Blog /

August 2023 CPI: Keep calm and carry on? But, we’re moving in the wrong direction.

Inflation in August will raise concern at the Bank of Canada and among many Canadians. With a 4% annual growth, surpassing market expectations of 3.8%, the summer months have provided a humbling reminder of the sensitivity of headline prices to volatile commodities like food and energy, with gasoline prices being the primary driver of this month's inflation.

Rewa

Share:

Inflation in August will raise concern at the Bank of Canada and among many Canadians. With a 4% annual growth, surpassing market expectations of 3.8%, the summer months have provided a humbling reminder of the sensitivity of headline prices to volatile commodities like food and energy, with gasoline prices being the primary driver of this month’s inflation. Many Canadian consumer and business surveys now show declining inflation expectations. The Bank of Canada, with one more month of data before its next policy meeting, faces mounting market expectations for another rate hike. We’ll likely see more upside surprises in the upcoming months.

Andrew DiCapua, Senior Economist, Canadian Chamber of Commerce

KEY TAKEAWAYS

Headline

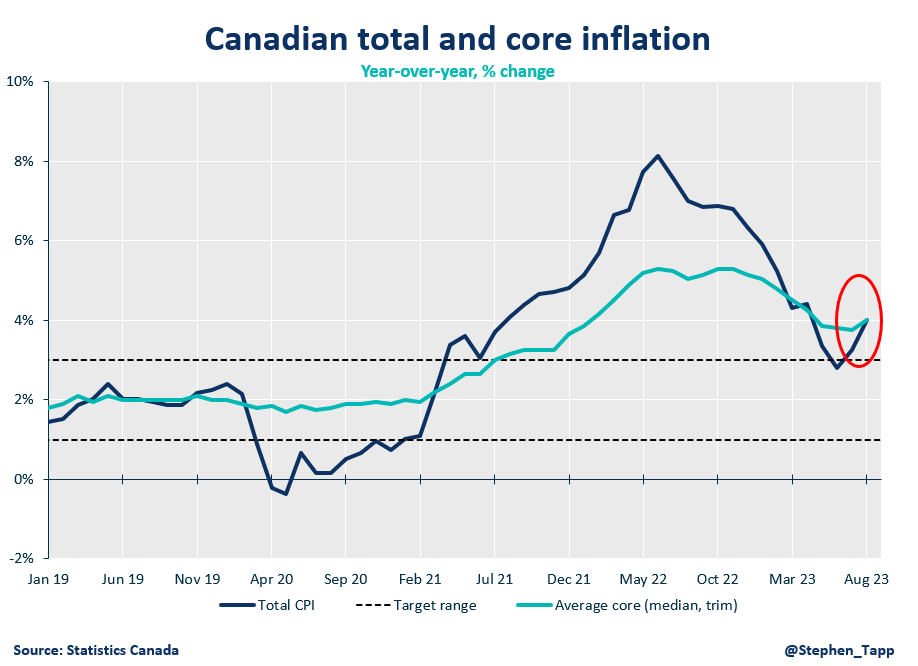

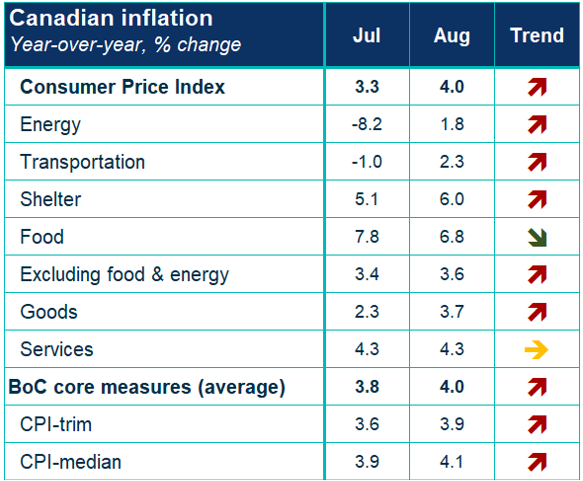

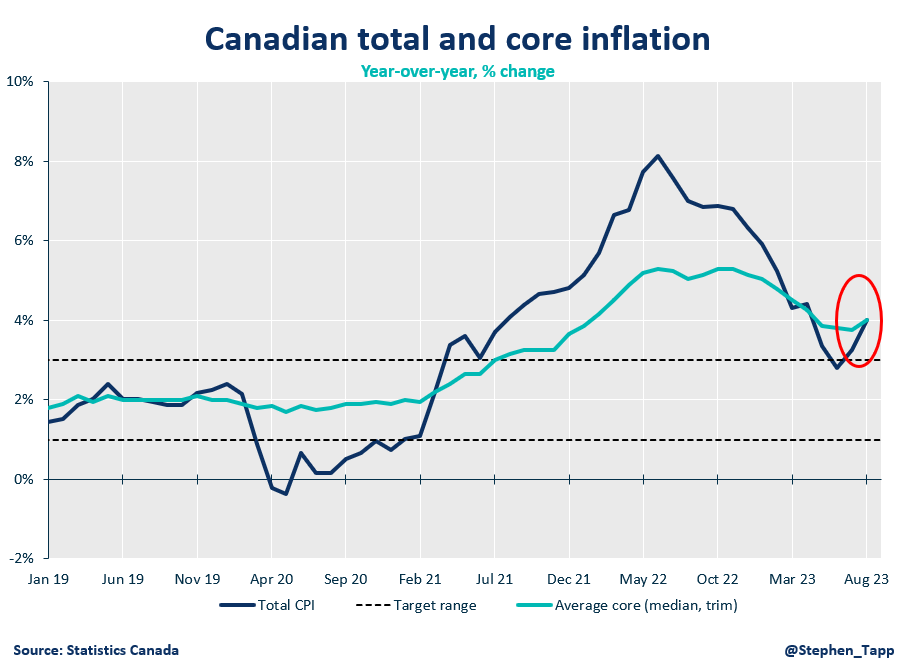

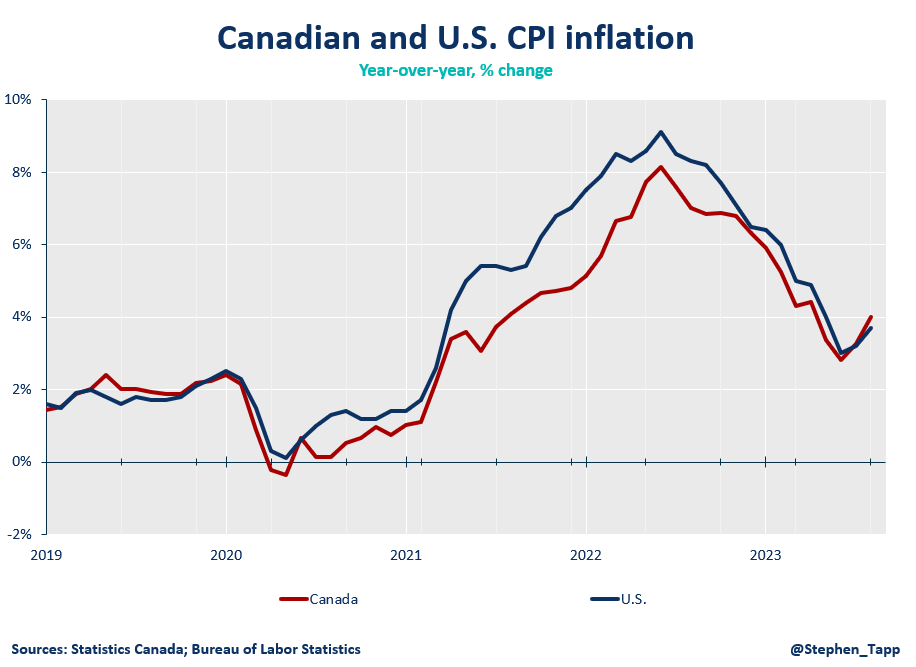

- Today’s release of August CPI was higher than expected. Canada’s headline CPI inflation grew 4% in August (compared to consensus of 3.8%) on a year-over-year basis. This comes after 3.3% growth in July, marking two months of headline CPI increases. Now that base-effects have settled in, headline inflation will swing within a range on a monthly basis.

