Blog /

May 2025 GDP: The economy is still swimming.

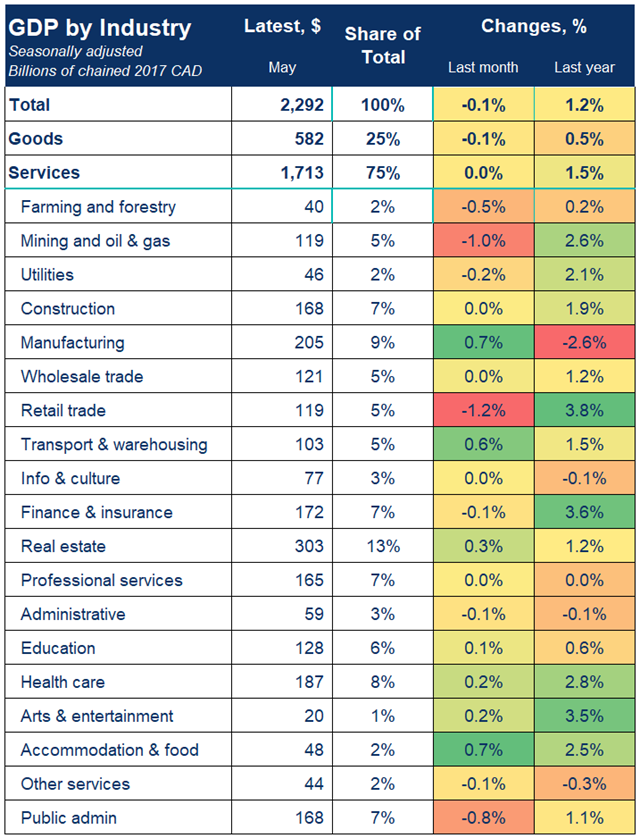

Real gross domestic product dropped 0.1% in May, but the worse from the trade war might be behind us.

Andrew DiCapua

Share:

“The 0.1 % contraction in Canada’s GDP for May was in line with expectations, but a rebound in manufacturing, mostly from temporary inventory build-ups masked deeper weakness. Trade affected sectors are still trending down, yet stronger hours worked in June suggest the StatsCan positive flash could come true. All together, the data looks more resilient. While second-quarter GDP is still expected to contract, these upside surprises help support yesterday’s decision to keep rates on hold, for now”

KEY TAKEAWAYS

Real gross domestic product edged down once again by 0.1% in May, in line with expectations. This decline was driven lower by 13 of 20 sectors, with goods-producing sectors declining 0.1%, and the services sector essentially unchanged.

May GDP was mixed, with the overall picture of an economy treading water. May data were influenced by a temporary build up in inventories in the manufacturing sector, higher transportation rail and pipeline activity, and real estate activity.

Manufacturing rose 0.7% on the month following a record contraction in April, led by durable goods. This was largely due to a build up in inventories for businesses in aerospace and fabricated metals and we expect this to be temporary. Manufacturing GDP for the first five month of the year is trending below 2024 levels.

Transportation and warehousing grew 0.6% in May, following declines in April from decreases activity due to tariffs. Rail volumes rebounded from April and pipeline flows for both crude oil and natural gas are continuing growth

Retail trade contracted 1.2% led by lower sales of motor vehicles and parts, followed by food and beverage and gasoline sales. Vehicle sales remain above 2024 levels despite a downward trend in recent months. On a positive note, arts, entertainment and recreation grew 0.2% in May driven by two Canadian teams competing in the Stanley Cup Playoff finals.

Some temporary factors led to mining, oil and gas and public administration to post declines in May. Crude oil producers in Alberta were undergoing facility upgrades, and the pullback in workers for the federal election was a drag on public administration.

OUTLOOK AND IMPLICATIONS

The advance estimate for real GDP in June is expected to be +0.1%, which puts Q2 on track to avoid a contraction, which is still widely expected. The Bank of Canada anticipates in their July Monetary Policy Report, Q2 GDP to contract -1.5% annualized. Hours worked for June in the LFS rose 0.5%, supporting the flash estimate.

Governing Council is right to shift focus from inflation risks to economic weakness, but recent data suggests a rosier picture than originally anticipated. May’s GDP release although a contraction doesn’t show us the damage that we know to be evident. Holding its policy rate steady may be justified for now, but spillover impacts and the economic resilience we’ve seen so far will become more like the outlook describe in the Bank’s recent outlook as we approach their next decision in September.

Other Blogs

Canada’s economy on pace to rebound in the first quarter

Use it while you can: The federal government spends its growth-driven fiscal windfall

A Solid Start, but Signs of Fatigue Emerging: Retail Sales February 2026

Inflation rises on energy shock, but underlying price pressures muted.

Sticky hiring, but wage growth at its highest since 2024: Labour Force Survey March 2025

Volatile Imports Drive Wider Deficit Despite Export Rebound: Merchandise Trade February 2026

January 2026 GDP: Canada’s economy kicks off 2026 on decent footing

Strong Start to the Year, but Underlying Momentum Remains Fragile: Retail Sales January 2026