter, rising 0.8% annualized after the steep 28% annualized drop in Q2 driven by U.S. tariffs. Crude oil and commercial services supported export growth in Q3, while precious metals pulled it down. Imports fell nearly 9% annualized creating a whiplash effect and wide net-trade contribution to GDP compared to a deficit in Q2—the sharpest decline since 2022. The largest declines were in precious metals and machinery and equipment imports.

Government capital investment also boosted third-quarter GDP, increasing 11.6% annualized due to higher purchases of military equipment and infrastructure. This momentum is likely to continue next year as the federal government ramps up spending to reach NATO’s 2% target.

Lower interest rates provided some optimism in the housing sector. Residential investment rose 6.4% annualized in Q3, driven by strong resale activity. In contrast, non-residential investment continued to slide, falling 10.2% annualized as machinery and equipment and intellectual property investment contracted again. Businesses also drew down inventories by nearly $4 billion, contributing to weaker overall investment.

Domestic demand was essentially flat. Household consumption declined 0.4% annualized in Q3, reflecting softer spending on passenger vehicles and rent. Canadians’ spending abroad also fell 16% annualized as preferences shifted toward domestic tourism. On a per-capita basis, consumption fell 0.8% annualized. The household savings rate, however, improved to 4.7% as income growth outpaced spending.

The goods-producing sector rebounded, with mining, oil and gas, real estate, construction, and manufacturing all expanding in the third quarter. Monthly GDP rose 0.2% in September, led by growth in oil and gas.

OUTLOOK AND IMPLICATIONS

Q3 GDP growth exceeded expectations from most economists—and even the Bank of Canada, which had forecast just 0.5% annualized. Statistics Canada’s advance estimate points to a 0.3% contraction in October, setting up Q4 GDP to grow at roughly 0.5% annualized, below the Bank’s outlook. We may have avoided a technical recession, but the domestic fundamentals that were strong in Q2 were largely absent in Q3.

Markets continue to price in no near-term rate cuts from the Bank of Canada. Economic risks remain tilted to the downside, and inflation is holding near target. The Bank signaled at its last meeting that monetary policy has little room left to stimulate growth. For now, it will remain on the sidelines.

Source: Statistics Canada

Other Blogs

Volatile Imports Drive Wider Deficit Despite Export Rebound: Merchandise Trade February 2026

January 2026 GDP: Canada’s economy kicks off 2026 on decent footing

Strong Start to the Year, but Underlying Momentum Remains Fragile: Retail Sales January 2026

Bank of Canada holds interest rates on cloudy conditions downplaying oil price risk to inflation

The dip before the spike, as base effects bring inflation below 2%

Labour market softens as job losses mount and youth unemployment climbs: Labour Force Survey February 2025

Auto Shutdowns Reverse Canada’s Export Momentum: Merchandise Trade January 2026

Inventory drawdown causes GDP to knee jerk into contraction despite improving fundamentals.