- The Bank of Canada’s core measures of underlying inflation are also heading in the wrong direction, with an average of two core indicators (CPI-median and CPI-trim), growing at 4.0% year-over-year, and 0.4% on a monthly basis.

CPI Component

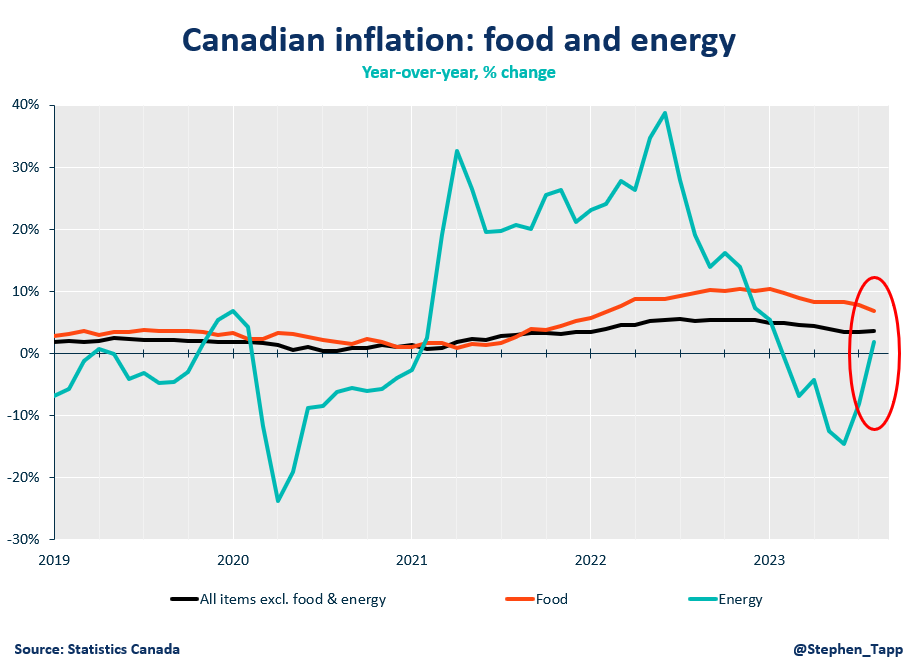

- Gasoline prices rose on a yearly basis for the first time since January 2023, by 0.8%. After a nearly 13% decline in prices in July, a reversal in direction in August drove inflation growth as base effects shift. Excluding food and energy, prices rose 3.6%. Gas prices for the first two weeks in September indicate that prices are expected to stay elevated relative to last year, largely due to reduced global supply, as opposed to strong demand.

