Blog /

Tipping the scale: Bank of Canada aims to reset pace and prioritize inflation expectations

The Bank of Canada held its interest rate at 2.75%.

Andrew DiCapua

Share:

“Today, the Bank of Canada sent a clear signal that while the outlook for the Canadian economy is uncertain, they’re increasingly concerned about inflation risks. Higher pricing and tariff costs highlighted in their latest survey tipped the balance of risks, leaving them to pause in absence of convincing data. I’m not surprised that the the Governor struck a relatively dovish tone, recognizing that incoming data will likely force the Bank to lower interest rates, which are not currently providing much stimulus to the economy.”

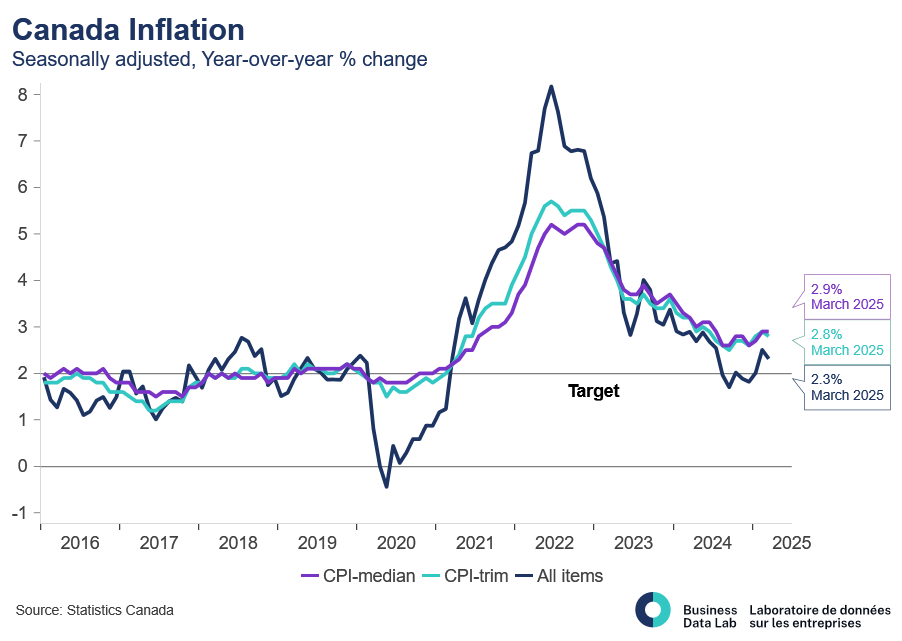

The Bank of Canada kept its policy rate at 2.75% as we expected. Following seven consecutive rate cuts since June 2024, the Bank focused on realigning monetary policy expectations. Recent increases in survey inflation expectations and the potential passthrough of higher supply chain costs tipped the scale for a rate pause. However, the dovish messaging shows Governing Council will move lower to support growth if economic activity falters. Markets were only pricing in a 40% chance of a 25 basis point cut, but many economic forecasters were expecting the Bank to move lower.

The Bank of Canada presents two scenarios in their April Monetary Policy Report (MPR), in lieu of their conventional projections.

“Scenario 1: we assume most of the new tariffs get negotiated away, but the process is unpredictable, and businesses and households remain cautious. GDP growth in this scenario stalls in the second quarter, then expands only moderately. Inflation drops below the 2% target for the rest of 2025 and into 2026, both because of the end of the consumer carbon tax and a weak economy.

Scenario 2: we assume a long-lasting global trade war. The economic consequences are severe. Canada’s GDP contracts in the second quarter and the economy is in recession for a year. Growth gradually returns in 2026 but remains soft through 2027 as US tariffs permanently reduce Canada’s potential output and lower our standard of living. Inflation rises above 3% in mid-2026 as tariffs, countermeasures and shifts in supply chains raise costs, pushing up many prices. Inflation then eases as weak demand limits ongoing inflationary pressures.”

The Canadian economy is between a rock and a hard place. The Bank of Canada is expecting much weaker growth in 2025 compared to 1.8% in their January forecast. The April MPR under their first scenario expects GDP to grow 0.4% in 2025. The worse-case scenario would place Canada in a recession, with four quarters of consecutive negative growth. We’ll likely end somewhere in the middle as fiscal stimulus and automatic stabilizers (i.e. exchange rate.etc) offset the impact on reduced demand for Canadian goods.

Canada’s inflation is expected to be lower in 2025 under both scenarios. The removal of the carbon tax starting in April will remove up to 0.7% inflation in 2025. Inflation is expected to be below 2% for most of this year, but the momentum heading into 2026 will depend on the scenario. The Bank expects inflation to rise above 3% in 2026 under the worse-case scenario.

The Bank expects a global recession in their scenarios. A global recession is typically considered growth below 3%. Under scenario 1, the global economy expands 2.6% in 2025, and is much lower at 1.6% under scenario 2. Coincidentally, The World Trade Organization (WTO) released their updated forecast for the global economy, based on the current policy environment. They forecast global growth in 2025 of 2.2, weaker than the Bank’s 2025 average under scenario 1 of 2.6%. Ultimately, we can expect the global backdrop weaker and a key risk to Canadian growth.

From a risk mitigation perspective, the Bank should’ve continued their path to lower interest rates. The Bank of Canada isn’t providing much stimulus to the Canadian economy, with estimates of a “neutral rate” (the rate which neither stimulates or restricts the economy) at around 2%. With very low consumer confidence and appreciation of the Canadian dollar, the pause could raise import prices and keep demand on the sidelines. Markets are pricing in a 25 basis-point rate cut at the June 4 meeting.

Other Blogs

Canada’s Trade Story Finds New Supporting Cast: Merchandise Trade April 2026

It is green across the board for May’s labour market: Labour Force Survey May 2026

Where Canada’s defence debate goes next

Recession or Resilience? An unexpected first-quarter GDP contraction points to an uphill battle.

Pivot or Peril: Are Canadian Cities Diversifying or Doubling Down on America?

Retail sales defy expectations, but spending may be running out of gas.

Inflation becoming more of an isolated energy story, for now : April 2026 CPI

Narrow Strait, Wide Impact: How a Global Shock Reaches Canada