Blog /

Retail Sales September 2025: Retail sales stumble as autos drag down goods demand

Retail activity dipped in September, with weaker auto purchases showing consumers shifting into a more cautious gear.

Jasleen Trehan

Share:

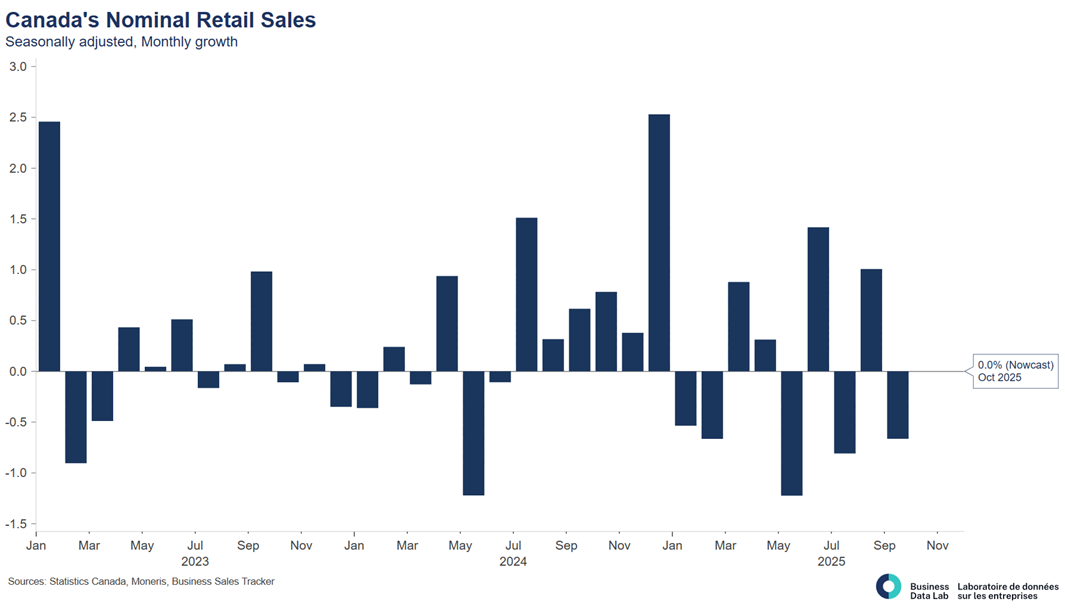

“September’s 0.7% drop in retail sales shows consumers tapping but not slamming the brakes. A pullback in auto purchases drove the decline, while the rest of the picture is far steadier. Excluding autos and gasoline, retail spending was essentially flat, and BDL’s Business Sales Tracker still shows solid year-over-year card-spending growth. Households aren’t retreating; they’re recalibrating. With inflation easing and early-fall job gains holding firm, today’s data points to a consumer adjusting to higher borrowing costs – resilient, but not strong enough to carry the recovery on its own, especially with Stat Can’s flat October flash estimate showing this softer momentum continuing into Q4.”

