Blog /

Sputtering economy puts the Bank of Canada on pause

While the Bank held its fire, we should consider this a “hawkish hold,” emphasizing that it will raise interest rates...

Rewa

Share:

While the Bank held its fire, we should consider this a “hawkish hold,” emphasizing that it will raise interest rates further, if needed. Even though underlying inflation pressures remain problematic, the abrupt and unexpected contraction in Canada’s economy in the second quarter is for now overshadowing inflation concerns. Leading indicators suggests we could be heading into a mild recession, if we aren’t already there.

Stephen Tapp, Chief Economist, Canadian Chamber of Commerce

KEY TAKEAWAYS

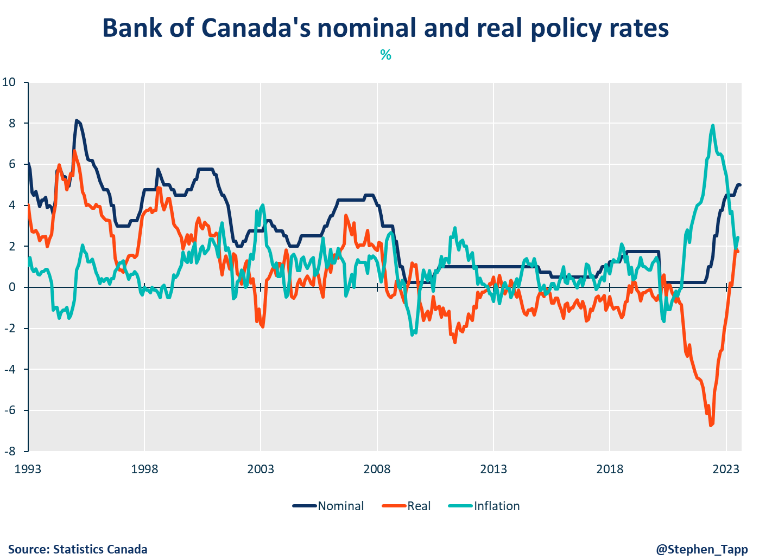

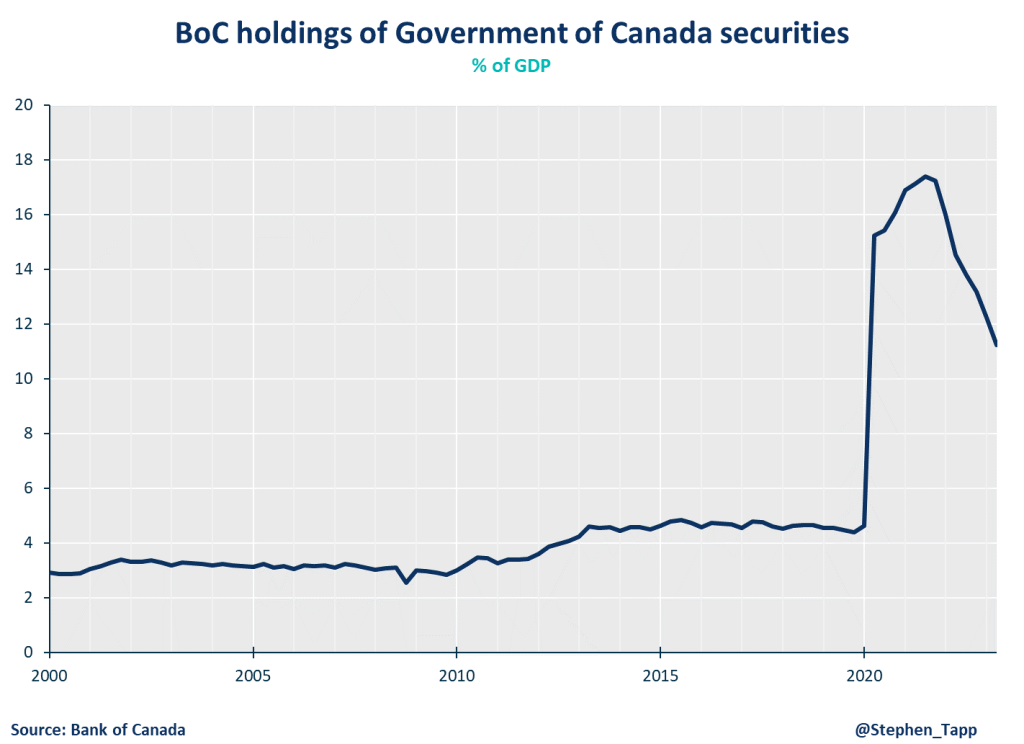

- After two consecutive rate increases over the summer, today the Bank of Canada held its policy rate at 5.0% and continued quantitative tightening, by allowing maturing assets to roll off its balance sheet. These moves were widely expected by financial markets after last Friday’s disappointing data, which showed a surprising contraction in Canada’s GDP in the second quarter (-0.2% annualized, which included downward revisions to previous data, and was well below the +1.2% growth expected).