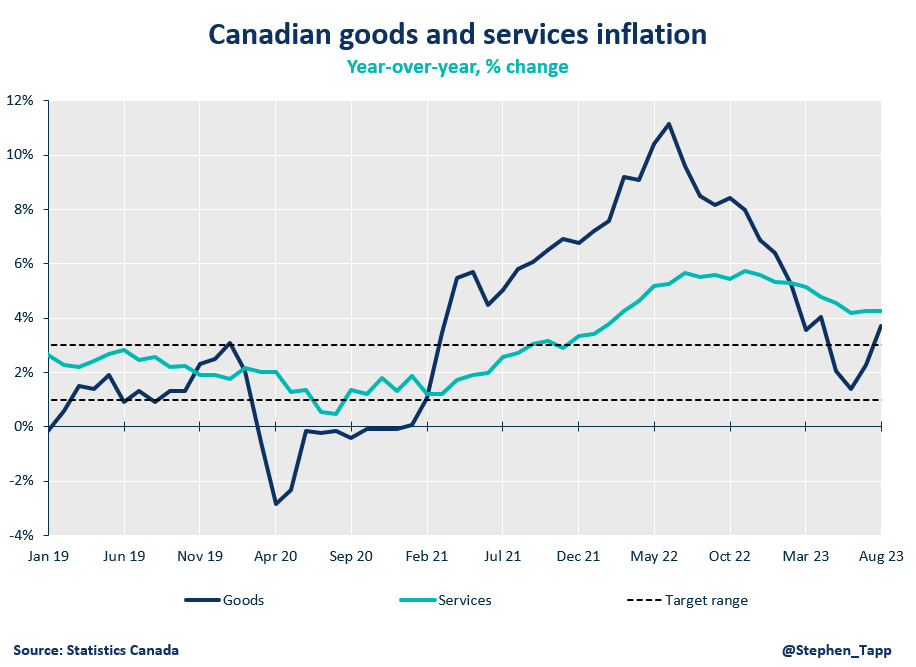

- Goods inflation rebounded in August, growing at 3.7%. Services inflation remains high and grew on an annual basis of 4.3%. This has been consistently high for months and will need to decline further in order to tame wage growth pressures.

- Despite some earlier cooling in the housing market this year, shelter prices were up 6%, primarily driven by rent price index, and further indicating pressure on supply.

- One modest bright spot in the data was a decline in grocery prices to 6.9% growth, from 8.5% in July. That said, food prices continue to grow above headline inflation and will be a continued challenge for affordability.

Provincial and regional inflation

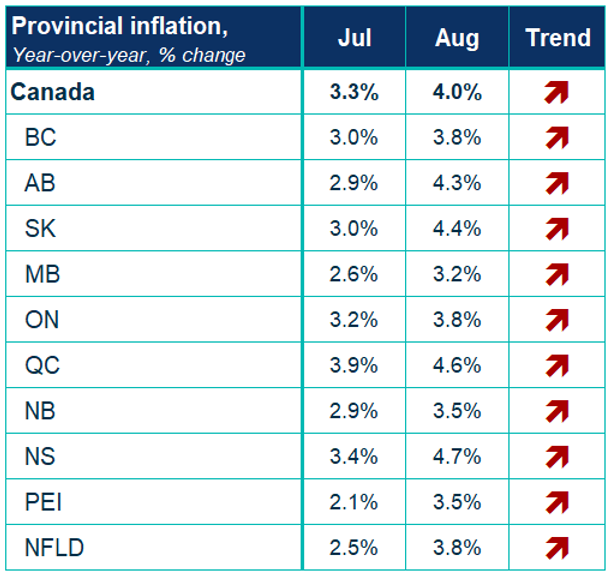

- On an annual basis, all provinces experienced upward price pressure in August, but Nova Scotia saw the highest growth at 4.7%. Price growth for gasoline accelerated the most in Alberta, growing by 13%.

SENTIMENT, OUTLOOK AND IMPLICATIONS

Bank of Canada

- The Bank of Canada’s core measures moved in the wrong direction, now hovering at almost double the Bank’s target of 2%. This will put added pressure on the Bank to raise rates at their next policy meeting on October 25. With another month of inflation data to consider, and the release of their Monetary Policy Report at the next meeting, we will have a better picture on the future path of rates.

- Ultimately, the Bank needs to consider their “higher for longer” policy, and whether another hike will put the Canadian economy in jeopardy.

Inflation expectations

- Despite inflation moving higher over the past two months, various consumer and business surveys reinforce that both input and output price growth is set to slow.

SUMMARY TABLES

Table 1: Canadian Inflation – CPI Components and BoC Core Measures

Table 2: Provincial Inflation

CPI CHARTS

Other Blogs

Retail sales defy expectations, but spending may be running out of gas.

April 2026 CPI: Inflation becoming more of an isolated energy story, for now.

Narrow Strait, Wide Impact: How a Global Shock Reaches Canada

Canada Needs More Than “Steady”: Key Findings from Business Insights Quarterly (Q1 2026)

Falling employment masks a deeper worry, with full-time jobs being replaced by part-time work: Labour Force Survey April 2025

Price-Driven Surge Pushes Canada Back into Surplus: Merchandise Trade March 2026

Canada’s economy on pace to rebound in the first quarter

The Bank of Canada sees current interest rate “appropriate” despite energy shock.