Key Takeaways

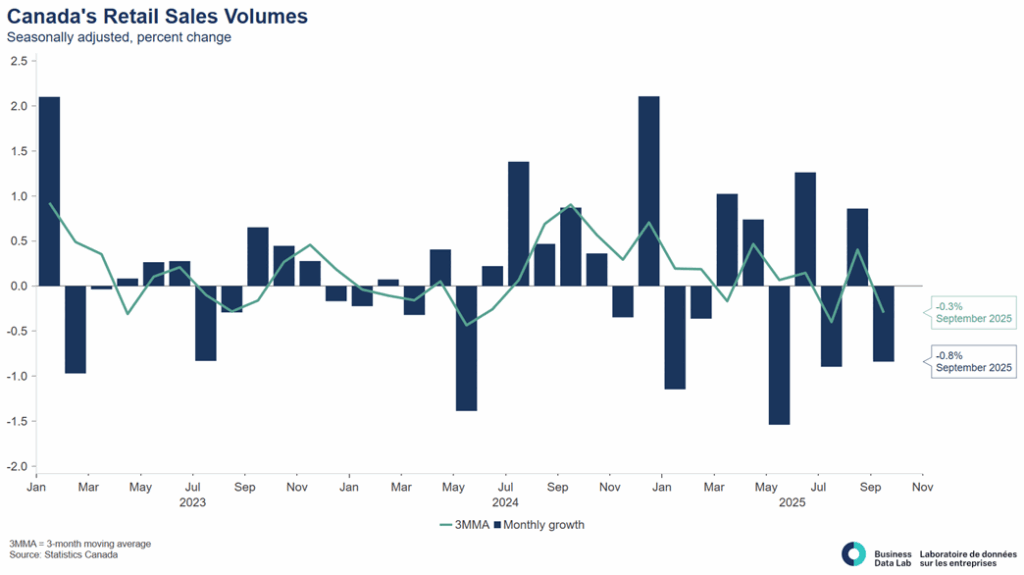

- Overall performance: Retail sales declined 0.7% m/m to $69.8B, with six of nine retail subsectors posting declines, driven largely by a sharp drop in motor vehicle and parts dealers. Real sales fell 0.8%, while core retail (excluding autos and gasoline) was essentially unchanged, pointing to concentrated – not broad-based weakness in September.

- Strengths: Food and beverage retailers rose 0.8%, supported by beer, wine and liquor (+3.4%), and discretionary categories such as sporting goods and miscellaneous retailers (+1.6%) posted gains.

BDL’s Business Sales Tracker continues to show solid year-over-year spending, indicating underlying consumer resilience even as monthly momentum cools. - Weakness: Motor vehicle and parts dealers fell 2.9% for the first time in three months, led by new car dealers -3.6%, reversing August’s strength. Building materials (-2.0%), general merchandise (-0.5%), and health & personal care (-0.2%) also softened, reflecting interest-sensitive and renovation-related spending pressures. Gasoline station receipts rose 1.9%, posting their first increase in three months, but real fuel volumes fell 1.0%, underscoring weaker underlying demand.

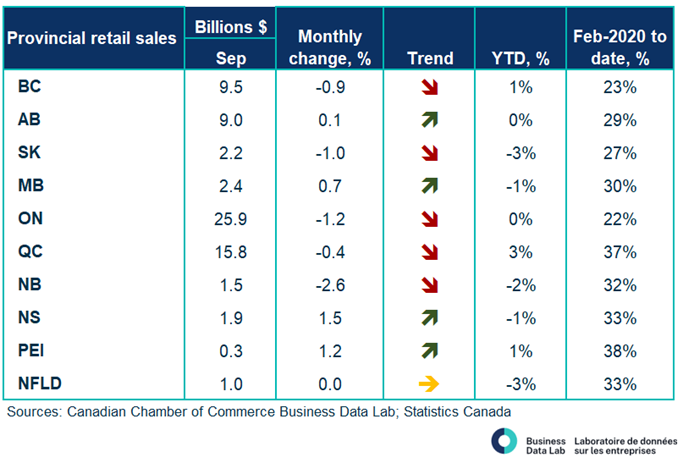

- Regional trends: Sales declined in six provinces, led by Ontario (-1.2%), New Brunswick (-2.6%), and B.C. (-0.9%). The Toronto CMA fell 2.3%, mirroring the sharp auto-led decline. Nova Scotia, PEI, and Manitoba recorded modest gains.

- Advance estimate: Looking ahead, StatCan’s advance estimate for October shows sales were flat again, suggesting the weaker momentum in household spending has carried into Q4. With real retail volumes slipping, goods-sector activity softening, and inflation easing, the consumer is resilient – but not strong enough to lift the economy without help. These conditions may give the Bank of Canada more room to consider rate adjustments next year, depending on how growth and inflation evolve.

- Canadian consumers continue to spend, but at a slower and more cautious pace as higher borrowing costs weigh heavily on autos and home-related purchases. Stable core sales, easing inflation, and steady job gains are helping anchor demand – but the overall trend points to a gradual cooling, suggesting the Bank of Canada may have more flexibility to adjust policy in 2026.

Tables

Charts

Other Blogs

Canada’s economy on pace to rebound in the first quarter

Use it while you can: The federal government spends its growth-driven fiscal windfall

A Solid Start, but Signs of Fatigue Emerging: Retail Sales February 2026

Inflation rises on energy shock, but underlying price pressures muted.

Sticky hiring, but wage growth at its highest since 2024: Labour Force Survey March 2025

Volatile Imports Drive Wider Deficit Despite Export Rebound: Merchandise Trade February 2026

January 2026 GDP: Canada’s economy kicks off 2026 on decent footing

Strong Start to the Year, but Underlying Momentum Remains Fragile: Retail Sales January 2026