- As our Local Spending Tracker indicated earlier, consumer spending is finally slowing in response to higher rates. For the overall economy, fast growth in population and prices have flattered headline nominal numbers, but digging into the real numbers reveals a much weaker story: official data now show Canada’s inflation-adjusted household spending per person fell in three of the last four quarters. Real GDP per capita and productivity data have also brought serial disappointments.

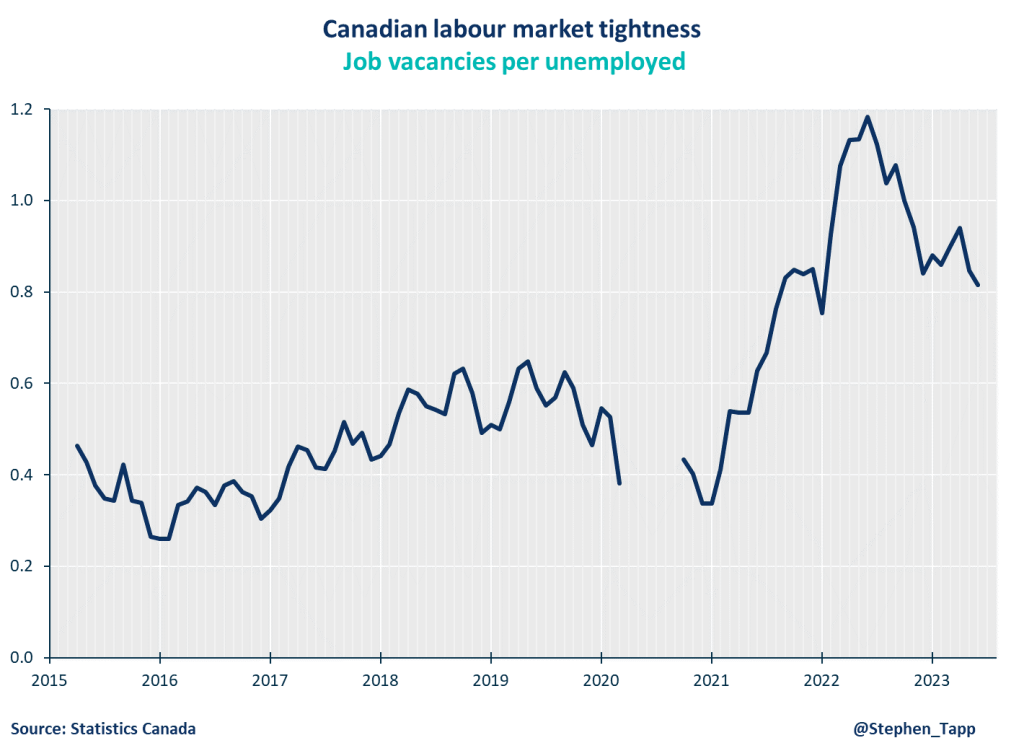

- The labour market has also softened with falling labour demand showing up in lower job vacancies. The unemployment rate has recently crept up 0.5 percentage points—which is close to crossing a threshold that often signals a recession is underway. That said, wage growth remains elevated at between 4% and 5%. Given weak labour productivity, this is above the level that’s consistent with the 2% inflation target.

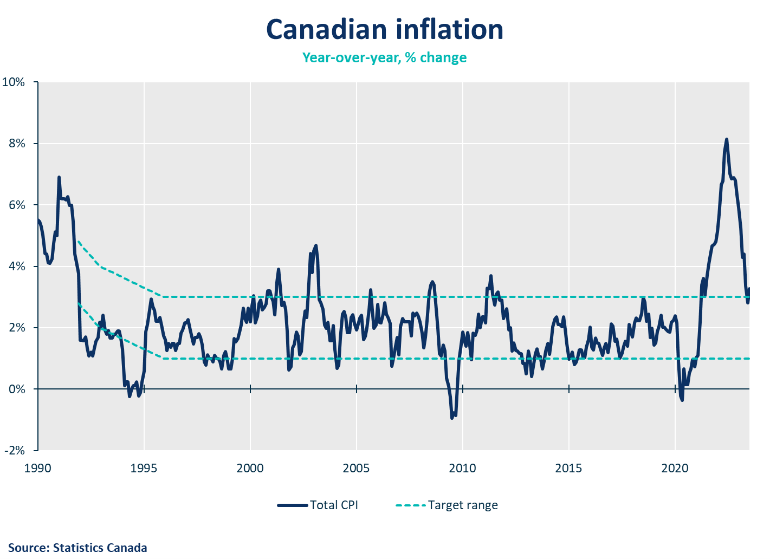

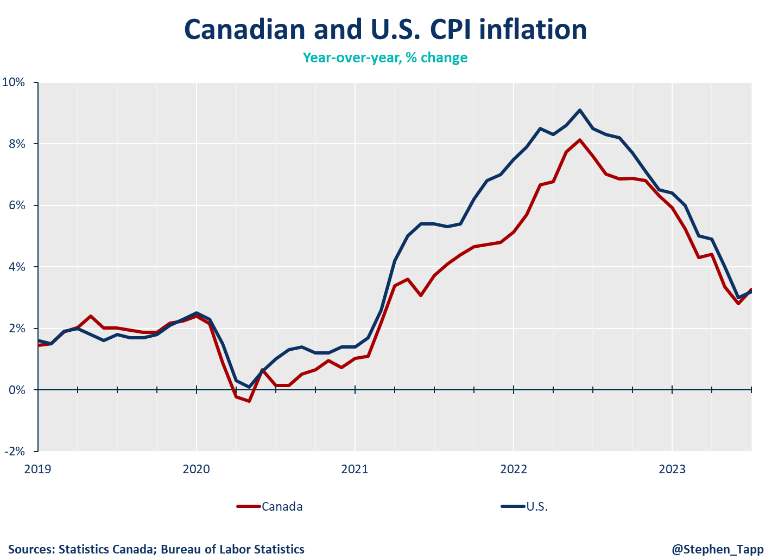

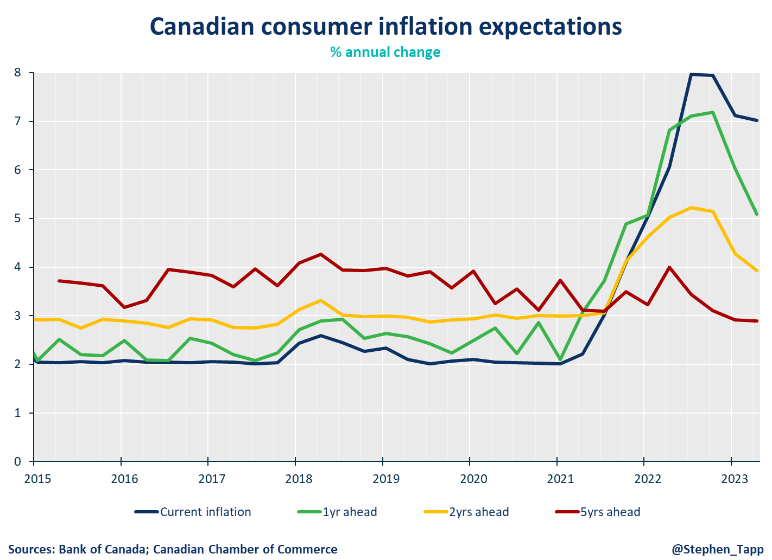

- Inflation remains broad-based and running too hot at around 3.5% annualized. It is still uncomfortably above the top of the Bank of Canada’s inflation control target, both on a year-over-year basis and in shorter-term “core” measures. The Bank emphasized that, “the longer high inflation persists, the greater the risk that elevated inflation becomes entrenched, making it more difficult to restore price stability.”

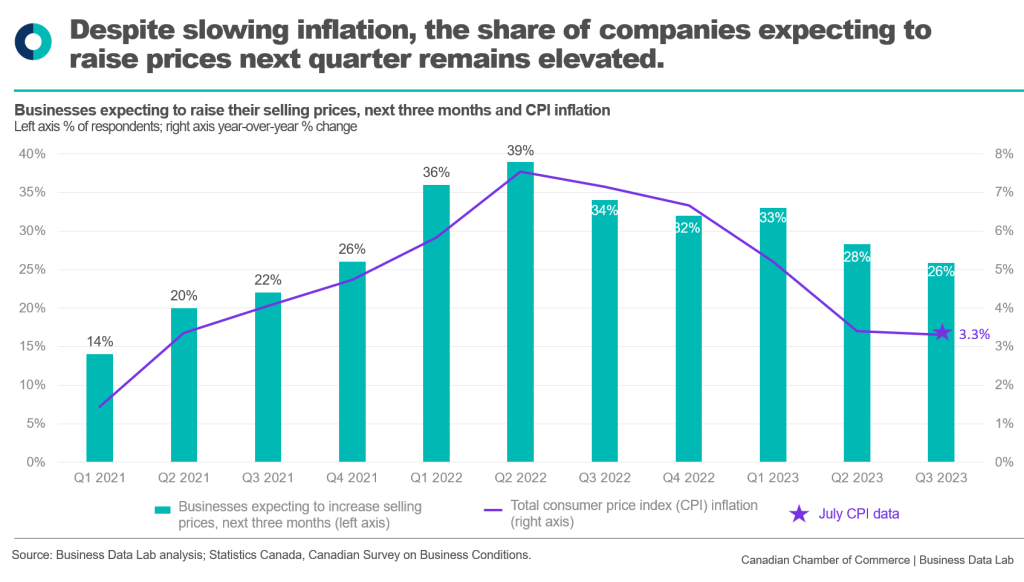

- In the last announcement, Governing Council said it was looking for progress on: short-run core inflation; wages; corporate pricing behaviour; and inflation expectations. Unfortunately, all these signs remain problematic. However, the abrupt slowdown in Canada’s economy is overshadowing these concerns and suggests we could be heading into a mild recession, if we aren’t already there.

- Overall, the Bank delivered a “hawkish hold”, as expected, stating that “Governing Council remains concerned about the persistence of underlying inflationary pressures, and is prepared to increase the policy interest rate further if needed.”

- We will have to wait until October 25th for the Bank’s next Monetary Policy Report with updated economic projections. Right now, we could be headed for mild “stagflation”, which would be difficult for the BoC, featuring slow or stagnant economic growth, but stubborn inflation that’s slow to return to the 2% target.

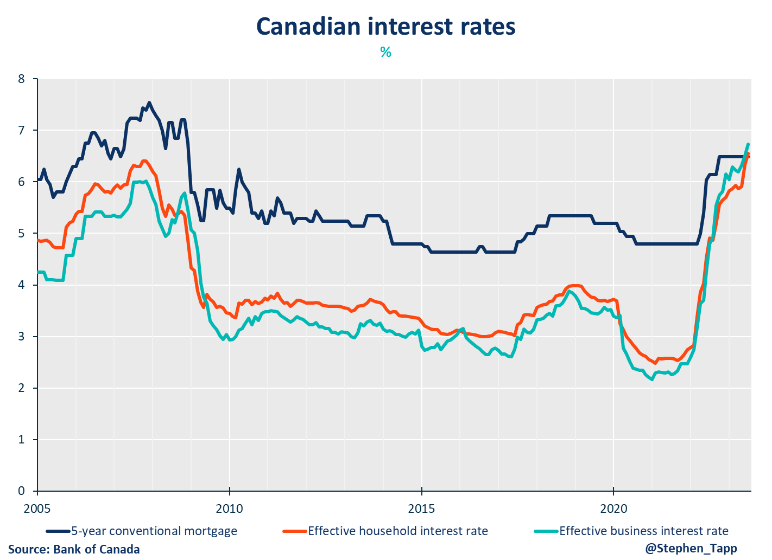

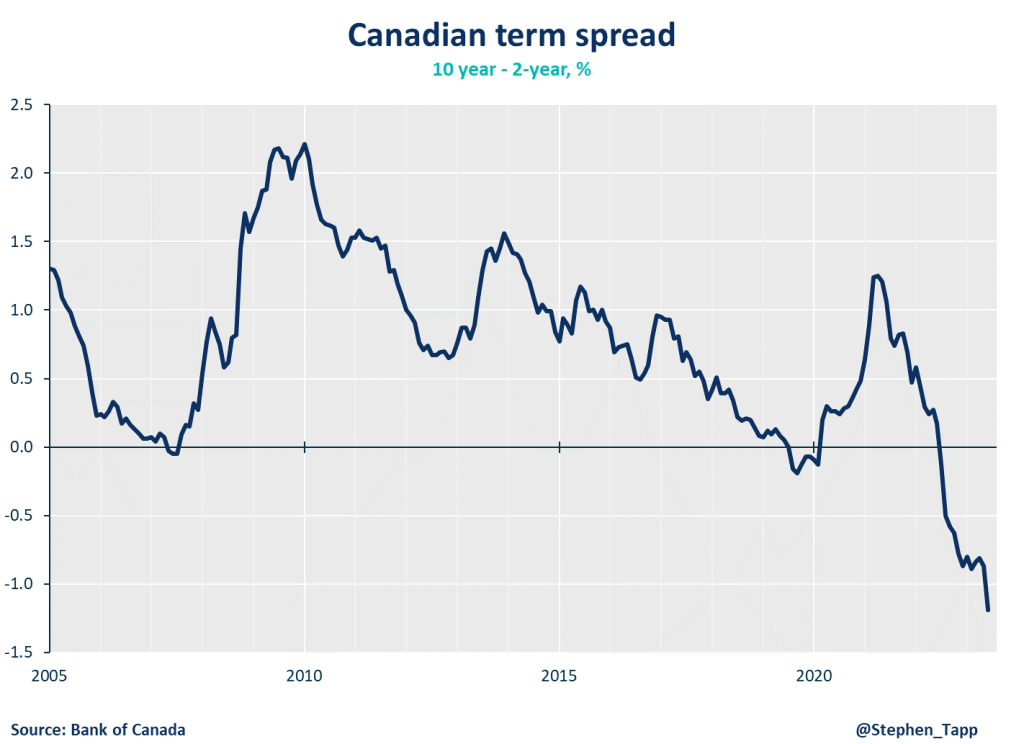

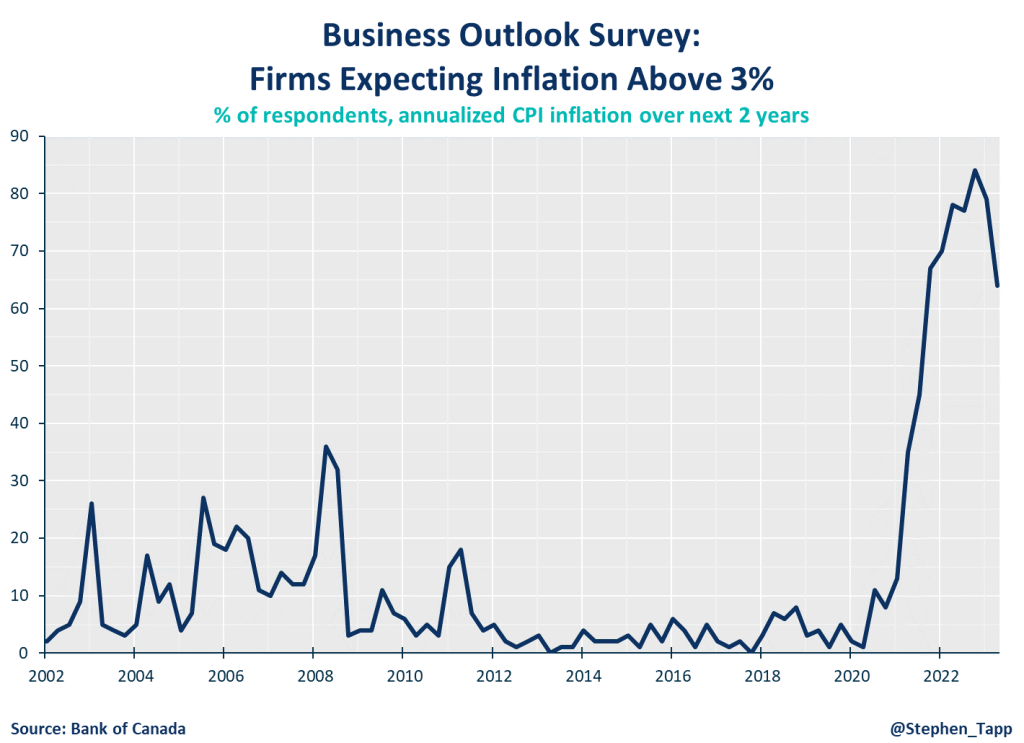

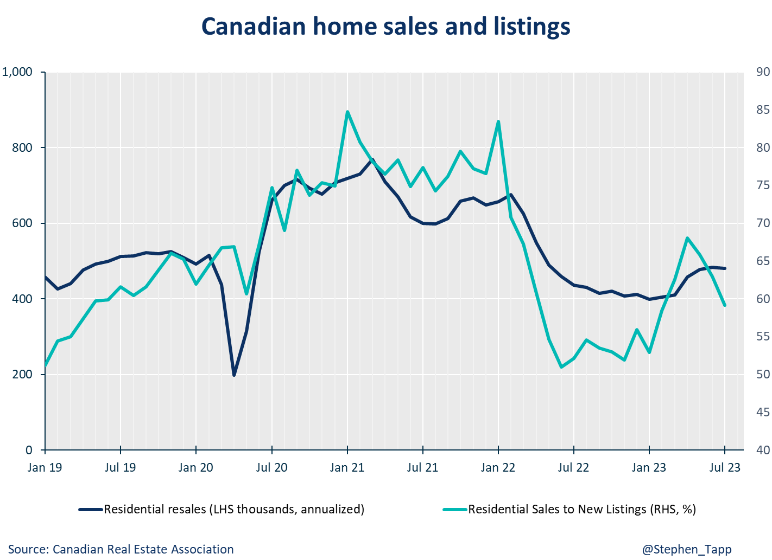

CHARTS

Other Blogs

Canada’s economy on pace to rebound in the first quarter

Use it while you can: The federal government spends its growth-driven fiscal windfall

A Solid Start, but Signs of Fatigue Emerging: Retail Sales February 2026

Inflation rises on energy shock, but underlying price pressures muted.

Sticky hiring, but wage growth at its highest since 2024: Labour Force Survey March 2025

Volatile Imports Drive Wider Deficit Despite Export Rebound: Merchandise Trade February 2026

January 2026 GDP: Canada’s economy kicks off 2026 on decent footing

Strong Start to the Year, but Underlying Momentum Remains Fragile: Retail Sales January 2026